- Concentrate imports rising to feed expanding smelting capacity

- TC/RCs are collapsing due to intense competition for raw materials

China’s refined copper production hits record high despite tight concentrate supply

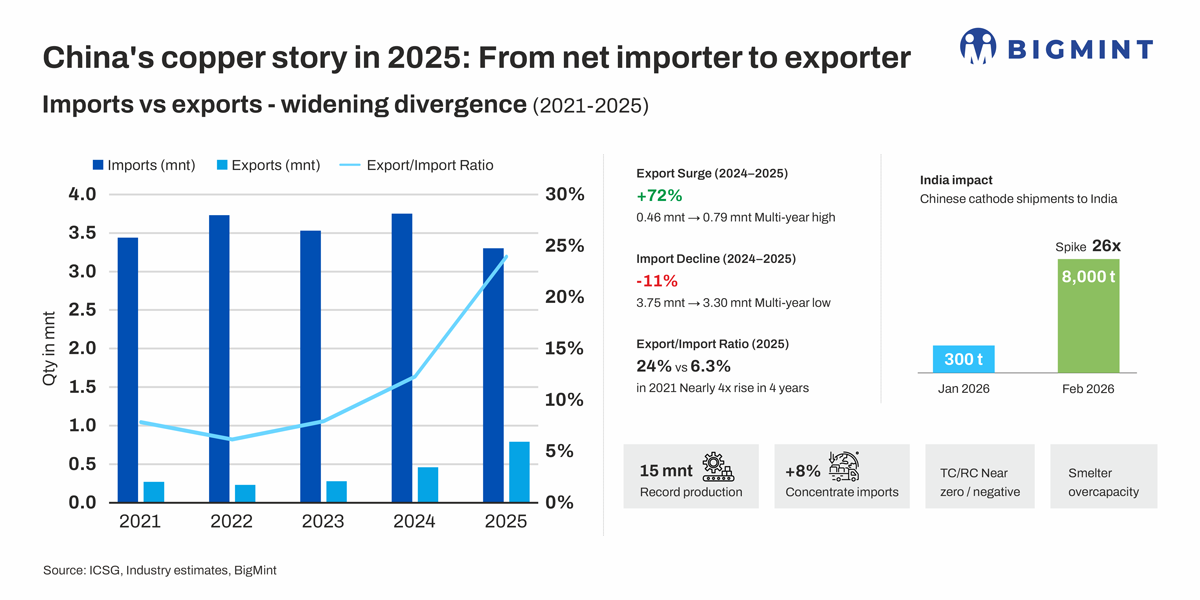

China’s refined copper production surged to nearly 15 mnt in 2025, up sharply from ~13.6 mnt in 2024, marking a record high. What makes this rise particularly significant is that it occurred amid severe copper concentrate shortages and historically low TC/RCs, indicating that smelters expanded output despite deteriorating processing economics.

This reflects the capacity-led nature of China’s copper industry, where production decisions are increasingly driven by installed smelting capacity rather than raw material availability. The aggressive ramp-up highlights the strategic importance of maintaining output levels, even under margin pressure, to retain global dominance.

According to International Copper Study Group (ICSG) data, global copper smelting capacity is expected to grow from about mnt in 2024 to approximately 30 mnt by 2028, representing a compound annual growth rate of 3.8%.

The majority of this expansion is projected to occur during 2025-2026, with China driving much of the growth. Chinese smelters currently account for more than 50% of global copper smelter output.

What is driving surge in output?

The primary driver was large-scale smelting capacity additions, particularly by major integrated players such as Tongling Nonferrous Metals Group. The commissioning and ramp-up of 800,000 t/year of new capacity significantly boosted refined output during the year.

The second phase of the Mirador Copper Mine in Ecuador, operated by Tongling Nonferrous Metals Group, has completed construction and entered the trial run stage, marking a key milestone in China’s overseas resource expansion.

Phase II is expected to add 60,000-70,000 t of copper output annually, taking the mine’s total capacity to around 140,000-160,000 t/year. The project is being advanced alongside the formal signing of mining contracts and operational agreements.

Once fully ramped up, Mirador will strengthen long-term concentrate supply security for Chinese smelters, especially amid tight global feedstock conditions and historically low TC/RCs.

Overall, China’s smelting capacity has expanded by 25% since 2021, creating a situation of structural overcapacity. This excess capacity has intensified competition among smelters for limited concentrate supply, leading to aggressive procurement strategies and sustained high operating rates.

Unlike traditional market behaviour where low margins lead to production cuts, Chinese smelters continued operating at elevated levels, indicating a market-share-driven approach rather than margin optimisation.

Is China reducing dependence on refined copper imports?

Refined copper imports declined to 3.3 mnt in 2025, down from 3.7-3.8 mnt in 2024, marking a multi-year low.

This decline was primarily driven by higher domestic production, which increasingly met internal demand. The broader implication is that China is steadily transitioning from being a net importer of refined copper to a more balanced or even surplus market.

Why did refined copper exports surge to multi-year highs?

China’s refined copper exports rose sharply to 0.79 mnt in 2025, compared to 0.46 mnt in 2024, reflecting an increase of 72% y-o-y and marking a multi-year high.

This surge was driven by a mismatch between supply and demand. While production rose significantly, domestic consumption increased only modestly to 17.48 mnt, up from 16.86 mnt in 2024. This created surplus availability within the domestic market.

As per reports, global arbitrage opportunities improved, making exports more attractive. Chinese smelters and traders were able to achieve better netbacks in international markets compared to domestic sales, encouraging outbound shipments.

China’s growing presence in export markets was particularly evident in India, where shipments increased from 300 t in January to 8,000 t in February, reflecting competitive pricing and surplus availability.

This trend indicates that China is not only self-sufficient but is increasingly acting as a swing supplier in the global refined copper market.

China’s concentrate imports in 2025

China’s copper concentrate imports increased from 28.16 mnt in 2024 to 30.37 mnt in 2025, reflecting a growth of ~8% y-o-y.

Rather than importing refined metal, China is increasingly focused on securing raw materials (concentrates) and processing them domestically. This shift is largely driven by the need to feed its rapidly expanding smelting capacity, ensuring high utilisation rates across newly commissioned plants. This approach allows the country to maximize value addition within its own industrial ecosystem.

The increase in concentrate imports is particularly notable given the tight global supply environment, highlighting China’s ability to secure feedstock even under constrained conditions while sustaining elevated smelter operations.

Why did TC/RCs collapse despite strong concentrate imports?

China’s TC/RC scenario in 2025 has been shaped by direct negotiations between major Chinese smelters such as Tongling Nonferrous Metals Group and Jiangxi Copper, and global miners like Antofagasta. Benchmark terms were settled at historically low levels of around $20-25/t, with some spot deals reported at near-zero TC/RCs due to intense competition for concentrate.

As tightness deepened, certain Chinese smelters even accepted negative TC/RCs in spot transactions, effectively paying miners to secure feedstock. This shift highlights rising miner bargaining power and reflects how smelters are prioritising raw material security over margins to sustain operations and utilise newly added capacities.

Despite higher concentrate imports, TC/RCs fell into negative territory in 2025, an unusual and extreme market condition. This indicates that demand for concentrate from smelters significantly exceeded available supply.

The primary reason lies in overcapacity in smelting. With too many smelters competing for limited concentrate, miners gained pricing power, forcing smelters to accept unfavourable terms.

In some cases, smelters effectively paid miners to secure feedstock, highlighting the severity of the imbalance. This represents a reversal of traditional dynamics, where smelters typically earn processing margins.

Outlook

Chinese domestic oversupply amid tepid demand and global arbitrage opportunities drove Chinese exports of refined copper up sharply in 2025. Will China continue to act as a swing supplier even in 2026? More importantly, how will the aggressive behaviour of Chinese smelters in acquiring copper concentrates even at the expense of positive margins affect the global market and prices, given China’s outsized influence in the market?

Book your seat at the upcoming BigMint India Non-Ferrous Week (BINFW) for insights on global copper demand shifts, supply constraints and pricing outlook

Leave a Reply