- Feedstock mix shifts from finished metal to intermediates

- New refinery ramp-up supports stronger anode demand

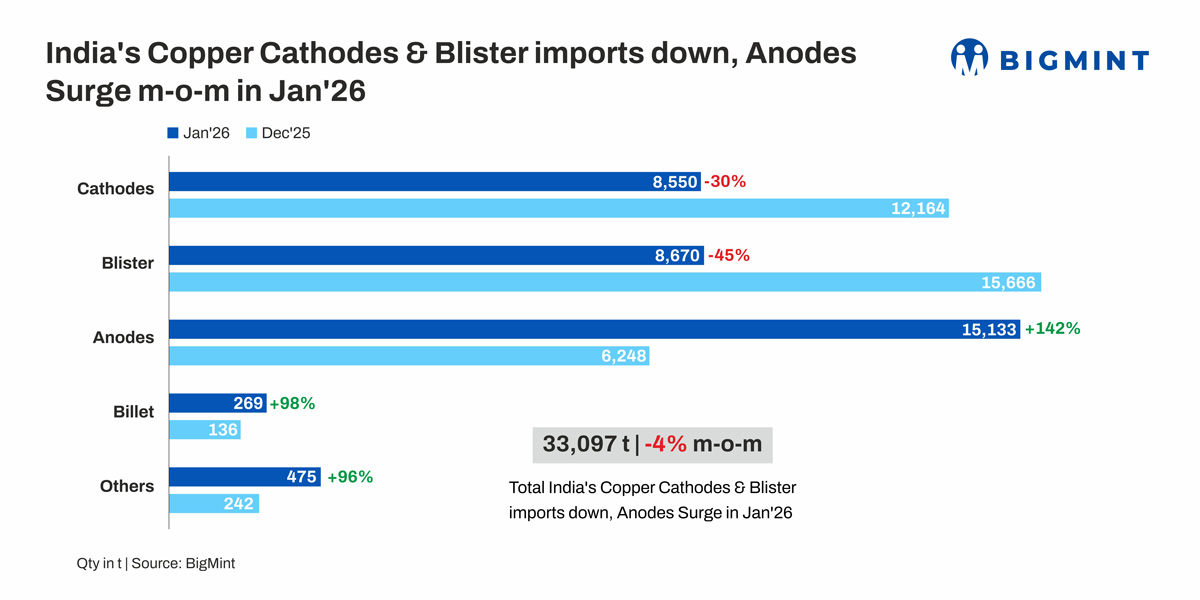

India’s copper import basket underwent a structural reshuffle in January 2026, with a clear shift away from refined cathodes and blister towards intermediate anode material. While total semi-finished imports declined modestly by 4% m-o-m to 33,097 t, the internal composition changed significantly — indicating feedstock optimisation rather than demand weakness.

Rising refined copper supply prompts 30% drop in cathode imports

Cathode imports fell 30% m-o-m to 8,550 t in January from 12,164 t in December. The decline was largely led by lower buying from integrated refiners and fabricators. Imports by Hindalco Industries dropped sharply, while Polycab India also moderated procurement.

The fall suggests that domestic refined availability improved sufficiently in December — when India’s refined copper output rose 36% m-o-m to 64,000 t — reducing the need for immediate spot cathode purchases in January. For integrated producers, importing cathodes when domestic output is stable offers limited economic advantage, particularly when London Metal Exchange (LME)-linked import parity remains elevated.

Additionally, continuous casting (CCR) rod manufacturers appear to have increased scrap blending ratios. Higher scrap intensity reduces cathode requirement per tonne of finished rod output, structurally lowering refined import demand. This blending strategy becomes more prominent when refined metal prices remain firm, as it protects conversion margins without affecting downstream supply commitments.

Blister imports plunge as smelting operations improve

Blister imports witnessed an even sharper contraction, falling 45% m-o-m to 8,670 t. The decline was led by lower volumes from Vedanta Limited and nil arrivals reported by Hindalco in January.

Blister is typically imported to bridge smelting gaps, supplement concentrate shortages, or maintain throughput during operational constraints. The sharp drop, therefore, signals improved smelting stability and better concentrate planning visibility among domestic players. The absence of blister imports at Hindalco indicates no immediate smelting shortfall, while Vedanta’s reduced intake points toward stable internal feed management rather than procurement disruption.

Anode imports surge as refiners shift to intermediate feedstock for domestic processing

In contrast, anode imports surged 142% m-o-m to 15,133 t, marking the most notable shift in the January trade data.

Hindalco’s anode imports jumped 170% to 7,674 t, while Vedanta nearly doubled its intake. The rise in anodes alongside falling cathodes clearly indicates substitution — refiners replacing finished metal imports with intermediate feedstock for domestic processing.

Unlike cathodes, anodes allow refiners to utilise electrolytic refining capacity internally and retain refining margins instead of paying embedded premiums in finished metal imports. This strategy improves operational flexibility, as anodes can be processed in phases based on downstream dispatch schedules, supporting better inventory control and working capital management.

Another important development in January was the entry of Adani Enterprises into the anode import market. The company has begun procuring anodes, adding incremental volume to the segment. With Adani scaling up its copper operations, its anode buying contributed to the overall surge in intermediate imports.

Adani’s participation is structurally significant. As new refining capacity ramps up, initial feedstock requirements are often met through semi-processed material such as anodes before long-term concentrate linkages stabilise. This dynamic naturally increases anode trade flows during commissioning and early ramp-up phases.

The bottom line

The simultaneous decline in blister and rise in anodes also reflects strategic feed mix balancing. Blister carries smelting economics embedded in its pricing, whereas anodes provide greater refining-stage control. By increasing anode intake while reducing blister dependency, refiners are effectively shifting more value addition domestically within the refining stage rather than relying on externally smelted material.

Importantly, the overall decline of just 4% in semi-finished imports confirms that January was not a demand contraction story. Instead, it was a composition shift: Refined cathodes reduced due to improved domestic output and higher scrap blending. Blister declined amid stable smelting operations. Anodes surged as refiners optimised feedstock mix and new capacity (Adani) entered procurement.

The data, therefore, points toward refinery utilisation maximisation and feedstock restructuring, rather than weakness in downstream copper demand.

Going forward, if domestic refined output remains steady and new capacity continues ramping up, India’s copper import basket may stay tilted toward intermediate feedstock such as anodes instead of finished cathodes. This would indicate deeper integration of refining operations and stronger internal margin capture across the domestic copper value chain.

Leave a Reply