- Renewables gain share in power mix, coal declines

- Ample supply pushes spot prices lower by 17% y-o-y

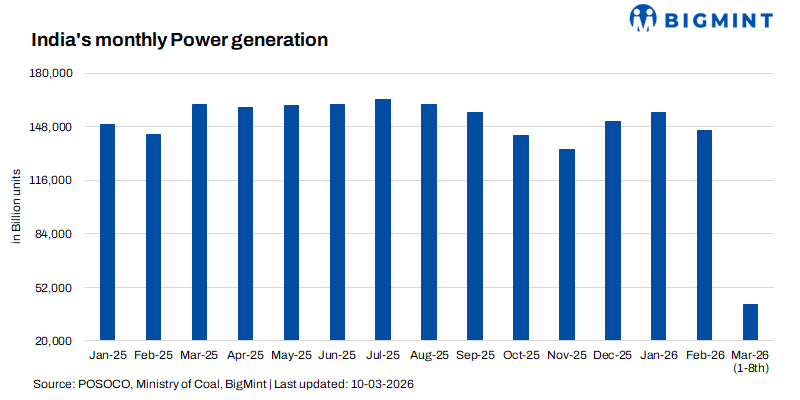

India’s electricity sector entered March 2026 with stable demand but a noticeably changing generation mix. Data for the first eight days of March shows that total power generation increased slightly y-o-y, while renewable energy strengthened its role in the grid. At the same time, spot electricity prices on the Indian Energy Exchange (IEX) declined sharply even as trading volumes surged, indicating that supply conditions remain comfortable.

Overall, the early March data suggests that the momentum observed in February — characterised by strong renewable output and stable thermal generation — has largely continued into the new month. The gradual onset of summer has also become evident, with the higher maximum peak indicating that electricity demand is gradually strengthening.

Generation trends: Modest growth but clear shift in fuel mix

Total electricity generation during 1-8 March 2026 reached 41,682 million units (MU) compared with 41,220 MU during the same period in 2025. This represents y-o-y growth of about 1.1%. Average daily generation increased slightly from 5,153 MU in early March 2025 to around 5,210 MU in 2026.

However, the most significant development is not the growth in total generation but the shift in the sources of electricity.

Renewable generation increased by 739 MU y-o-y, accounting for the majority of the incremental electricity supply during the period. As a result, the share of renewables in the generation mix rose from 13.6% to more than 15%.

Coal generation, by contrast, declined slightly in absolute terms, and its share of total generation dropped by nearly two percentage points. Despite this decline, coal continues to dominate India’s power sector, supplying nearly three-quarters of the country’s electricity.

February momentum continues into March

The strong renewable output seen in February 2026 has largely continued into March. Average daily renewable generation during the first eight days of March is almost identical to the February average.

The data shows that renewable generation remained consistently strong while coal generation increased slightly to meet incremental demand. This suggests that thermal plants continue to play an important balancing role in the system, compensating for fluctuations in renewable output and meeting peak demand.

Peak power demand continues to edge higher

National electricity demand also grew modestly during early March. During 1-8 March 2026, India’s national peak power demand ranged between 209,874 MW and 238,378 MW, with an average peak of around 226,450 MW.

In comparison, during the same period in 2025, peak demand varied from 212,879 MW to 233,009 MW, with an average of approximately 226,200 MW, indicating broadly stable average demand levels y-o-y despite a slightly wider peak range in 2026.

The highest demand recorded during the period was 238,378 MW on 7 March 2026, about 2.3% higher than the highest peak recorded during the same period in 2025.

Although the increase in average peak demand is relatively small, the higher maximum peak indicates that electricity demand is gradually strengthening as temperatures begin to rise ahead of summer.

Regional demand patterns

Electricity demand patterns vary significantly across India’s regions. In the northern region, peak demand generally occurs during the late morning between 9:30 AM and 10:30 AM, reflecting strong agricultural pumping and commercial activity.

The western region, which includes major industrial states such as Maharashtra and Gujarat, typically experiences peak demand during the late morning to early afternoon, driven by manufacturing and commercial load.

The southern region displays a more complex pattern. Early in the month, peak demand tends to occur in the morning, but as solar generation increases during the day, the system load curve shifts, producing a secondary peak in the mid-afternoon.

In contrast, the eastern and north-eastern regions exhibit a consistent evening peak between 6 PM and 8 PM, reflecting residential consumption and lighting demand after sunset.

IEX spot market: Lower prices but higher volumes

The Indian Energy Exchange provides another indication of changing market dynamics. During 1-8 March 2026, the Indian Energy Exchange (IEX) recorded a notable improvement in trading activity, even as prices softened.

The average market clearing price declined to INR 3,556/MWh, compared with INR 4,280/MWh during the same period in 2025, reflecting a 17% y-o-y decrease. In contrast, the average scheduled volume increased significantly to 166,046 MWh from 111,302 MWh last year, marking a 49% y-o-y rise in traded electricity volumes on the exchange.

Average spot prices fell sharply from INR 4,280/MWh in early March 2025 to about INR 3,556/MWh in 2026, a decline of nearly 17%.

At the same time, trading volumes on the exchange increased by almost 50%, indicating that distribution companies are increasingly using the spot market to optimise procurement and take advantage of lower prices.

Prices fell below INR 2,900/MWh on several days, reflecting abundant supply and the growing influence of renewable generation, which has near-zero marginal cost and therefore clears early in the merit order.

Outlook

The early March data highlights three important structural trends in India’s electricity sector. First, renewable generation continues to expand rapidly and is gradually increasing its share of the national power mix.

Second, coal remains the backbone of the system, providing the bulk of electricity and ensuring reliability during periods of high demand. Third, the power market is becoming increasingly dynamic, with rising exchange volumes allowing utilities to respond more flexibly to changing supply conditions.

As temperatures rise in the coming months, electricity demand is expected to strengthen further. India could therefore see new peak demand records during the summer of 2026, even as renewable generation continues to reshape the structure of the country’s power system.

Leave a Reply