- Finished steel demand weakens, mills make limited inquiries

- Semis, finished steel prices drop by around INR 900/t w-o-w

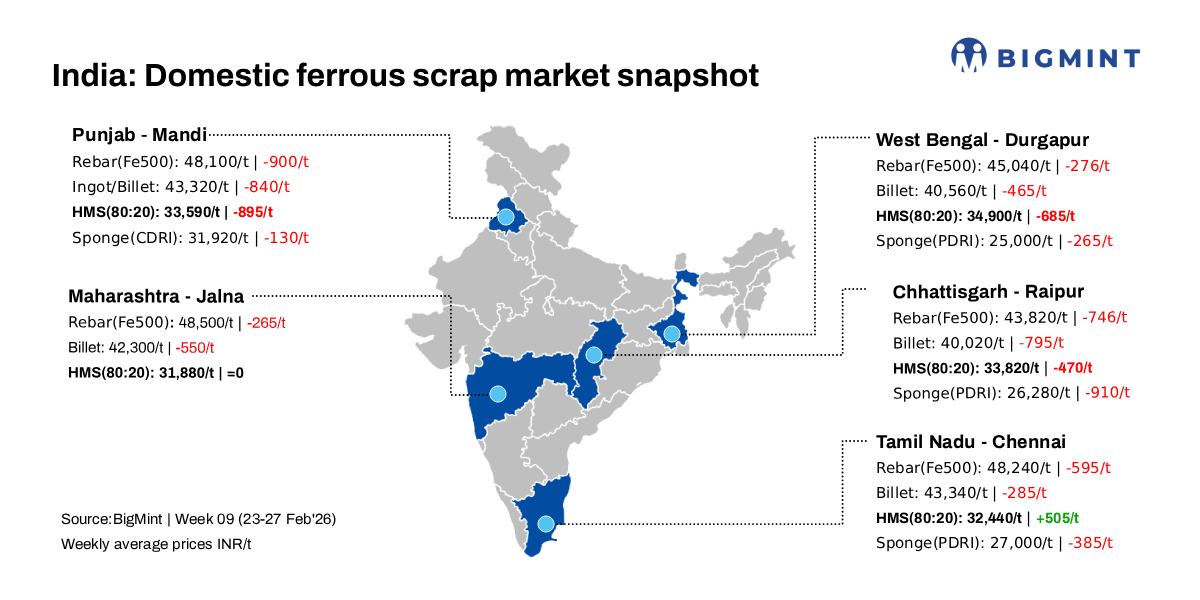

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, declined by INR 300/tonne (t) d-o-d to INR 36,500/t DAP on 27 February 2026. Meanwhile, the index decreased by INR 855/t w-o-w.

Steel market activity in Mandi Gobindgarh stayed weak, with scrap prices declining by INR 855-900/t. Inquiries remained limited, as major mills procured limited volumes amid excess arrivals of domestic scrap from neighbouring states and sluggish demand for finished steel, building inventory pressure for both raw materials and finished products.

Demand for imported scrap remained muted due to the availability of cheaper domestic alternatives.

Alternative raw material prices

Sponge iron (CDRI) prices in Mandi Gobindgarh decreased by INR 100/t to INR 31,900/t (DAP). Prices dipped by INR 130/t w-o-w.

Steel-grade pig iron prices in Ludhiana remained stable d-o-d at INR 39,300/t (DAP), while recording a w-o-w decrease of INR 610/t.

Steel market dynamics

In the semi-finished steel segment, ingot prices in Mandi Gobindgarh fell by INR 350/t d-o-d to INR 43,000/t DAP, while prices across other major production hubs dropped by INR 100-550/t over the same period. On a w-o-w basis, ingot prices in Mandi slid by INR 820/t.

Rebar (Fe 500) prices in Mandi Gobindgarh fell by INR 100/t d-o-d to INR 47,900/t. On a w-o-w basis, prices significantly decreased by INR 900/t. HR strip (patra) prices also softened by INR 925/t w-o-w.

Overview of Hyderabad market

In Hyderabad, billet prices declined by around INR 500/t d-o-d to INR 41,000/t, primarily due to subdued demand for finished steel products in the local market. The slowdown in construction activity and cautious procurement by buyers weighed on overall steel consumption. Additionally, easing sponge iron prices pressured billet rates, as lower input costs have prompted mills to adjust their offers downward. The combined impact of weak downstream demand and softer raw material prices resulted in a bearish trend in the billet segment during the week.

HMS (80:20) prices in the region fell by INR 100/t to INR 31900/t (DAP), while w-o-w, prices dipped by INR 300/t.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 6,300-6,600/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $344-$345/t, approximately INR 33,712/t (inclusive of freight). HMS (80:20) prices in Mumbai fell by INR 400/t d-o-d to INR 33,100/t DAP. Indicative prices of shredded from Europe stood at $366/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 13,950/t.

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply