- LME stocks fall 1.7% w-o-w

- Smelter restarts will tighten supplies further

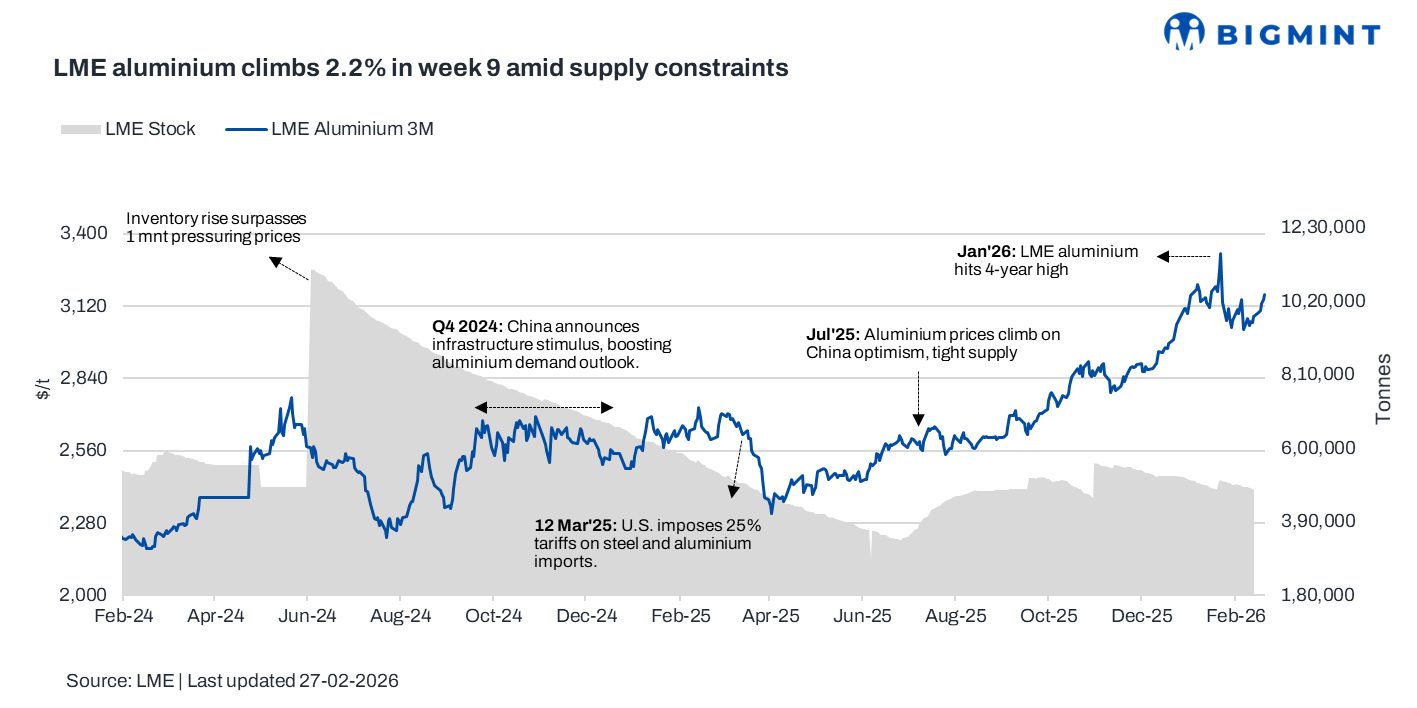

Benchmark aluminium prices on the LME rose 2.20% in the week ended 27 February 2026. LME aluminium prices rose w-o-w, supported by production disruptions at Century Aluminum, planned smelter restarts, tight near-term supply expectations, and cautious investor sentiment amid potential mid-year Fed rate adjustments.

Pricing, inventory trends

LME aluminium averaged $3,129/t during the week, up $68/t or 2.20% w-o-w. The week opened near $3,097/t, strengthened to $3,132/t mid-week, and closed at $3,165/t.

Meanwhile, LME aluminium stocks fell 1.7% w-o-w to 465,550 t from 473,550 t, reinforcing the narrative of constrained supply and underlying market tightness.

Factors impacting prices

LME aluminium prices rose w-o-w, supported by a combination of supply adjustments and positive market sentiment. Recent corporate updates highlighted production disruptions and subsequent capacity resumption plans, which reinforced short-term supply tightness. Century Aluminum’s Q4 2025 output fell 14% q-o-q due to equipment issues at its Iceland smelter, while the Mt. Holly smelter’s idle 50,000 t capacity is expected to restart in April, gradually reaching full production by Q2 end. These developments, coupled with the Iceland smelter’s earlier-than-expected ramp-up, underpinned market expectations of tighter near-term availability.

On the demand side, robust growth in China’s motorcycle industry added further support. January production and sales rose sharply y-o-y and m-o-m, while export volumes reached multi-year highs, highlighting resilient downstream consumption and export demand.

Additionally, market participants remained attentive to broader macroeconomic cues. While the probability of a March Fed rate cut is low, expectations of potential easing by mid-year kept investor sentiment cautious but supportive, encouraging fund flows into industrial metals like aluminium. Together, these supply constraints and demand signals contributed to LME aluminium’s w-o-w price gains.

Outlook

Aluminium prices are likely to remain supported near-term as smelter restarts at Mt. Holly and Iceland tighten the supply-demand balance. However, elevated LME stocks and cautious investor positioning amid muted Fed easing expectations may cap gains. Market attention will focus on actual production ramp-ups, oil price trends, and downstream industrial activity to gauge whether the current rally can sustain into Q2.

Leave a Reply