- Stalled exports from Middle East, rising freights drive up prices

- Indian buyers shift to US NAPP coal, raise domestic coal usage

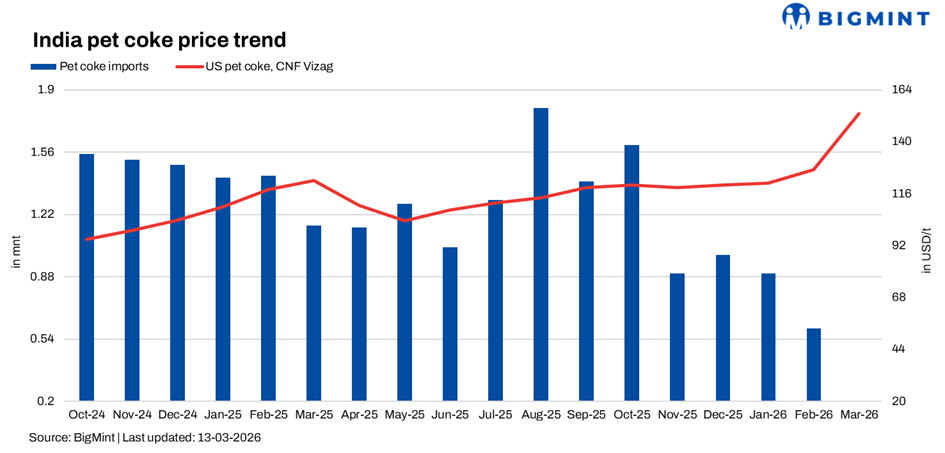

The global petroleum coke (petcoke) market has moved sharply higher over the past two weeks, as of 13 March 2026. Prices across most regions have increased significantly, but the rise has been driven mainly by supply disruptions and freight costs rather than stronger demand from end users.

In the United States, the main exporting hub for petcoke, prices surged quickly. High-sulphur petcoke with around 6.5% sulphur is now trading near $98-105/t FOB US Gulf, with some sellers unwilling to sell below $110/t FOB. Lower sulphur grades are even stronger, with 4.5% sulphur material around $107-110/t FOB.

This increase has pushed delivered prices in importing markets higher.

In India, delivered prices of high-sulphur petcoke are now widely quoted around $150-155/t CNF, compared with around $125-130/t just a few weeks earlier. Some cargo offers are even higher. Market participants reported mid-sulphur petcoke offered near $175/t CFR Kandla and high-sulphur cargoes around $165/t CFR Kandla for April loading.

Despite these rising offers, buying activity in India has slowed significantly. Cement producers and other industrial users are largely staying out of the market, relying on existing inventories while waiting to see if prices stabilise.

Other importing regions are seeing similar price increases.

In China, delivered prices vary widely depending on sulphur content. Low sulphur petcoke around 2% sulphur is trading near $195-200/t CFR, while 3% sulphur material is near $200-205/t CFR. Higher sulphur grades are cheaper, with 6.5% sulphur around $145-150/t CFR and 8.5% sulphur near $150-155/t CFR.

In Turkiye, delivered prices are around $132-133/t CFR for 5.5% sulphur and $127-128/t CFR for 6.5% sulphur.

In Europe, delivered prices into the Amsterdam-Rotterdam-Antwerp (ARA) region are roughly $135/t for 4.5% sulphur and about $126/t for 6.5% sulphur.

In Brazil, prices are similar, with 4.5% sulphur petcoke near $132-133/t delivered and 6.5% sulphur around $123-124/t delivered.

Freight costs have also increased sharply. Shipping petcoke from the US Gulf to west coast India is around $51-52/t, while freight to east coast India is roughly $54-55/t. Freight to China is around $58-59/t, and freight to Turkey is near $33/t.

These higher freight rates are pushing up delivered prices in all importing regions.

Supply risks, freight inflation distort trade flows

The current rally in petcoke prices is largely being driven by disruptions to supply and logistics linked to the ongoing conflict in the Middle East.

One of the biggest impacts has been on petcoke exports from refineries in the Arabian Gulf. Shipments from major refining hubs such as Jubail in Saudi Arabia have been disrupted because vessels must pass through the Strait of Hormuz, where shipping risk has increased significantly since the start of the conflict.

Several traders report that cargo loadings from some Gulf refineries have been delayed or suspended. At least one cargo originally scheduled for India is believed to be stuck in the Gulf because vessels are reluctant to enter the region.

Insurance costs for ships operating in the Gulf have also surged. War-risk premiums for vessels entering the region have increased sharply within a short period of time. At the same time, bunker fuel costs have increased as crude oil prices moved higher.

Because of these risks, many shipowners are avoiding the Gulf region entirely or demanding significantly higher freight rates.

This has created a major distortion in global petcoke trade.

Buyers who normally rely on Middle East supply are now turning to US-origin cargoes, which has tightened availability in the US export market and pushed prices sharply higher. However, this price rally is happening without a corresponding increase in demand.

In India, cement producers had already started reducing petcoke purchases when prices were around $122-130/t earlier in the year. At that time, several companies began switching to high-calorific US NAPP coal as an alternative fuel. Others increased the share of domestic coal blends in their fuel mix. Now that petcoke prices have moved above $150/t, buying interest has dropped even further.

In China, buyers are also resisting the higher prices. Many consumers believe current offers are too expensive relative to coal and are waiting for the market to stabilise. In Turkiye, the situation is similar. Petcoke is now significantly more expensive than coal on an energy-equivalent basis, which is pushing some cement producers to switch fuels.

Outlook: High offers but limited buying

The petcoke market is now entering a phase where prices are being driven more by cost pressures than by real demand. As long as shipping disruptions in the Gulf continue and freight rates remain elevated, exporters will struggle to offer cargoes at lower prices. This means offers are likely to remain firm in the near term.

However, demand from key importing regions — particularly India — has weakened sharply at current price levels. If cement producers and other industrial users continue to stay out of the market, actual transactions may remain limited even though offers are high. This creates a market where quoted prices are rising but real trade volumes are falling.

The next direction for the market will depend on three key factors: First, if vessel movement through the Strait of Hormuz improves, supply from Gulf refineries could return to normal and ease pressure on US exports. Secondly, shipping costs are currently one of the biggest drivers of delivered prices. Any decline in freight rates could quickly reduce landed costs. If high petcoke prices continue, many cement companies may continue shifting toward coal alternatives, which would limit demand.

For now, the global petcoke market remains highly volatile. Prices have moved higher due to supply disruption and freight inflation, but without stronger demand, the rally may struggle to sustain itself over the longer term.

Leave a Reply