- Chinese thermal coal prices rose post-holiday on supply fears

- Demand cautious despite tight inventories and measured mine recovery

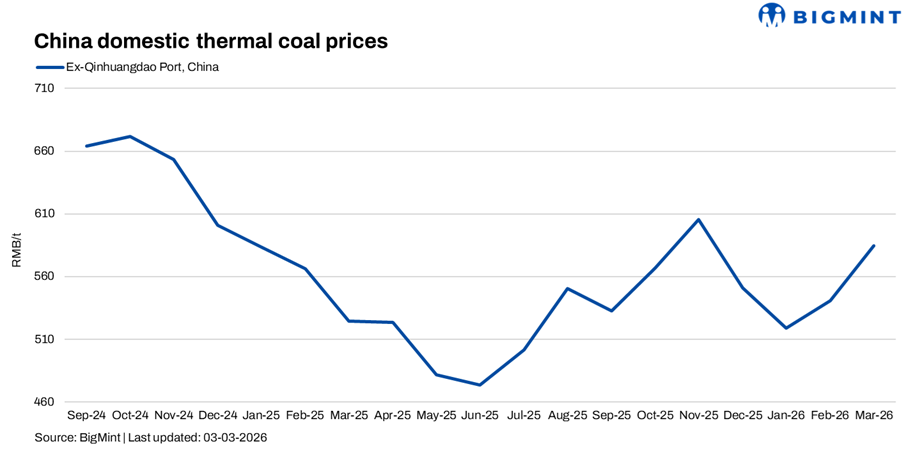

Mysteel Global: China’s thermal coal market extended its upward trend in the first working week (February 2428) after the Chinese New Year (CNY) holiday, driven primarily by concerns over supply shortages linked to Indonesia’s planned production cuts. Post-holiday restocking, particularly for high-quality cargoes, also supported price gains.

As of February 28, Mysteel assessed the benchmark 5,500 kcal/kg NAR thermal coal at northern transfer ports at Yuan 748/tonne ($109/t) FOB with VAT, up from Yuan 721/t on February 14, the last working day before the holiday. Lower grades saw larger increases over the same period, with 5,000 kcal/kg and 4,500 kcal/kg NAR grades both rising Yuan 30/t to reach Yuan 671/t and Yuan 584/t, respectively.

At northern ports, trading activity remained limited, largely confined to high-quality, high-priced cargoes. Some power utilities purchased coal for blending with lower-quality materials, while a few speculative traders restocked in anticipation of further price rallies.

Most domestic power plants stayed on the sidelines, as they faced little immediate pressure to replenish inventories. Mysteel’s February survey of 493 power plants across China indicated that their combined coal stocks were sufficient for 24.9 days of operation on average, well above the critical threshold of 15 days. Coal demand from non-power sectors has also yet to recover, despite expectations of industrial activity resumption in the near term.

Contributing to the post-holiday price rally was mainly the firmer sentiment since Indonesia announced annual production cuts for 2026. Uncertainty over quota allocations had persuaded many Indonesian miners to withhold spot cargoes, pushing seaborne coal prices higher and eroding Indonesian coal’s price advantage against Chinese domestic coal. Consequently, Chinese buyers turned to domestic spot coal, boosting portside prices.

Northern port inventories remained relatively tight, supporting market confidence. As of February 28, combined coal stocks at the eight northern Chinese ports tracked by Mysteel totaled 23.09 million tonnes, slightly up from 22.68 million tonnes on February 14 but 15.9% below year-ago levels.

Although mines in China’s major producing regions gradually resumed operations after the holiday, effective supply recovery remained measured. Over February 20-26, Mysteel’s survey of 462 thermal coal mines showed their daily production averaged 4.91 million tonnes/day, up 11.7% from a week earlier but still below the typical level of 5.5 million t/d.

In the seaborne market, Indonesian thermal coal prices increased last week, buoying prices of Australian and Russian cargoes as well. As of February 28, Mysteel assessed Indonesian 3,800 kcal/kg NAR coal at $61/t FOB Kalimantan, up from $57/t on February 14. Assessment for Australian 5,500 kcal/kg NAR coal increased $6.1/t to $86.1/t FOB, while Russian 5,550 kcal/kg NAR coal rose from $85/t to $91/t on a CFR China basis.

The U.S.-Israel strike on Iran on February 28 sent shockwaves through global energy markets. Analysts forecasted significant increases in oil and gas prices, with Brent crude, standing at $73/barrel on February 27, potentially surpassing $100 in the near term. This could indirectly support coal demand for industrial use, as elevated oil prices make coal-based chemical production more cost-effective.

However, coal prices remain less sensitive than oil and gas. Market fundamentals and domestic energy policy will continue to drive trends, and prices could face downward risks if China decides to increase domestic supply, sources cautioned.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply