- Freight supported by firm coal shipments

- Limited activity even with higher fixtures

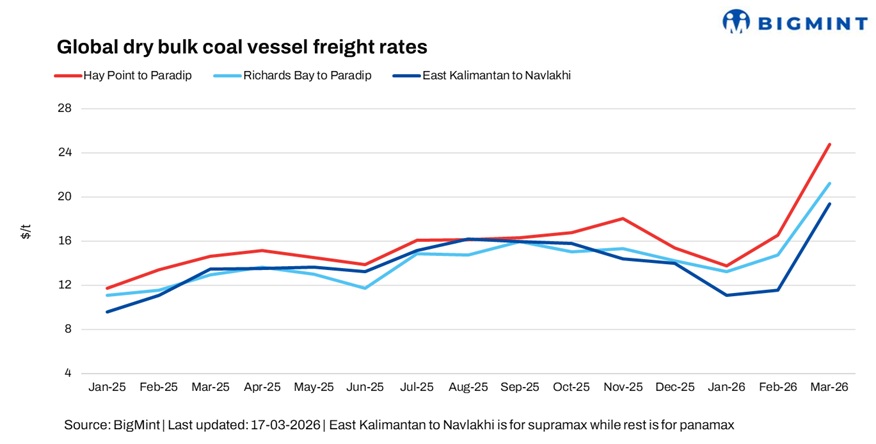

Dry bulk coal freight rates rose w-o-w as of 17 March, supported by firm coal shipments and tighter vessel supply on key India routes, though bunker price volatility kept market sentiment cautious.

According to market sources, fixtures on certain routes were concluded at higher levels despite the broader uncertainty surrounding bunker pricing and vessel operating costs. “Several traders can’t pay the market levels right now leading to less fixtures,” a ship broker said.

On the Atlantic basin, stronger coal shipments toward India combined with tightening vessel supply helped support Panamax freight sentiment during the week. However, participants indicated that enquiry levels remained somewhat limited, suggesting that market momentum was not entirely broad-based.

Adding to the cautious tone, another source told BigMint that sentiment appeared to be moderating. “Supramax seems to be softening a bit in Southeast Asia, while Panamax has also started to lose some steam. Freight may be slightly down for Supramax,” the source said.

“As per our information, bunker listed prices are higher but physical levels are considerably lower,” the source added. Meanwhile, market activity in the Supramax segment remained relatively muted, with limited cargo enquiries reported in the regional market even as Indonesian coal shipments to India continued.

A coal cargo fixture was reported last week by the Steel Authority of India Limited (SAIL), indicating active chartering on the east coast trade route. A vessel of 75,000 ±10% mt has been fixed for the Abbot Point-Hay Point-Dalrymple Bay to east coast India route, with laycan scheduled between 3-12 April at a freight rate of $29.90/dry metric tonne (DMT).

Reflecting the cautious mood among shipowners and charterers, another industry participant said that the lack of clarity around bunker costs was discouraging active fixing. “Don’t know what to say given the bunker prices. Not hearing much fixtures as of now,” the source said.

Outlook

Freight sentiment is expected to remain mixed in the near term as bunker price movements and evolving market fundamentals continue to influence vessel operating costs and chartering decisions. While firm cargo flows may continue to lend support to freight levels on certain routes, market participants are likely to remain cautious until clearer pricing signals emerge in the bunker market.

Leave a Reply