- Rising demand with price spikes indicates supply pressure

- Stocks sufficient overall, but regional shortages persist

Electricity demand

The first 15 days of March 2026 have seen a clear and significant increase in electricity demand compared to the same period in 2025. Peak demand levels are consistently higher, indicating robust economic activity and early onset of summer conditions.

Generation momentum: The strong power generation momentum from February has not only been maintained but has accelerated in the first half of March. This ramp-up is critical to meeting the surging demand.

IEX market dynamics: The power market on the IEX is reflecting this demand-supply tension. While total offered and cleared volumes are higher in March 2026, indicating a more active market, the average Market Clearing Price (MCP) has also risen sharply. The price spikes observed in mid-March suggest periods of supply tightness where expensive generation is being called upon.

Coal stock adequacy: At an all-India level, coal stocks at power plants appear comfortable and have been steadily built up ahead of summer. However, this national picture masks significant regional imbalances. High-demand states like Tamil Nadu, Telangana, and Rajasthan have stock levels well below the national average, making them vulnerable to supply chain disruptions and requiring robust inter-regional power transfers.

Power demand: March 2026 vs March 2025 (first 15 days)

The data clearly shows a substantial increase in peak electricity demand during the first half of March 2026 compared to the same period in 2025.

Higher peak: The peak demand in the first 15 days of March 2026 reached 238,378 MW (on 7 March), compared to 235,224 MW (on 11 March) in 2025.

Sustained strength: On 10 out of the first 15 days, the peak demand in 2026 exceeded the corresponding day’s peak in 2025.

Early summer load: The consistently high demand levels above 230 GW in 2026 (observed on 9 out of 15 days) point towards an early and strong summer demand season, likely driven by increased cooling needs and industrial activity.

Therefore, the demand for electricity in early March is significantly stronger and more consistently high than in the previous year, confirming a growth trajectory in power consumption.

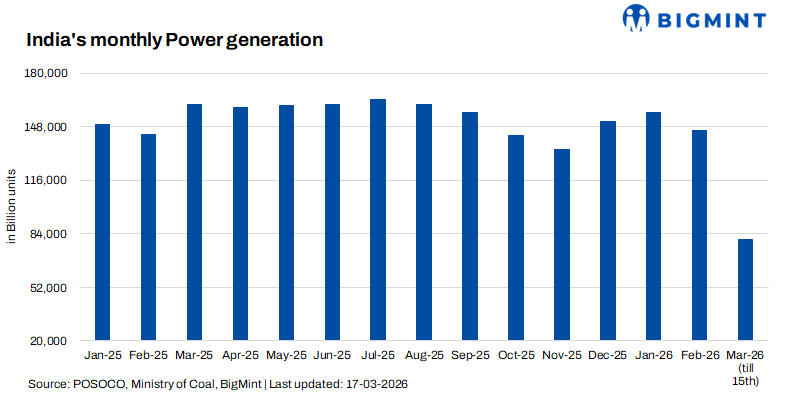

Generation ramps up

The robust generation momentum established in February has not only been maintained but has accelerated in the first half of March 2026.

Sustained high generation: Average daily generation in the first 15 days of March (5,355 MU/day) is higher than the average for the entire month of February (5,192 MU/day).

Rapid ramp-up: Generation in March started strong and quickly surpassed February’s peak levels, hitting 5,605 MU on 11 March compared to February’s peak of 5,357 MU on 27 February.

Coal-based lead: The increase in total generation is primarily driven by a significant jump in coal-based power. Average daily coal generation rose from ~3,779 MU in Feb to ~3,908 MU in the first half of March. Renewables also showed strong performance.

Power plants, especially coal-fired ones, have successfully ramped up operations to meet the rising demand. The generation momentum from February has been carried forward and amplified in March.

Power exchange signals stress

The Indian Energy Exchange (IEX) data reveals a market under pressure, characterized by higher demand, increased activity, and significantly higher prices in 2026.

Higher demand & activity: The average daily purchase bid in March (239,804 MWh) is 32% higher than in March 2025 (181,396 MWh), indicating stronger appetite from buyers. The final scheduled volume (cleared volume) is also up by 28%.

Supply response: Sell bids have also increased dramatically (by 42% on average), suggesting that sellers are responding to higher prices and bringing more power to the exchange.

Sharply higher prices: The average Market Clearing Price (MCP) for the first 15 days has surged to INR 4,187/MWh in 2026 from INR 4,167/MWh in 2025. This marginal increase in average hides significant volatility. Prices in mid-March 2026 (for example INR 6,695 on 13 March) far exceeded any prices seen in the same period of 2025 (peak of INR 5,158), indicating periods of acute supply tightness where expensive generation was required to meet demand.

The IEX market is functioning as a crucial balancing mechanism. The surge in buy bids and cleared volumes shows increasing reliance on the spot market. The high and volatile prices are a direct signal of the demand-supply gap, incentivising all available generators to sell power.

Coal stocks adequate nationally but regional vulnerabilities persist

The available data paints a picture of comfortable national stocks but highlights critical regional vulnerabilities.

Adequate national stocks: The daily coal report for plants with domestic linkages (TOTAL A) shows total actual stocks of 53.19 million tonnes against a normative requirement of 69.29 million tonnes. This gives a national average of 76% of normative stock, which is generally considered comfortable. Stocks had already been building steadily through February, reaching about 59.29 mnt.

Imported coal plants in distress: Plants designed to run on imported coal are in a more precarious position. Several facilities, including Adani Power Mundra, are flagged as critical with stocks as low as 8% of normative levels, highlighting their dependence on international coal markets.

Regional coal imbalances

The national average hides severe regional disparities. Several high-demand states are operating with coal stocks significantly below the national average.

Tamil Nadu (TANGEDCO): Overall stock stands at only 41% of normative levels. Specific plants such as North Chennai TPS Stage-2 (19%) and Tuticorin TPS (29%) are flagged as critical.

Telangana (TSGENCO): Overall stock is about 33% of normative levels, with Kothagudem TPS (NEW) at 23% flagged as critical.

Rajasthan (RRVUNL): Overall stock is 71% of normative, but this is pulled down by plants such as Kalisindh TPS (64%) and Suratgarh TPS (43%), the latter being flagged critical.

Comfortable states

Coal-producing regions remain well supplied.

• Chhattisgarh (CSPGCL): 153% of normative stock

• Uttar Pradesh (UPRVUNL): 93% of normative stock

This confirms the continuing role of pithead plants in eastern and central India as the backbone of the country’s power system.

Market opportunities emerging from regional imbalances

The emerging imbalance between coal availability and electricity demand is likely to shape market dynamics during the upcoming summer months.

Although coal stocks are comfortable at the national level, they are unevenly distributed across the country. Coal-producing states in eastern and central India hold large inventories, while several high-demand southern and western states are operating with significantly lower stock levels.

This imbalance is likely to create several market opportunities.

First, stronger long-distance coal movement: States with low stocks will need increased coal deliveries from mines in eastern and central India. This will place greater demand on railway logistics and coal evacuation infrastructure.

Second, higher inter-regional power transfers: Electricity generated by pithead plants will increasingly be transmitted to deficit regions in southern and western India, making India’s national transmission grid even more critical during the summer months.

Third, selective imported coal demand: Power plants designed to run on imported coal – particularly coastal plants – may need to increase imports to rebuild stocks and maintain generation levels.

Moving power and coal across India

India has enough coal overall to meet the expected summer demand. The challenge lies in ensuring that the fuel is available in the regions where electricity demand is growing the fastest.

The southern and western states depend heavily on long-distance coal transportation from mines located in eastern India. As demand rises, this dependence will increase.

This makes both the national power grid and the Indian Energy Exchange crucial mechanisms for balancing supply across regions. Electricity generated by well-supplied pithead plants in central and eastern India must be efficiently transmitted to demand centres in southern and northern India.

Any disruption in coal transport through the rail network or constraints in transmission capacity could quickly transform a comfortable national fuel situation into localized power shortages.

Summer demand will test coal logistics

India’s electricity demand is already showing signs of a strong summer season.

While the country currently has adequate coal stocks in total, maintaining system stability will depend on three critical factors:

• efficient coal transportation across long distances

• strong inter-regional transmission flows

• active balancing through the IEX power market

The current situation does not indicate a shortage of coal in India. Instead, it highlights a logistical and geographical imbalance between where coal is available and where electricity demand is rising.

Managing this imbalance effectively will be key to maintaining reliable power supply during the peak summer months while also creating new opportunities across the coal supply chain.

Leave a Reply