- Improved steel demand lifts Chennai scrap

- Billet prices increase by INR 1,000/t w-o-w

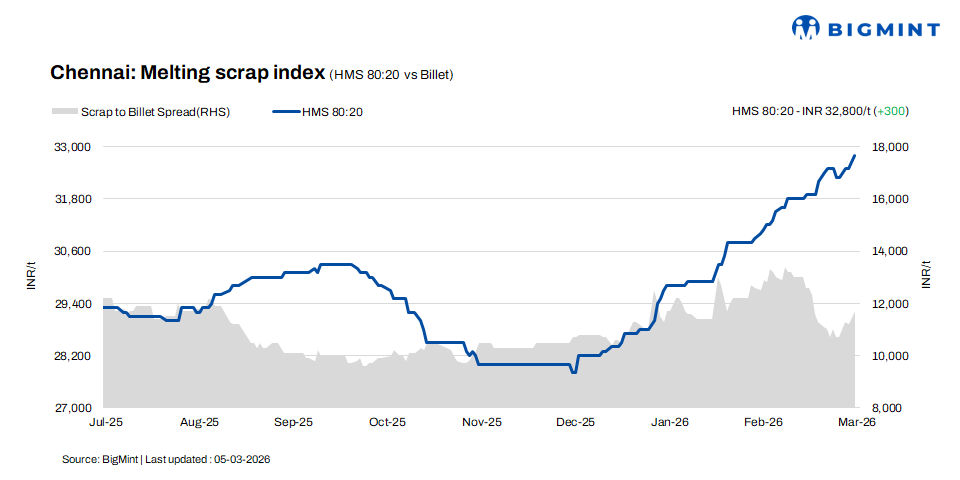

According to BigMint’s latest assessment, HMS (80:20) scrap prices in Chennai increased by INR 300/t on both daily and weekly bases, reaching INR 32,800/t. Billet prices rose by INR 800/t d-o-d to INR 44,500/t, registering a cumulative weekly increase of INR 1,000/t. Meanwhile, rebar prices climbed by INR 1,300/t w-o-w to INR 49,500/t, while also gaining INR 500/t on a daily basis. The stronger movement in billet and finished steel trades reflects improving market sentiment and better trading activity in the region.

Imported and domestic price trends

Market participants reported that Australia-origin imported shredded scrap was offered at $372-375/t CFR Chennai, while HMS (80:20) scrap was quoted at $355-357/t CFR. However, buyers were bidding $5-10/t lower than prevailing offers. Buying interest remained subdued as the strengthening US dollar continued to push up landed costs, keeping buyers cautious about fresh imported scrap bookings.

In the domestic market, HMS (80:20) scrap prices were assessed at INR 32,500-33,000/t for immediate payment, while transactions on extended credit terms were concluded at higher levels of INR 33,000-33,500/t. Overall market sentiment remained stable, supported by steady liquidity conditions. Both buyers and sellers adopted a cautious trading approach, balancing procurement volumes with payment terms and financing availability.

Buyer-supplier sentiments

According to a mill source, sponge iron prices are receiving support in the market as coal prices continue to rise amid the ongoing Iran-Israel conflict. The geopolitical tensions have led to volatility in global energy markets, pushing up input costs for steel producers. Iran is also a major exporter of sponge iron across the region. Due to the war-related disruptions, steel production in importing countries could be impacted, which may prompt these nations to explore alternative supply sources such as India.

Market sources stated that rising scrap offers have encouraged billet suppliers to increase prices to sustain conversion costs. Meanwhile, rebar demand has slowed temporarily due to Holi festivities, which have led to labour shortages and logistical constraints. Rebar inventory levels at major mills are currently around 15-20 days.

A scrap supplier indicated that HMS (80:20) prices were currently hovering in the range of INR 32,500-33,500/t, with variations largely dependent on payment terms and mill-specific volume requirements. The market is currently experiencing mild supply tightness due to the ongoing Holi festival, which has affected material flow and trading activity. Additionally, higher dollar rates and limited imported scrap bookings over the past few months have supported domestic scrap offers in the region.

Regional comparison

In the western India-based Jalna market, rebar prices increased by INR 800/t to INR 50,600/t, while billet prices rose by INR 200/t to INR 44,200/t. Meanwhile, HMS (80:20) scrap prices also edged up by INR 200/t to INR 32,300/t. Market participants reported improved trading activity in the finished steel segment over recent sessions, supported by better buying interest. Additionally, stable scrap availability has continued to support mill operations, allowing producers to maintain steady production levels in line with the prevailing regional demand and firm market sentiment.

Outlook

In Chennai, scrap prices are expected to trade within a narrow range with a slightly positive bias. Improving activity in semi-finished and finished steel markets may encourage mills to maintain regular scrap procurement. However, cautious purchasing strategies and short-term demand fluctuations could limit sharp price movements, keeping the market balanced with mild upward potential.

Leave a Reply