- Gas market volatility pushes power producers towards high-CV coal

- Tight portside supply, slow dispatches, lower output lift Indian prices

High-calorific US NAPP (Northern Appalachian) coal is quietly becoming one of the most sought-after fuels in the global thermal coal market. The current strength in prices is not being driven by one single factor. Instead, it is the result of three different developments happening at the same time.

First, petcoke prices have surged, and supply has tightened, forcing cement producers to search for alternatives. Secondly, gas markets in Europe remain volatile, which is improving the relative economics of coal for power generation. Thirdly, portside availability of US high-CV coal in India has become increasingly concentrated, pushing retail prices sharply higher.

Together, these factors are creating strong demand for high-energy coal from the United States and supporting a rise in FOB prices in the Atlantic market.

Global high-CV coal prices move higher

In the international market, high-CV thermal coal prices have been strengthening steadily.

Recent market indications show FOB US East Coast 6,900 NAR coal trading around $90-95/t, while European delivered coal prices near the ARA hub are around $120/t for 6,000 NAR material. At the same time, FOB Newcastle 6,000 NAR coal is trading close to $130/t, highlighting how high-energy coal grades continue to command strong premiums in the global market.

These prices are being supported by two key dynamics:

(1) continued uncertainty in global gas markets and

(2) renewed interest in high-calorific fuels for power generation and industrial use.

Whenever gas markets tighten, power producers tend to look again at coal as a reliable alternative fuel. Even a modest increase in coal burn can tighten the global market because the supply of high-energy coal grades is relatively limited.

This is particularly supportive for US NAPP coal because of its very high calorific value, typically around 6,900-7,100 NAR, which allows it to compete directly with premium coal grades used in both power and industrial applications.

Petcoke shortage pushes cement plants towards coal

The most immediate demand boost for US NAPP coal is coming from the cement industry.

Petcoke has traditionally been the preferred fuel for many cement plants because of its high calorific value and relatively low price per unit of energy. However, the global petcoke market has tightened sharply. Imported US petcoke prices have recently climbed to around $150-155/t CNF India, compared with roughly $125-130/t earlier in the year. Freight costs have also increased, pushing delivered prices higher.

At the same time, domestic petcoke availability in India has tightened significantly. Several refiners have raised prices sharply for March supply. Some refineries have increased prices by more than INR 1,200/t, while others have lifted prices to around INR 16,000/t, the highest levels seen in nearly two years.

Another key factor tightening the market is that one of the largest refiners is consuming most of its petcoke internally, leaving very limited volumes available for the merchant market. As a result, cement producers are increasingly shifting towards alternative fuels, particularly high-calorific imported coal such as US NAPP.

Portside NAPP stocks in India tighten

While imports of US coal continue, the availability of prompt material in the domestic market has become extremely tight. Recent portside data shows that combined stocks of NAPP coal at Kandla and Tuna ports are only about 265,000 t. More importantly, much of this inventory is controlled by a small number of large buyers.

One major industrial buyer alone holds more than 150,000 t, while another cement producer controls more than 100,000 t. That means only a limited quantity of coal is actually circulating in the spot market.

Weekly lifting data also shows that recent dispatches were relatively modest, indicating that many holders are either conserving stocks or selling selectively at higher prices. This concentration of stocks has created a classic squeeze in the portside market.

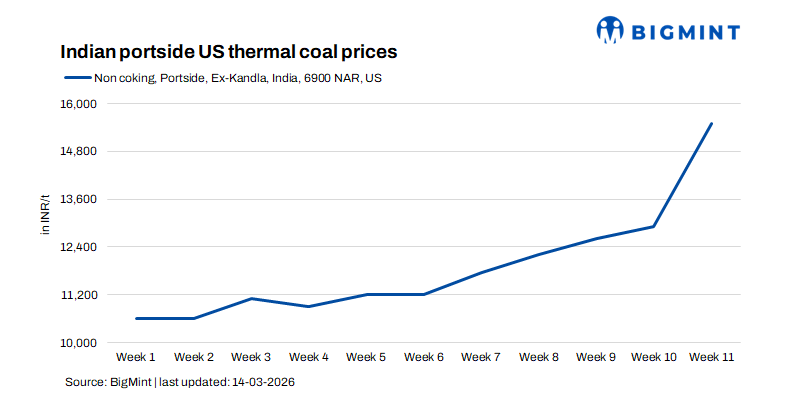

Retail prices at ports surge sharply

The tightening supply situation has pushed retail prices higher in a very short time.

In early March, portside prices of US thermal coal were widely indicated around INR 12,800-13,000/t ex-port. Within a few days, prices rose to INR 15,000-16,000/t as buyers rushed to secure available material. Recent offers for vessel-linked cargoes have increased, with current vessel supplies quoted at INR 16,100-16,200/t, while prompt cargoes are offered higher at INR 16,800-17,000/t, indicating tighter immediate availability.

These prices reflect not only the cost of imported coal but also the tightness of physical supply at the ports. In markets where inventory is concentrated among a few holders, prices can rise much faster than international benchmarks.

Brick kilns also feel the pressure

The tightening coal market is not only affecting large industrial users. Smaller industries are also facing significant fuel cost pressures.

Brick manufacturers in northern India have reported a sharp rise in coal prices over the past year, with prices increasing from roughly INR 10,500/t to nearly INR 17,000/t. At the same time, many kiln operators complain that the available coal contains higher ash levels, forcing them to burn larger volumes of fuel to achieve the required heat levels.

The industry’s transition to zigzag kiln technology, which requires more consistent fuel quality, has made this problem even more severe. As higher-quality imported coal is absorbed by cement producers and large traders, smaller users such as brick kilns are often left with more expensive or lower-quality alternatives.

Outlook: NAPP coal likely to remain firm

The near-term outlook for US high-CV NAPP coal remains supportive. Three key factors are expected to continue supporting the market:

- Tight petcoke availability: As long as petcoke supply remains constrained and prices stay elevated, cement producers will continue using coal as a substitute fuel.

- Global energy uncertainty: Volatility in gas markets and geopolitical tensions are increasing the value of reliable, high-energy fuels.

- Limited prompt availability in India: Portside inventory is currently concentrated among a few buyers, which is keeping spot prices elevated. For these reasons, US NAPP coal is increasingly becoming the preferred substitute fuel in several industrial sectors.

In the current environment, the market is not simply trading coal. It is trading energy security and fuel flexibility. And for many buyers right now, high-CV US coal provides exactly that.

Leave a Reply