- Bunker price volatility is lending support to freight levels

- Cautious buying sentiment is slowing fixing activity

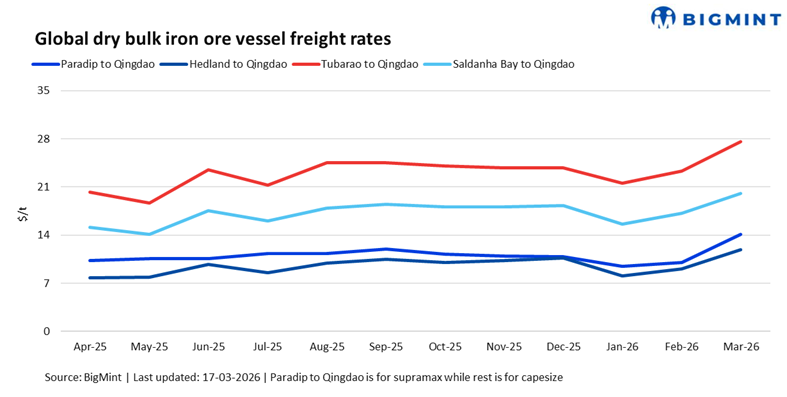

Dry bulk iron ore freight rates increased w-o-w as of 17 March 2026, driven by an uptick in the Capesize segment, supported by firmer FFA levels. However, overall market activity remained subdued, with participants adopting a cautious stance amid bunker price volatility and rising freight rates.

A source informed BigMint, “Supramax vessel sentiment in Southeast Asia appears to be softening, with freight rates edging slightly lower. Panamax rates remain broadly stable but show a weakening trend. Capesize continues to hold relatively firm for now. ”

Route wise updates:

“Bunker prices remain a key variable – while listed levels are elevated, physical trades are being concluded at noticeably lower levels. For instance, a recent fixture indicates VLSFO was booked around USD 950/mt in Singapore, compared to listed indications near USD 1,100/mt, highlighting a significant gap between paper and physical pricing.”

Another source informed “Current market levels appear too elevated for several traders to participate actively.”

Outlook

Iron ore freight rates are expected to remain range-bound with a slight firm bias, supported by bunker price volatility and relatively tight tonnage. However, slow trading activity, cautious buying, and resistance to higher rate levels are likely to cap further upside, keeping overall sentiment balanced but fragile.

Leave a Reply