- Exporters continue to procure paddy on expectations of demand recovery

- Prices may rise INR 10,000-12,000/t as Gulf buyers return for restocking

- Lower output, tighter stocks, higher packaging costs support bullish outlook

Morning Brief: India’s basmati rice export market is navigating an unusual phase where shipments to key Gulf destinations have slowed sharply, but prices remain resilient.

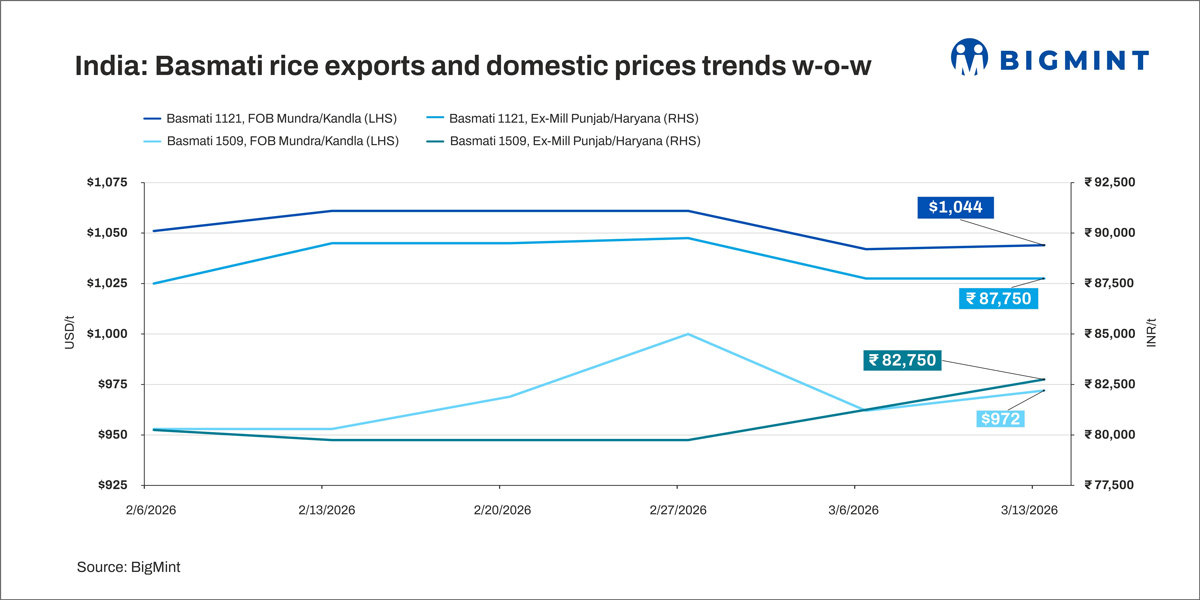

Price movements over the past six weeks highlight the market’s stability. The benchmark 1121 basmati variety, India’s premium long-grain aromatic rice widely traded above $1,000/tonne (t), softened slightly (1.6%) to $1,044/t FOB during the week ending March 13. Prices were broadly flat w-o-w after remaining at $1,061/t for three consecutive weeks through late February.

Domestic ex-mill prices in Punjab and Haryana were assessed at INR 87,500-88,000/t ($938-944/t), 2.2% below the late-February peak of INR 89,500-90,000/t ($960-965/t), indicating only slight downward pressure amid weaker export movement.

The 1509 basmati variety showed firmer momentum, with ex-mill prices rising to INR 82,500-83,000/t ($885-890/t) on 13 March, the strongest level recorded during the past six weeks, compared with INR 79,500-80,000/t ($852-858/t) in mid- and late February.

US-Iran conflict significantly disrupts Indian basmati exports

The conflict involving Iran has effectively frozen bookings across parts of West Asia, disrupting around a significant portion of India’s basmati rice trade. In total, the Middle East receives around 75% of India’s basmati rice exports. Specifically, of the 6.06 million tonnes (mnt) exported in CY’25, the largest share of around 4 mnt (66%) was consumed by Saudi, Iran, and Iraq. The rest were shipped to Yemen, Oman, Kuwait, and the UAE besides the US and UK.

Previously, in October 2025-February 2026, before the conflict started, India’s basmati rice exports were up by 13% y-o-y at around 3 mnt. October-February marks the first half of the marketing year and is also the peak export window.

Following the outbreak of the conflict, cargo movement from major export hubs such as Mundra and Kandla has slowed as exporters reassess logistics risks and freight costs.

Shipping rates have risen by $300-400/t. On some inter-ocean routes, freights have surged nearly tenfold amid the disruption. Exporters say that while the increase remains manageable for premium basmati shipments trading above $1,000/t, the same rise has significantly eroded margins for parboiled and white rice, which typically trade at $400-$425/t CIF.

Prices remain resilient despite stalled exports

Despite the slowdown in cargo movement, exporters and millers across the basmati belt of northern India are maintaining prices, optimistic that demand will rebound once geopolitical tensions ease.

Market participants say the resilience has surprised traders who expected a sharper correction given the disruption in export demand. “Movement is severely being affected due to the war, yet prices are not softening. Perhaps stockists are maintaining their levels,” said a senior exporter in northern India.

“If the war does not end by next month, prices may begin to soften. But for now, the market is not showing any downward trend,” said Ram Sahare, founder and managing director of Amar Singh Chawalwala.

In fact, millers and stockists across major basmati-producing regions such as Karnal, Amritsar and Ludhiana said that several exporters are continuing to procure paddy and build inventories rather than selling aggressively. “Basmati dealers do not sell in panic. There is simply no substitute for basmati. That is one fundamental difference from commodity rice,” said a mill owner in Haryana.

Moreover, packaging costs have firmed and inventory carrying costs have climbed higher, driven by longer holding periods and elevated financing expenses rather than a sharp rise in base warehousing tariffs. This has created a cost floor that limits the scope for price reductions.

In fact, according to Sahare, prices across basmati varieties could rise by INR 10,000-12,000/t ($107-129/t) if exports restart quickly after a ceasefire, as Gulf buyers return to replenish stocks.

Additionally, while current visible inventory appears elevated due to shipment disruptions, underlying pipeline stocks are tight (20 to 30% lower in key producing belts) due to weather damage. Basmati production from key states — Punjab, Haryana, Jammu and Kashmir, Himachal Pradesh, Uttarakhand, and Uttar Pradesh — also fell 5% y-o-y to 40 mnt during the kharif season of the 2025-26 marketing year. Therefore, excessive supply pressure has not emerged in the market.

Export diversification unlikely

In terms of potential export diversification, temporary adjustments are possible, but structural shifts are unlikely. There is currently no significant consumer base capable of absorbing the high volume of exports shipped to the Middle East.

Initially, the EU and Africa had emerged as possible alternatives. However, the EU’s stringent Maximum Residue Limits (MRL) remain a primary barrier. Indian exports frequently struggle to meet these low-pesticide requirements. Meanwhile, African buyers typically demand payment terms of 10% advance and 90% after shipment. Basmati dealers, accustomed to more secure Middle Eastern transactions, do not prefer these credit-heavy ratios.

Moreover, in markets including Nigeria, Benin, the Ivory Coast, Senegal, and Guinea, basmati remains a luxury. These regions are highly price-sensitive, favouring lower-cost non-basmati varieties. Similarly, major Asian economies rely on domestic or regional non-basmati rice.

Outlook

The Indian basmati market stands on a strong foundation: India commands 85% global market share, stocks are light this season, and despite Gulf tensions disrupting Iran trade, demand from Saudi Arabia, Iraq, UAE, and Yemen remains firm. The Middle East conflict will likely be a timing and delivery problem, not a demand collapse.

Over the next 2-4 months, basmati prices will depend on how the Middle East situation develops. If Hormuz tensions ease, demand will pick up, and prices can rise to around INR 95,000-105,000/t (1,019-1,126/t). If the current situation continues, prices will likely stay steady between INR 84,000-90,000/t ($901-965/t).

Conversely, if the conflict worsens, prices may fall slightly to INR 78,000-85,000/t ($836-911/t), but a big drop is unlikely because supply is tight and demand is still there, as the Middle East is heavily reliant on India for its rice imports.

Leave a Reply