- Firm import parity supporting domestic coke prices

- Cautious downstream demand capping further upside

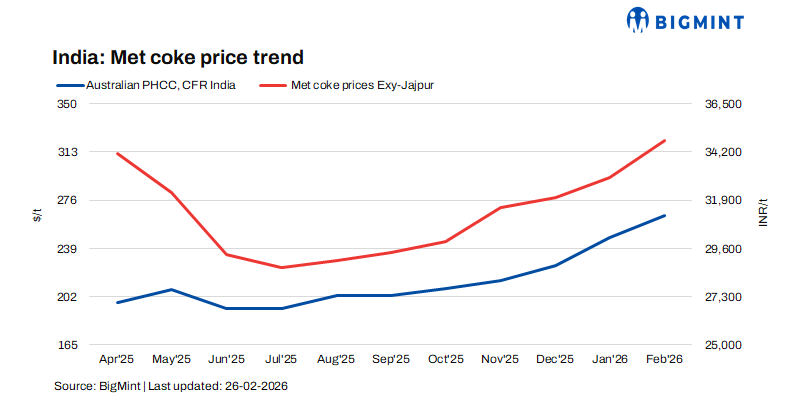

Indian blast furnace (BF)-grade metallurgical coke prices recorded a marginal week-on-week increase on 26 February 2026, supported by balanced domestic demand-supply fundamentals and firm import parity levels, despite a mild correction in upstream raw material costs.

Domestic market trends

In eastern India, BF-grade coke (25-90 mm) prices increased by INR 200/t week-on-week to INR 35,000/t ex-Jajpur, while in western India, prices rose by INR 100/t to INR 30,500/t ex-Gandhidham. The uptick reflects stable procurement by integrated steel producers and limited immediate supply pressure.

Foundry-grade metallurgical coke (+90 mm) prices remained unchanged at INR 36,100/t ex-Rajkot, indicating steady demand from the casting and foundry segment. The absence of price movement suggests a balanced market, with neither aggressive restocking nor oversupply conditions influencing trade flows.

Import parity and global influences

Firm import price indications continued to lend support to domestic pricing. Indonesian-origin BF coke (65/63) price indications were at $270-275/t CFR India, translating to a landed cost of approximately INR 34,000-34,500/t. These levels provided a pricing floor for domestic suppliers, allowing them to sustain elevated offers despite softer coking coal costs. However, bids were heard lower by $10.

Upstream, Australian premium hard coking coal prices declined marginally by $2/t week-on-week to $241/t FOB, amid subdued buying interest and cautious procurement from key importing markets. However, the limited correction was insufficient to materially alter domestic coke cost structures.

In China, the coking coal and coke markets remained stable but weak in tone as of 25 February. While post-holiday coal output continued to recover, downstream steel demand lagged. Coking plants maintained need-based procurement, and selective price cuts by some mines reflected efforts to stimulate sales. Weak steel margins, emission control measures, and subdued construction activity continued to weigh on consumption, indicating downside risks for coking coal prices in the near term.

Downstream Indicators and demand signals

Downstream sentiment remained cautious but stable. NMDC Limited’s Nagarnar Steel Plant auctioned 12,000 t of steel-grade pig iron on 20 February 2026, of which 4,600 t were booked at a base price of INR 36,500/t ex-works, while 7,400 t remained unsold. Notably, bids were unchanged from the 13 February auction, where the full quantity was cleared at the same price, indicating selective yet price-sensitive buying.

According to BigMint’s assessment, steel-grade pig iron prices in Durgapur declined by INR 650/t week-on-week to INR 37,650/t ex-works. Although this reflects cautious sentiment across the steel value chain, the correction has not yet translated into immediate pressure on metallurgical coke demand.

Market Outlook

In the near term, domestic BF-grade coke prices are expected to remain broadly stable with a mild firm bias, supported by import parity and steady integrated steel production levels. However, potential downside risks persist from softer global coking coal prices, weak Chinese steel fundamentals, and subdued pig iron demand domestically.

Should upstream coal prices correct further or steel margins compress meaningfully, coke prices may face gradual pressure. Conversely, sustained import firmness and stable blast furnace utilisation rates could limit sharp downside movement, keeping the domestic market range-bound in the short term.

Leave a Reply