- Global production exceeds consumption, pushing inventories higher across major producers

- Rising imports and comfortable stocks may cap rallies in India’s cotton market

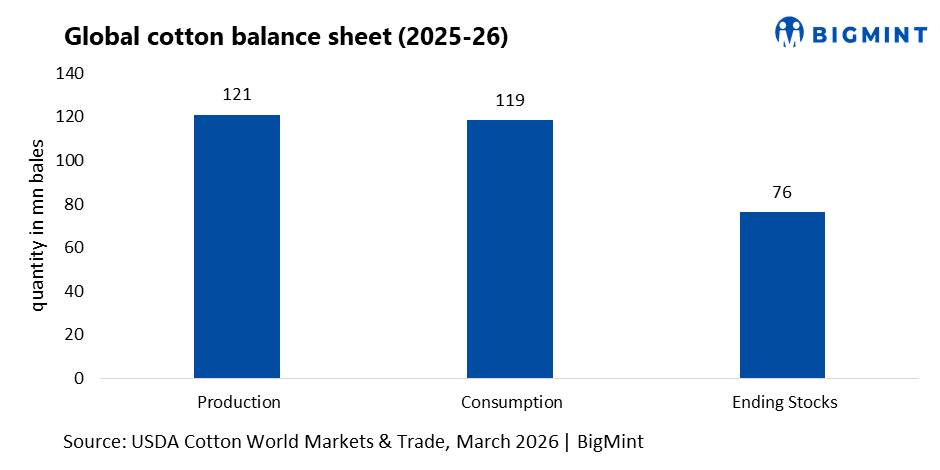

The global cotton market in the 2025/26 season is entering a phase of comfortable supply as production continues to outpace consumption, a development that could shape price behaviour and trade flows for major cotton-consuming countries such as India. According to the latest global outlook, world cotton production is projected to reach about 120.9 million bales, while global consumption is estimated at around 118.6 million bales, leaving the market with a modest surplus. As a result, global ending stocks are expected to rise to about 76.4 million bales, indicating that inventories across key producing nations are gradually building.

For global markets, this surplus is largely being driven by expanding output in Brazil and China, which together are offsetting production declines in some smaller producing countries. Brazil in particular continues to strengthen its role in the global cotton trade, with exports projected at around 14.5 million bales, making it one of the most dominant suppliers in the international market. This growing export presence means that Brazil increasingly influences global cotton price benchmarks and export competitiveness for other suppliers, including India.

From India’s perspective, the domestic supply-demand balance presents a slightly different picture. Cotton production for the 2025/26 season is estimated at around 23.5 million bales, while domestic consumption by spinning millers remains strong at approximately 25 million bales, highlighting the structural demand strength of India’s textile sector. Because mill demand exceeds domestic production, India is expected to increase cotton imports to about 4 million bales, a notable rise compared with previous projections. Lower import tariffs and competitive international prices are encouraging spinning mills to source cotton from overseas markets, particularly when domestic prices trade at a premium to global benchmarks.

At the same time, India’s cotton exports remain relatively limited at about 1.4 million bales, reflecting tighter domestic availability and stronger internal demand from spinning millers. With exports modest and imports rising, India’s cotton market is increasingly becoming consumption-driven rather than export-led. This dynamic means that mill buying behaviour and yarn demand will remain critical factors determining domestic cotton price trends.

International price indicators suggest moderate stability in the cotton market. Cotton futures on the Intercontinental Exchange (ICE) have recently traded near 64 cents per pound, while the global A-Index has moved higher to around 74.7 cents per pound, indicating a slight improvement in global price sentiment over recent weeks. However, the presence of comfortable global inventories continues to limit the scope for sharp price rallies.

For Indian ginners, spinning millers, and traders, the current market structure suggests a balanced but cautious outlook. Strong domestic mill consumption provides an underlying demand base for Indian cotton, but rising imports and ample global stocks could cap aggressive price increases. If international cotton prices remain stable and import parity continues to favour overseas purchases, Indian spinning mills may continue to diversify sourcing, which could keep domestic cotton prices within a relatively stable range.

Going forward, market participants will closely track global crop developments in Brazil and the United States, changes in import policies, and the pace of mill demand in major textile hubs. Any disruption in global supply or stronger textile demand could tighten the balance sheet quickly. However, under the current outlook of rising production and comfortable stocks, the cotton market may remain broadly range-bound, with domestic price movements in India largely guided by mill buying patterns and global price benchmarks.

Leave a Reply