- LME stocks drop nearly 2.5%; market consolidates after recent highs

- MCX zinc tracks global weakness; SHFE prices ease marginally

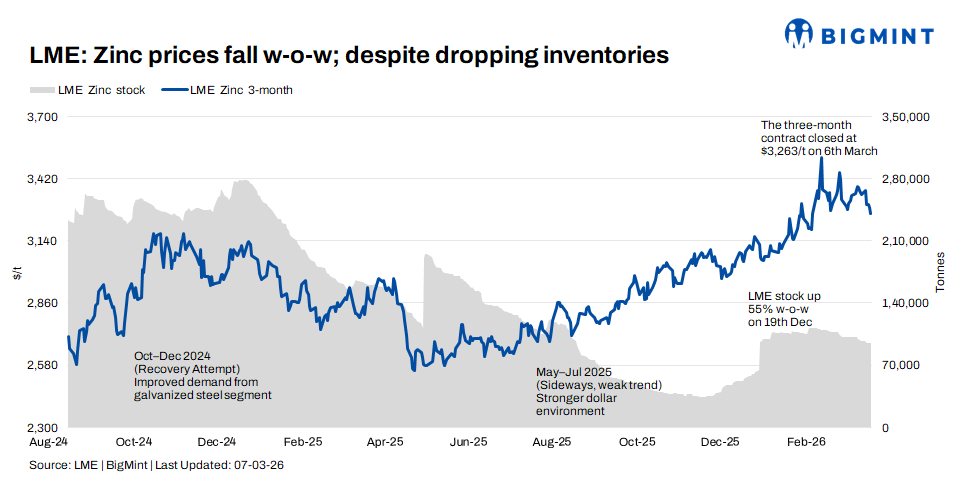

London Metal Exchange (LME) zinc prices traded lower in the week ended 6 March, retreating from early-week strength as profit-taking weighed on the market. Continued drawdowns in exchange inventories provided some underlying support, although prices slipped below the $3,250/t mark toward the end of the week.

Price trends

Zinc cash prices on the London Metal Exchange opened at $3,354/t on 2 March and initially moved higher before weakening through the remainder of the week. Prices fell to $3,238/t by 6 March, registering a decline of around 2.7% w-o-w compared with $3,327/t on 27 February.

The three-month contract followed a similar trend. Prices opened at $3,368/t on Monday and gradually declined to $3,263/t on Friday, compared with $3,348.5/t in the previous week, marking a drop of about 2.5% w-o-w.

The contract briefly attempted to hold above the $3,350/t zone early in the week but lost momentum amid broader base metals consolidation and cautious buying interest.

Inventory analysis

LME zinc inventories continued to decline during the week, reinforcing the broader trend of tightening visible supply.

Stocks fell from 97,350 t on 27 February to 94,975 t on 6 March, reflecting a drop of 2.4% w-o-w.

Inventories steadily declined through the week, dropping below the 95,000 t level by Thursday. The persistent drawdowns suggest ongoing physical offtake from exchange warehouses, although the pace of decline moderated compared with the previous week.

The continued reduction in visible stocks indicates underlying demand for refined zinc, even as futures prices experienced short-term corrections.

MCX zinc trends (2-6 Mar)

On the Multi Commodity Exchange of India, zinc futures broadly tracked the softer global cues.

The active April 2026 contract traded within a range of INR 323,200-333,700/t during the week. Prices opened at INR 331,200/t on 2 March and settled lower at INR 325,900/t on 6 March, reflecting a decline of around 1% w-o-w.

Trading activity picked up toward the end of the week, with volumes rising to 549 lots on Friday, while open interest increased from 143 lots at the start of the week to 696 lots, indicating fresh positioning amid the price correction.

Domestic demand from the galvanising sector remained stable but largely need-based.

SHFE zinc trend

On the Shanghai Futures Exchange, zinc prices showed a mild downward trend during the week.

SHFE zinc traded at around $3,530/t on 2 March before easing to $3,511/t by 6 March. The gradual decline mirrored movements on the LME, suggesting broadly aligned cross-market trends.

Chinese participation remained steady, although the absence of strong buying momentum limited upside movements in both markets.

Outlook

In the near term, zinc prices are likely to consolidate within the $3,200-3,250/t range.

Support may continue to emerge from the ongoing drawdown in LME inventories, which have now fallen below 95,000 t, indicating tightening visible supply. However, recent profit-taking and cautious buying interest could cap gains in the short term.

If inventories continue to decline toward the 90,000-92,000 t range, prices could attempt another move toward $3,350-3,400/t. Conversely, if stock drawdowns slow and broader base metals sentiment weakens, zinc may retest the $3,150-3,200/t support band.

Leave a Reply