- G4 dominates 12 Feb auction allocations

- G4 grade prices spike to INR 7,326/t on limited volumes

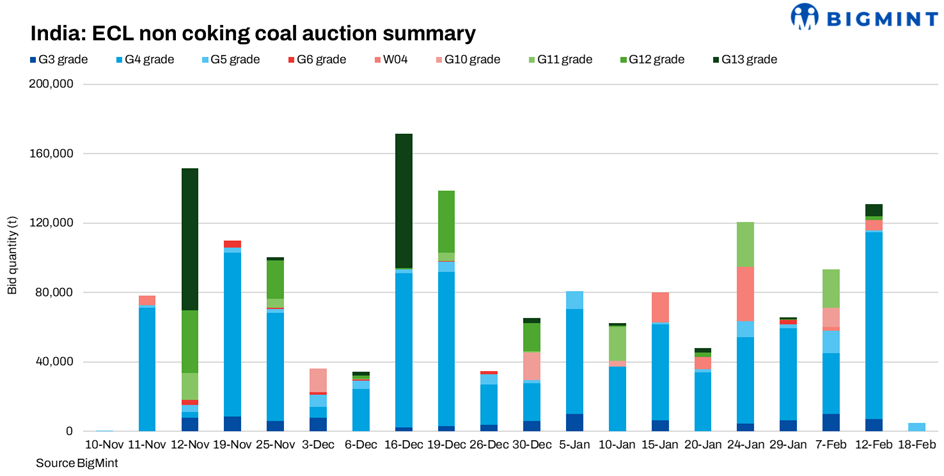

Eastern Coalfields Limited (ECL) conducted auctions on 12 February and 18 February 2026. Against a notified quantity of 1,149,650 t on 12 February, total allocated volume stood at 131,050 t, reflecting selective buyer participation. The 18 February event was significantly smaller, with 5,000 t offered and fully allocated, but at sharply higher prices.

Volume and grade trend

On 12 February, G4 grade coal dominated allocations at 107,900 t with an average bid of INR 5,381/t, accounting for the bulk of cleared volumes. Major contributions came from Sonepur Bazari at 30,000 t at INR 5,161/t and Chitra at 20,000 t at INR 4,963/t. Nakrakonda and Jhanjra also recorded sizeable clearances within the INR 4,400-4,800/t band.

Premium pricing was visible in select parcels. Parbelia cleared 2,000 t at INR 7,776/t, while Bansra and Porascole saw bids above INR 6,700/t. G3 totalled 7,000 t at an average INR 6,576/t. Lower grades such as G12 and G13 cleared at INR 1,798/t and INR 1,713/t respectively, indicating stable utility-linked demand. The overall average price for 12 February stood at INR 5,012/t.

On 18 February, the entire 5,000 t of G4 from Chinakuri Mine cleared at a significantly higher average price of INR 7,326/t. This marked a strong premium over the 12 February G4 average, indicating tight availability or stronger competitive bidding for specific mine-linked material.

Buyer participation

On 12 February, Shakambhari Ispat & Power emerged as the largest buyer with 20,050 t at INR 5,107/t. Neelkanth Sales secured 6,400 t at INR 5,140/t. Mark Trading Company and Iconic Coal Company were active in both G3 and G4 segments, with G3 bids ranging between INR 6,678-6,818/t. Shree Enterprises and Khemka Minerals lifted material above INR 6,000/t in premium parcels.

Lower-grade coal buying remained steady, with Apollo Energies and Jaiswal Brothers securing G12 and G13 material at INR 1,713-1,798/t.

On 18 February, participation was concentrated among multiple smaller buyers. Vinayak Support Services led with 3,400 t at INR 7,247/t, followed by Shree Enterprises, Mahalaxmi Traders and Krishna Enterprise, all bidding within the INR 7,250-7,450/t range. The tighter buyer pool and higher clearing price suggest focused competition for limited premium material.

Comparison and market implication

Compared to early February auctions, the 12 February event reflected broad but disciplined participation, with allocations significantly below offered volumes. G4 remained the anchor grade, while high-CV parcels attracted premium bids. The weighted average price of INR 5,012/t indicates balanced procurement across grades.

In contrast, the 18 February auction reflected strong price discovery in a constrained volume setting, with G4 clearing at INR 7,326/t nearly INR 1,900/t higher than the 12 February G4 average. This divergence highlights grade- and mine-specific demand rather than broad market escalation.

Market outlook

The latest auctions indicate stable demand for mid-CV grades. While overall allocation ratios remain controlled, higher bids in limited-volume auctions suggest tightening sentiment in specific segments.

Future price direction will depend on grade availability, downstream industrial demand, and auction frequency. If limited high-CV parcels continue to emerge, premium pricing may persist despite overall disciplined procurement behaviour.

Leave a Reply