- Cautious steel demand, especially in China, limiting price upside

- Controlled but adequate supply keeping prices rangebound

The global market for steelmaking raw materials – metallurgical coal, PCI and metallurgical coke – is currently stable on the surface but divided underneath. Prices are holding in most regions, yet buying interest remains cautious, and several structural factors will determine how the market may move next.

Where prices stand

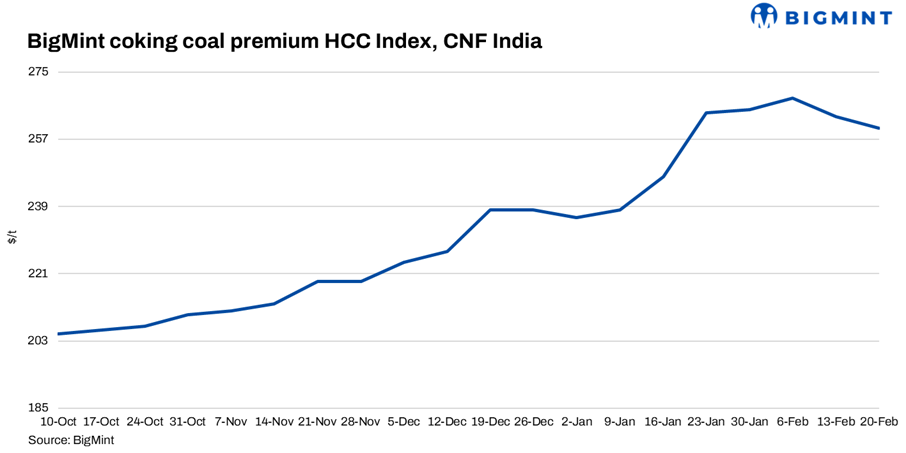

Premium Australian hard coking coal remains the strongest segment of the market. Top-tier low-vol and mid-vol coals are trading broadly in the low-to-mid $240s/t FOB Australia, while delivered prices into India are closer to the high-$240s to low-$250s range. Delivered China prices remain lower, around the low-$220s, reflecting weaker Chinese buying.

Lower-tier hard coking coal sits well below premium grades, mostly in the low-to-mid $190s/t FOB Australia, with delivered values into India and China near $195-200/t.

PCI coal is significantly cheaper. Australian low-vol PCI sits near the low-$150s FOB Australia, but delivered Asia prices are anchored lower by Russian material, with deals into China near the low-$120s and into India around the mid-$130s.

Metallurgical coke prices are stable rather than rising. Indonesian coke exports are broadly around $255/t FOB, with cargoes delivered into India near $280/t. Domestic Indian coke remains elevated, especially in eastern regions, where ex-stock prices are roughly INR 34,000-35,000/t, while western India trades lower.

Why the market looks this way

The biggest factor shaping the market right now is cautious steel demand rather than supply shortages.

China’s buying activity has been muted following the holiday period, reducing spot liquidity. When China steps back, the seaborne market tends to drift rather than move sharply. India has become the marginal buyer, but Indian mills are purchasing selectively and only covering immediate needs.

At the same time, supply signals are mixed. Some Atlantic producers have cut output due to weak margins, which has prevented prices from falling sharply. But those cuts have not translated into a rally because buyers are not chasing cargoes.

Freight economics also matter. Australian coal remains structurally competitive into Asia, while US cargoes face higher shipping costs into India, limiting their ability to displace Australian supply even when FOB prices are lower.

In PCI, Russian exports continue to act as the price anchor. As long as low-priced Russian PCI flows into Asia, it caps how high Australian PCI can rise.

For coke, the story is simple: availability exists and buyers are not rushing. This balance keeps prices stable rather than directional.

What happens next

The short-term outlook is sideways rather than bullish.

Premium metallurgical coal is likely to remain supported because steel mills still need high-quality coal and sellers are not under distress. However, any sustained price increase would require stronger buying from China or a clear rise in Indian steel output.

PCI is likely to remain capped by Russian supply, keeping delivered Asia prices competitive.

Met coke will probably stay rangebound unless blast furnace utilisation rises sharply or export supply tightens unexpectedly.

In short, the steel raw materials market is not weak – but it is cautious. Prices are stable because supply is controlled, yet demand is not strong enough to push the market decisively higher.

Leave a Reply