- Central India records steepest declines of INR 300-450/t d-o-d

- Billet, finished steel price volatility weighs on sponge iron demand

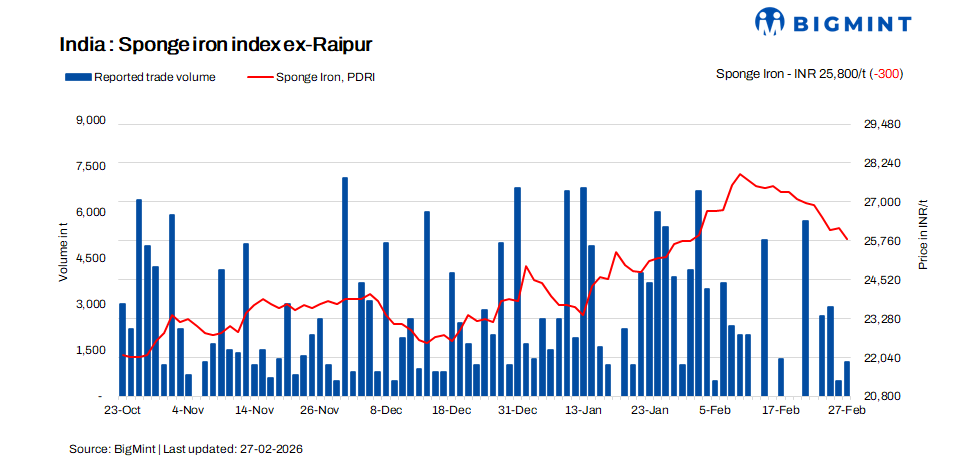

Indian sponge iron (DRI) prices declined by INR 50-450/t d-o-d on 27 February 2026 across major producing regions, as subdued demand and cautious buying behaviour dominated market activity.

Central India witnessed the sharpest corrections of INR 300-450/t, amid weak finished steel movement and sluggish billet demand. Producers in the region trimmed spot offers to stimulate enquiries; however, buyer response remained limited as mills restricted procurement to immediate requirements only.

Across pan-India markets, participation remained thin. Although sellers showed greater flexibility in negotiations, deeper discounts were largely avoided as producers sought to protect margins amid compressed conversion spreads and volatile finished steel prices.

Market participants noted that uncertainty in billet and rebar price direction continued to influence buying decisions. A Raipur-based furnace operator said, “Until billet and finished steel prices stabilise, sponge iron consumption will remain cautious.”

Daily trade volumes were estimated at around 5,600 t, reflecting limited engagement from both traders and end-users. Most bookings were concluded at lower price levels, underscoring prevailing bearish sentiment and weak liquidity in the market.

Rationale

Prices have been derived based on transactions, offers, bids, and indicative price data sets. Transactions are considered as T1 and given a weightage of 50%, whereas other data sets are considered as T2 and given a weightage of the balance 50%.

Click here for detailed methodology

Leave a Reply