- US cargo diversion tightening non-US spot availability

- Strong China demand supporting prices above $13,000

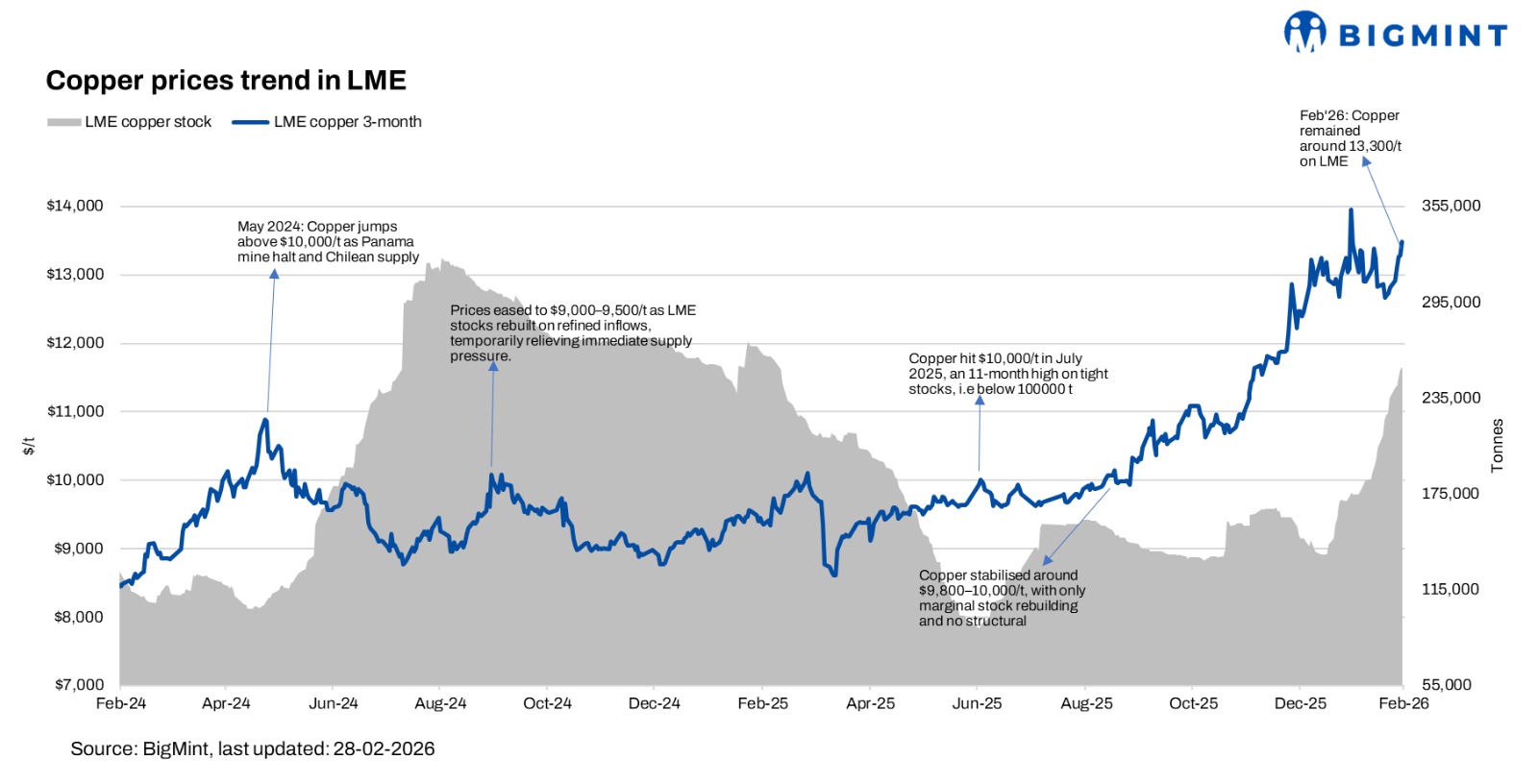

Copper futures on the London Metal Exchange (LME) climbed up to $13,340/tonne (t) on 27 February from $12,820/t on 20 February, marking an increase of roughly 4.1% w-o-w.

The upward move was largely driven by a combination of tightening near-term availability and improved macro sentiment. Market participants noted that buying interest picked up after China returned from the Lunar New Year holidays, with downstream fabricators and smelters gradually resuming operations.

Even when exchange inventories are at all-time highs, copper prices can still find support from physical demand and regional buying activity. According to recent LME data, copper stocks in London Metal Exchange warehouses climbed to around 243,000-249,000 tonnes, the highest since March 2025, and have risen roughly 70-80% so far this year.

Market participants have been redirecting refined copper cargoes to the US in anticipation of potential trade policy changes, including tariff-related developments. When buyers expect possible import duties or policy shifts, they often accelerate shipments to secure material ahead of any official announcement. This front-loading of cargo creates stronger short-term demand for US-bound metal.

As a result, material that would typically flow to Asia or Europe is being diverted, reducing spot availability in those markets. This reshuffling of trade flows has led to tighter physical supply conditions outside the US.

Global copper surplus widens in CY25; India output up 19% on Adani ramp-up

The International Copper Study Group (ICSG) reported preliminary data for CY’25, showing that global refined copper production grew by around 4.2% y-o-y, supported by a 3.9% rise in primary production (from ores via electrolytic and electrowinning processes) and a 5.8% increase in secondary production (from scrap).

India recorded a 19% increase in refined copper production, supported by improved operating capacity rates and the ramp-up of the Adani refinery.

Chilean refined copper production declined by 10%, with electrolytic output (from concentrates) down 16% due to smelter maintenance shutdowns, and electrowinning (SX-EW) production decreasing by 6.8%.

Global secondary refined copper production (from scrap) increased by 5.8%, largely driven by growth in China.

Outlook

Leave a Reply