- Australian, Brazilian shipments surge on Chinese restocking demand

- Freight sentiment mixed; Pacific rates uneven, Atlantic remains firm

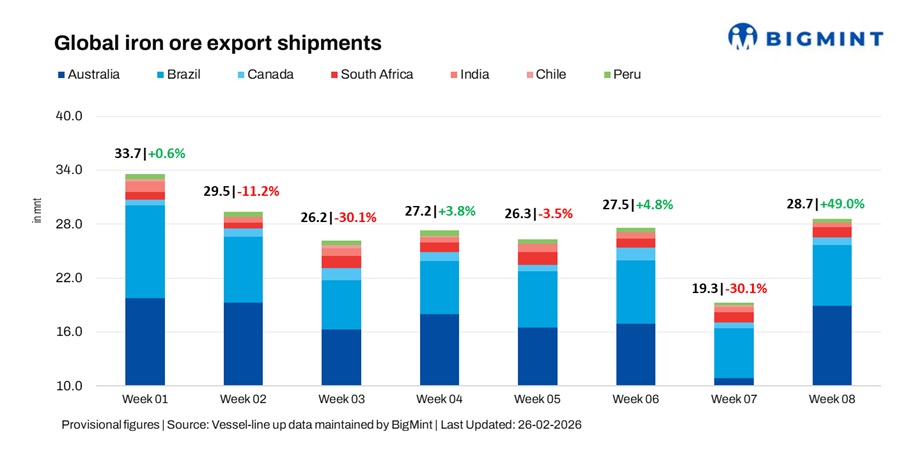

Country-wise trends

Port & shipper-wise trends

- Australia: Easing cyclone-led disruptions and active Chinese restocking contributed to the sharp w-o-w uptick. Port Hedland handled 11.8 mnt, while Rio Tinto (6.8 mnt), BHP (6 mnt) and FMG (4.3 mnt) led shipments. China absorbed 15.8 mnt of volumes.

- Brazil: The increase in shipments was supported by steady export programmes and sustained Asian demand. Ponta Da Madeira shipped 3.2 mnt, Tubarao 1.2 mnt, with Vale exporting 3.6 mnt during the week.

- Canada: The increase in exports reflected improved cargo flow from eastern terminals. Sept-Iles handled 0.5 mnt, while Port Cartier shipped 0.3 mnt.

- South Africa: Shipments increased moderately, underpinned by stable rail-to-port logistics. Saldanha accounted for 1.1 mnt, while Richards Bay handled 0.1 mnt.

- India: Exports declined, as subdued Chinese spot enquiries and ample port inventories weighed on bookings. Paradip shipped 0.3 mnt during the week.

- Peru: Shipments recovered, reflecting scheduled cargo clearances. Shougang Hierro exported 0.4 mnt, with China remaining the key destination.

- Chile: No iron ore shipments were recorded during the week.

Dry bulk iron 0re freight market sentiment

Pacific iron ore freights exhibited mixed trends w-o-w, as post-holiday demand normalisation supported select routes while uneven cargo flows capped broader gains. In contrast, Atlantic rates remained relatively supported, underpinned by steady Brazilian and South African export programmes and tighter regional tonnage supply.

Outlook

With Chinese procurement activity normalising and Australian export programmes stabilising, shipments may remain supported in the near term. However, the trajectory will hinge on steel demand recovery in China and evolving freight market dynamics.

Leave a Reply