- Hormuz tensions stall billet shipments to key GCC markets

- East Asian billet indications hold above $450/t FOB China

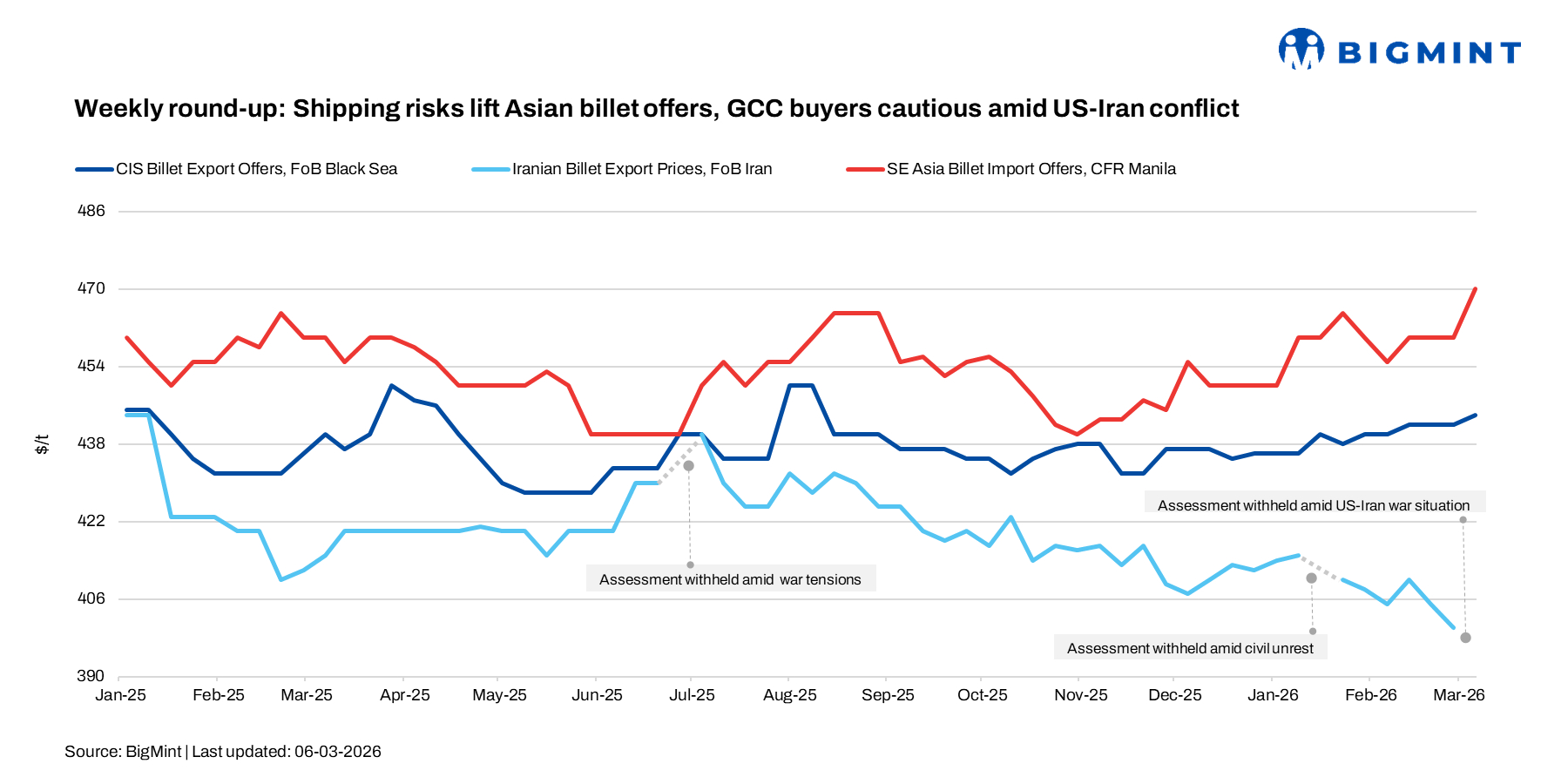

Rising Middle East tensions are disrupting key shipping routes around the Strait of Hormuz, lifting freight costs and supporting Asian billet export prices. Chinese mills raised 3sp billet offers by around $10-12/t w-o-w FOB amid supply concerns and firm raw material costs.

On the other hand, Turkish deep-sea scrap prices remained stable, with US HMS 80:20 at $370-375/t CFR and EU/Baltic at $368-375/t CFR. Around four to five deals were heard at $363-373/t CFR. The scrap-rebar spread held at $179-180/t, with rebar offers at $555-560/t FOB, while buying stayed cautious amid weak finished steel demand.

East Asian billet export market

Asian billet export offers continued to firm this week, supported by ongoing geopolitical tensions in the Middle East, expectations of stronger regional steel demand, and production curbs in China.

At the start of the week, Chinese mills offered 3sp billet at $445-450/t FOB for April–May shipment, up from $440-442/t FOB in the middle of last week. Market participants noted that producers have lifted offers and are not in a hurry to conclude sales as they assess the broader impact of the geopolitical situation. Rising raw material costs and exchange-rate volatility are also adding upward pressure, while China’s urban renewal stimulus and environmental restrictions in North China are expected to limit steel supply and support prices.

Towards the end of the week, indicative levels from East Asian suppliers were heard around $450/t FOB China and $470/t FOB Indonesia, while Philippines-origin material was reported near $470/t CFR for 5sp grade.

Offers from Indonesia’s Dexin Steel increased by $5/t to around $460-465/t FOB for April shipment, although no confirmed bookings were reported.

In Southeast Asia, 5sp billet was heard at $470-480/t CFR, slightly higher than around $465-466/t CFR last week. However, demand remained subdued, with many buyers adopting a wait-and-watch approach. Some market participants indicated that buyers could still accept higher prices to secure billets from China and Indonesia amid the absence of Iranian material due to the conflict.

Market participants noted that rising Gulf tensions have restricted vessel movements to parts of the Middle East, while the CIS region and Turkiye remain key destinations for Chinese billet, supported by rising coal and fuel costs that are lifting steelmaking expenses.

Traders reported increased buying interest from Thailand and Indonesia, which has also contributed to the recent firmness in Chinese billet prices. These markets were previously active buyers of Iranian semi-finished steel.

Industry sources estimate that close to 0.5 mnt of billets and slabs may currently be stranded in Iran, although this figure remains unverified.

A few cargoes were reported to have changed hands during the week. However, buyer sentiment remains divided. Some market participants believe the current price rise is temporary and could correct if the geopolitical situation eases, while others continue purchasing to keep mills operational despite higher billet costs.

GCC market

Geopolitical tensions in the Middle East have escalated following US-Israel strikes on Iran and subsequent retaliation, adding volatility to regional commodity markets and raising concerns for the GCC steel sector.

Market participants say the Strait of Hormuz–through which nearly 20% of global oil shipments pass– has become a major risk point. Security concerns have already pushed freight rates and war-risk premiums higher, with over 200 vessels reported waiting near the strait as shipping operators reassess movements.

“Freight costs are being recalculated, and vessels are waiting for clarity,” a UAE-based trading house source said, adding that steel markets usually react shortly after energy markets because logistics chains are closely interconnected.

Meanwhile, suppliers reported that the Chinese billet trade to the UAE and Saudi Arabia has largely stalled due to shipping disruptions. Exporters noted that vessel movements to the UAE are being affected, while shipments to Saudi Arabia via the Red Sea remain possible but involve higher risk and freight costs.

Outlook: Rising crude prices, potentially crossing $100/bbl, could lift fuel and electricity costs for GCC steel producers, tightening margins. While steel demand in the UAE and Saudi Arabia remains supported by infrastructure and government-led projects, sentiment has turned cautious, with some buyers delaying large purchases amid geopolitical uncertainty. Overall, the GCC steel market is facing higher cost volatility and logistical risks, prompting producers, traders, and buyers to adopt a wait-and-watch approach.

Leave a Reply