- Several deals closed for Mar, most miners’ remaining EC volumes booked

- Limited spot availability supports prices, but weak steel prices cap upside

Iron ore prices in the Odisha region remained firm this week, supported by active trading through direct sales and auctions conducted by private miners. Market participants noted that buying interest improved as steelmakers and traders secured cargoes for March delivery, particularly with the expiration of environment clearance (EC) limits for several major miners approaching.

Price update

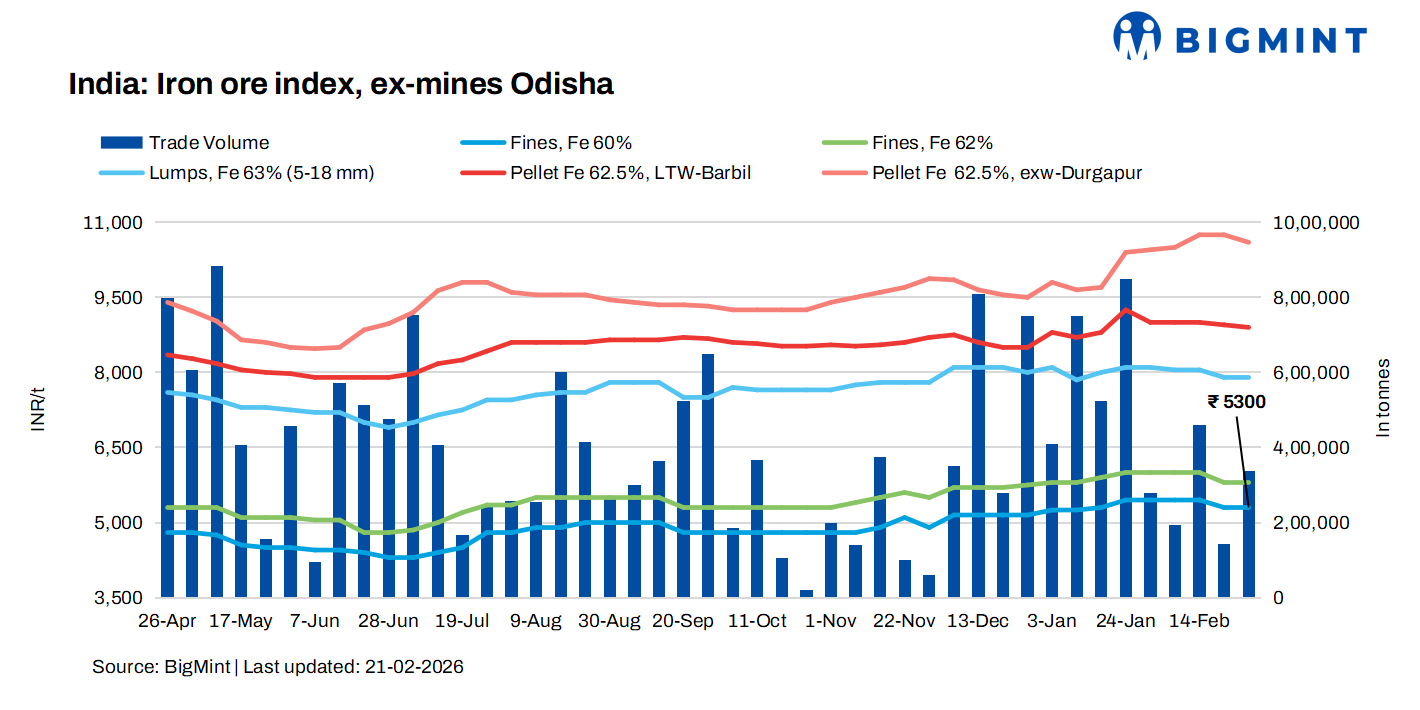

BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,800/t ($64/t) ex-mines on Saturday (28 February). BigMint recorded deals for around 336,000 t this week, concluded directly by steelmakers with private miners and traders. Meanwhile, around 214,130 t of iron ore (Fe 56.5-63%) were booked via auction this week at INR 3,800-7,900/t ex-mines basis, including royalty.

Market highlights

A trader said, “Buyers are actively booking March material as many large miners are nearing their EC limits. There is limited availability in the spot market, which is keeping prices supported.” Several advanced deals for March were reportedly concluded to ensure supply continuity.

However, sentiment in the downstream segment remained cautious. A steelmaker highlighted that the continuous decline in sponge iron and semi-finished steel prices has created cost pressure. He added, “Iron ore prices are not aligning with the fall in billet and sponge iron prices. Current levels are slightly higher for trade, and we expect some correction if finished steel demand does not improve.”

Meanwhile, a few buyers raised concerns over the actual grade of material in certain deals from prominent miners, stating that quality variations at prevailing price levels are being closely monitored.

On the supply side, miners have largely kept their offers unchanged, with most reporting that their remaining EC volumes are fully booked. A private miner stated, “Our sales are complete for the current EC period, and we are not offering discounts for the remaining trades.”

Steelmakers continue to procure through auctions on a need-based basis to manage raw material inventory amid volatile downstream markets.

Market participants expect iron ore prices in Odisha to remain stable in the near term, supported by limited availability but capped by weakness in sponge iron and semi-finished steel prices. Additionally, low-grade exporters remain largely inactive in the domestic market due to non-viable export realisations in the seaborne market.

Factors affecting iron ore prices

Pellet prices fall w-o-w: Pellet (6-20 mm, Fe 62.5%) prices in Odisha’s Barbil inched down by INR 50/t w-o-w to INR 8,900/t ($98/t) loaded to wagon on 27 February. Pellet (Fe 62.5%, 6-20 mm) prices in Durgapur fell by INR 150/t to INR 10,600/t ($116/t) exw.

Sponge iron prices down w-o-w: According to BigMint’s assessment, sponge iron C-DRI (FeM 80%) prices in Rourkela inched down by INR 50/t w-o-w to INR 27,000/t ($296/t) on 28 February.

Billet prices fall w-o-w: Meanwhile, steel billet (100*100 mm) prices in Rourkela declined by INR 900/t ($10/t) w-o-w to INR 39,100/t ($429/t) on 21 February.

Rationale

- T1- Six (5) deals for Fe 62% fines were recorded in the publishing window, and one (1) were considered for price computation. These were given 50% weightage for index calculation.

- T2 – BigMint received eighteen (18) offers and indicative prices under the T2 category (offers, indicative, and bids) in this publishing window. Eighteen (18) were taken into consideration and given 50% weightage. To check BigMint’s iron ore assessment, pricing methodology, and specification document, click here.

Outlook

Iron ore prices in Odisha are expected to remain stable in the near term. Private miners are likely to finalize additional deals without offering discounts, due to the limited availability of material.

Leave a Reply