- Uncertainty continues around Indonesian production curbs

- Indonesian index prices rise on tight supply, firmer demand

Indian portside prices of Indonesian-origin thermal coal increased w-o-w during the week ended 27 February 2026. The uptrend was primarily driven by supply-side tightness in Indonesia amid continued regulatory uncertainty surrounding Indonesia’s Rencana Kerja and Anggaran Biaya (RKAB), or Mining Work Plan and Budget.

Portside price movements

Portside thermal coal prices across key Indian ports continued their upward momentum during the week, reflecting tightening spot availability and sustained buying interest. According to BigMint’s latest assessment, 5,000 GAR coal prices advanced by INR 50/t w-o-w to INR 8,350/t at Kandla and INR 8,250/t at Vizag.

Similarly, 4,200 GAR coal prices increased by INR 150/t w-o-w to INR 6,450/t at Kandla and INR 6,500/t at Vizag. Lower-grade 3,400 GAR coal also rose by INR 50/t w-o-w to INR 4,900/t at Navlakhi.

Indonesian miners still await clarity on CY’26 output, export curbs

The continued uncertainty surrounding RKAB approvals in Indonesia kept market participants uncertain about production and export restrictions. A few miners who had exhausted their first-quarter quota were heard not offering material for exports.

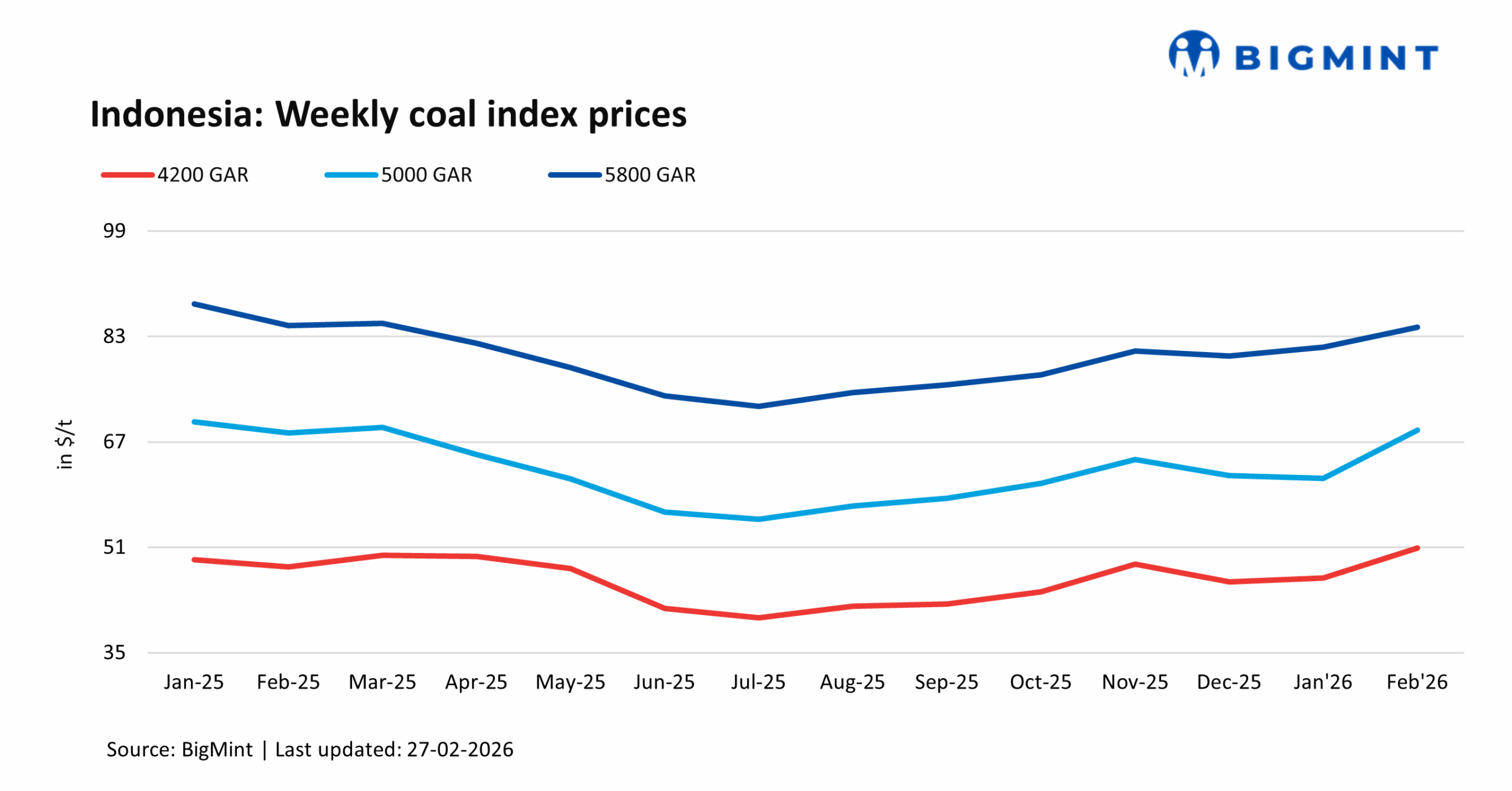

Indonesian benchmark trends: Gradual upward correction

Indonesian weekly benchmark prices also recorded modest w-o-w gains. During the period, 5,800 GAR coal prices increased by $1/t, 4,200 GAR by $2.6/t, and 3,400 GAR by $0.7/t. The relatively stronger gains in mid-grade benchmarks align with tightening supply dynamics and firmer buying interest from price-sensitive markets such as India. The benchmark movement further reinforces the supportive cost push observed at Indian ports.

Outlook

Indian portside thermal coal prices are likely to maintain upside, supported by Indonesian supply uncertainty and selective restocking by power producers. However, improved domestic supply, ample offered volumes at domestic auctions, or potential clarity on Indonesian exports are likely cap gains. Overall, prices are expected to stay largely stable with a positive bias, particularly for mid- to high-GAR grades.

Leave a Reply