- RKAB delays are restricting Indonesian coal exports

- Tight supply is pushing up prices of mid- and high-CV grades

Policy uncertainty tightens export supply

The Indonesian coal market has become the main driver of price movements across Asia in recent weeks. The biggest reason is uncertainty around the approval of annual mining plans, known as RKAB.

Because producers are still waiting for clarity on these approvals, many miners are cautious about committing to production and exports. Some are holding back cargoes, while others are offering coal only at higher prices. This has reduced the number of prompt cargoes available in the market and tightened supply for buyers across Asia.

Traders report that offers for Indonesian coal, especially mid- and high-calorific material, have become limited. In some cases, sellers are not quoting at all until they have better visibility on production approvals. This lack of clarity has slowed trade flows and reduced spot market liquidity.

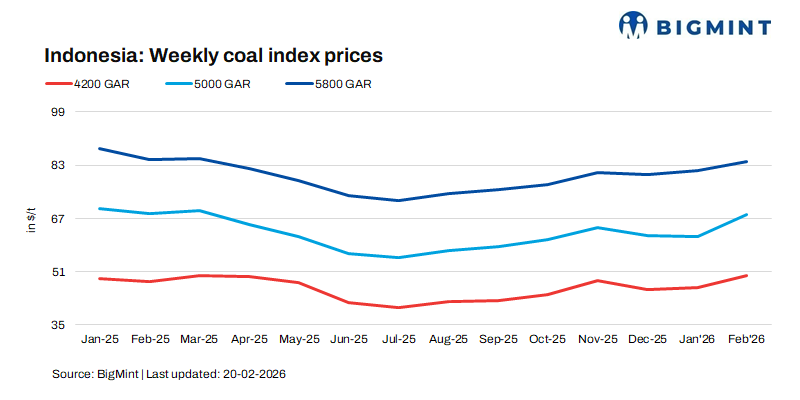

Prices rising across calorific segments

As supply has tightened, prices for Indonesian coal have moved higher across most grades.

Low-rank coal of around 3,400 kcal/kg GAR is now at $33/t FOB, while 3,800 kcal/kg GAR coal is around $41/t FOB. Mid-range coal at 4,200 kcal/kg GAR has moved toward $50-51/t FOB, reflecting stronger demand from price-sensitive markets.

Higher-calorific Indonesian coal of around 5,000 kcal/kg GAR is trading near $67/t FOB, while premium material close to 5,800 kcal/kg GAR has risen to around $84/t FOB.

These price increases are also visible in importing markets. At Indian ports, Indonesian coal prices have risen sharply w-o-w. According to BigMint’s latest assessment, 5,000 GAR coal prices advanced by INR 600/t w-o-w to INR 8,300/t at Kandla and INR 8,200/t at Vizag.

Similarly, 4,200 GAR coal prices recorded a firm increase of INR 450/t w-o-w, reaching INR 6,450/t at Kandla and INR 6,350/t at Vizag. Lower-grade 3,400 GAR coal also witnessed a notable uptick, rising by INR 250/t w-o-w to INR 4,850/t at Navlakhi.

The strongest price increases have been seen in mid- and high-calorific coal, where stock levels are lowest and demand is strongest.

Impact on regional trade and buyer behaviour

The tightening of Indonesian supply has forced buyers across Asia to adjust their sourcing strategies.

Indian consumers, in particular, are facing reduced availability of Indonesian coal at ports. Traders report limited fresh arrivals and low stocks of better-quality coal used for blending. This has encouraged some buyers to look at alternative origins such as South Africa or domestic coal.

However, Indonesian coal remains the cheapest and most flexible fuel option for many industries. As a result, buyers continue to purchase even at higher prices, especially when they need specific calorific values for blending or operational needs.

Freight costs have also played a role. Stronger Panamax shipping rates have increased delivered coal costs, reinforcing the upward trend in import prices.

Outlook

The near-term outlook for Indonesian coal depends largely on government decisions.

If mining plans are approved soon and producers increase exports, supply could improve quickly and prices may stabilise. However, if uncertainty continues, exporters are likely to remain cautious, keeping availability tight and prices supported.

For now, Indonesian coal is setting the tone for the regional market. Limited export visibility, cautious seller behaviour, and steady Asian demand mean that prices are likely to remain firm in the short term.

In simple terms, the Indonesian coal market is not facing a shortage of reserves, but a shortage of certainty. Until policy clarity improves, supply will stay tight, trade will remain selective, and prices across Asia will continue to take direction from Indonesia.

Leave a Reply