- Global aluminium output rises 0.3% m-o-m

- Global refined copper output up 4.2% m-o-m

LME base metals traded on a mixed note on a w-o-w basis during the latest week, reflecting selective buying interest across the complex. Aluminium prices increased 2.53% to $3,157/t, while nickel rose 1.93% to $17,685/t. Copper recorded the strongest gains, climbing 4.82% to $13,440/t. In contrast, zinc slipped 0.49% to $3,327/t, and lead declined 1.08% to $1,928/t.

On the inventory front, trends were also mixed. Copper stocks rose sharply by 7.89% to 253,700 t, and nickel inventories edged up 0.09% to 287,976 t. Meanwhile, aluminium stocks fell 2.10% to 465,550 t, zinc inventories dropped 4.16% to 97,350 t, and lead stocks declined 0.36% to 286,100 t.

Aluminium

India’s imported aluminium scrap prices witnessed a positive trend w-o-w on 28 February 2026, following gains in LME aluminium prices.

As per BigMint’s assessment for CFR Nhava Sheva deliveries, UK-origin Zorba 95-5 firmed sharply by $110/t to $2,610/t, and Taint Tabor Clean (Middle East) advanced $85/t to $2,585/t.

Domestic aluminium prices in India increased w-o-w on 26 February, mirroring gains in aluminium futures on the London Metal Exchange (LME) and the Multi Commodity Exchange (MCX), amid ongoing global supply concerns.

As per market assessment, domestic aluminium ingot prices in Delhi NCR increased by INR 4,000/t, or 1%, w-o-w to INR 313,000/t.

Additionally, Global primary aluminium production stood at 6.32 mnt in January 2026, marking a 0.3% m-o-m increase from 6.30 mnt in December 2025.

Copper

Imported copper scrap prices in India moved sharply higher w-o-w, as assessed on 28 February, tracking a strong rebound on the London Metal Exchange (LME). Firm global cues, renewed Chinese buying after the holiday break and active short covering lifted both import offers and domestic scrap prices.

According to BigMint’s assessment, Middle East-origin Birch Cliff scrap was assessed at $12,355/t CFR Mundra, up by 4.4% w-o-w, while armature scrap prices were up by 2% w-o-w to INR 1,132,000/t ex-Delhi.

Domestic brass honey scrap prices increased w-o-w. BigMint assessed brass honey, ex-works Jamnagar, Gujarat, at INR 712,000/t, marking a rise of INR 29,000/t compared to INR 683,000/t last week.

Additionally, The International Copper Study Group (ICSG) reported preliminary data for CY’25, showing that global refined copper production grew by around 4.2% y-o-y, supported by a 3.9% rise in primary production (from ores via electrolytic and electrowinning processes) and a 5.8% increase in secondary production (from scrap).

Zinc

India’s zinc scrap and dross prices moved up w-o-w on 28 February 2026, supported by sustained procurement from local processors and firm global cues. Strength on the London Metal Exchange (LME) lent support to import bookings, while domestic trading activity improved across key consumption centres.

BigMint assessed zinc diecast scrap (Middle East origin) at $2,670/tonne (t) CFR west coast India, up $30/t w-o-w on steady inquiry levels.

HZL on 26 February increased its zinc ingot prices by INR 3,800/t ($42/t) to INR 342,000/t ($3,773/t) compared to the previous revision on 23 Feb’26.

Additionally, in 2025, the global refined zinc market recorded a 33,000 t deficit. Reported inventories across the London Metal Exchange (LME), Shanghai Futures Exchange (SHFE) and market participants declined by 77,000 t, ending the year at 739,000 t.

Lead

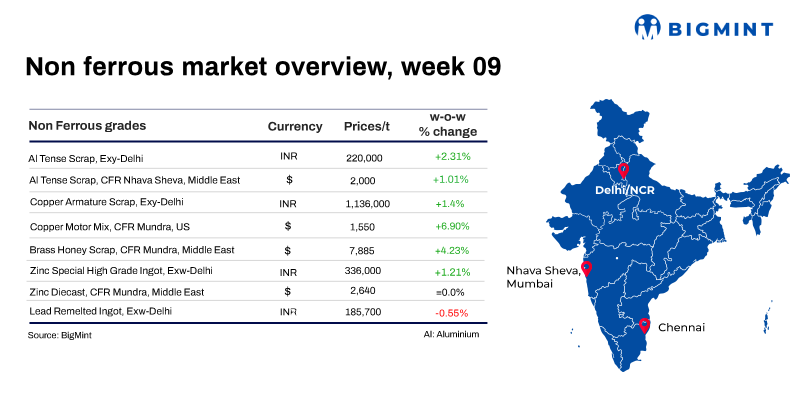

Domestic primary lead ingot prices stood at INR 196,200/t, down by 0.25% w-o-w, while re-melted ingots stood at INR 185,700/t, down by 0.5% w-o-w.

Meanwhile, HZL’s on 26 February increased its lead ingot prices by INR 300/t ($3/t) to INR 207,800/t ($2,287/t) compared to the previous revision on 23 February.

Leave a Reply