- EU scrap prices supported by freight, geopolitical tensions

- Brazilian scrap prices stable amid gradual demand recovery

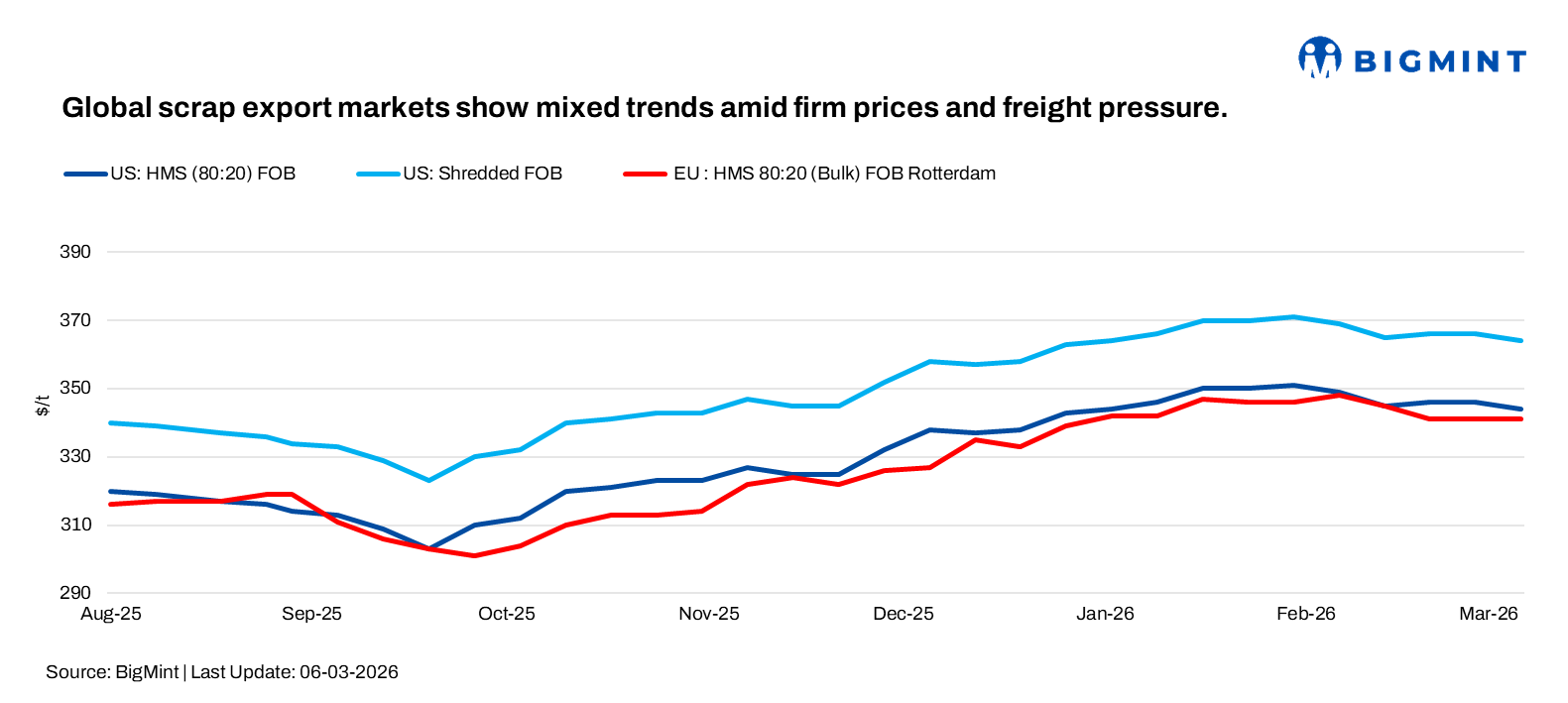

The global ferrous scrap export market showed mixed sentiment in early March, with supply improvements in some regions weighing on prices while freight uncertainty and geopolitical tensions continued to influence export trade.

Market participants across key exporting regions reported cautious buying activity as mills closely monitored freight costs, currency movements and demand conditions in major importing markets such as Turkiye, India, and Bangladesh.

US

Ferrous scrap sentiment remained under pressure in early March as improving weather increased supply while export demand stayed weak. March negotiations started with mills bidding mostly flat from February levels, with busheling around $445-450/t delivered Midwest and $450-455/t delivered Southeast, while shredded scrap hovered near $450/t.

Market participants stated that weak export demand, particularly from Turkiye, led to a domestic surplus of obsolete grades. HMS 80:20 import levels into Turkiye were indicated around $374-375/t CFR, while Indian buyers were comfortable near $350-355/t for HMS and about $365/t for shredded. Rising freight costs, up around $15/t from the US, also continued to complicate export trade.

Brazil

Brazil’s ferrous scrap market remained largely stable in the week to 6 March, as steelmakers gradually resumed purchases. HMS was heard around BRL 810-820/t ($154-156/t) FOT (Free on Truck), turnings scrap near Real 730-740/t ($139-140/t), and clean steel scrap about Real 900-910/t ($171-173/t) FOT.

Market participants noted slightly improved demand for ready-to-charge scrap, as mills preferred processed material to lower internal processing costs. Sentiment remained cautiously positive despite margin pressure.

Export negotiations also remained challenging, with Brazilian HMS around $285/t FOB and shredded near $305/t FOB, while Indian buyers continued pushing for lower prices.

Europe

European scrap export sentiment strengthened this week amid rising freight costs and ongoing Middle East tensions following the announcement of additional liner surcharges, with dock levels heard at Euro 260-270/t ($282-293/t).

A yard owner source noted that although European sellers are also facing elevated freight costs, the weakening euro is partially offsetting the impact, allowing exporters to better absorb higher logistics expenses.

Shredded scrap offers from the EU were heard around $378-385/t CFR Nhava Sheva/Mundra, while HMS 80:20 was indicated at $355-360/t CFR and HMS 90:10 near $368-370/t CFR.

Market participants stated that some EU/UK-origin shredded deals were reported around $390-395/t CFR Qasim, while recent offers were heard as high as $405/t. Participants also noted that a weaker euro against the US dollar may partly offset higher freight costs for exporters.

FOB assessments (Rotterdam, Europe)

- HMS 80:20 (Bulk): $341/t, stable w-o-w

Outlook

Looking ahead, export market participants expect global scrap trade to remain cautious in the near term. Freight volatility, geopolitical tensions and currency movements are likely to continue shaping export flows, while demand from key importing markets such as Turkiye, India and Bangladesh will remain a critical factor influencing price direction in the coming weeks.

Leave a Reply