- Global refined copper output to rise only 0.9% in 2026 against 3% in 2025

- Supply shortfall pushes major producers to lift 2026 production guidance

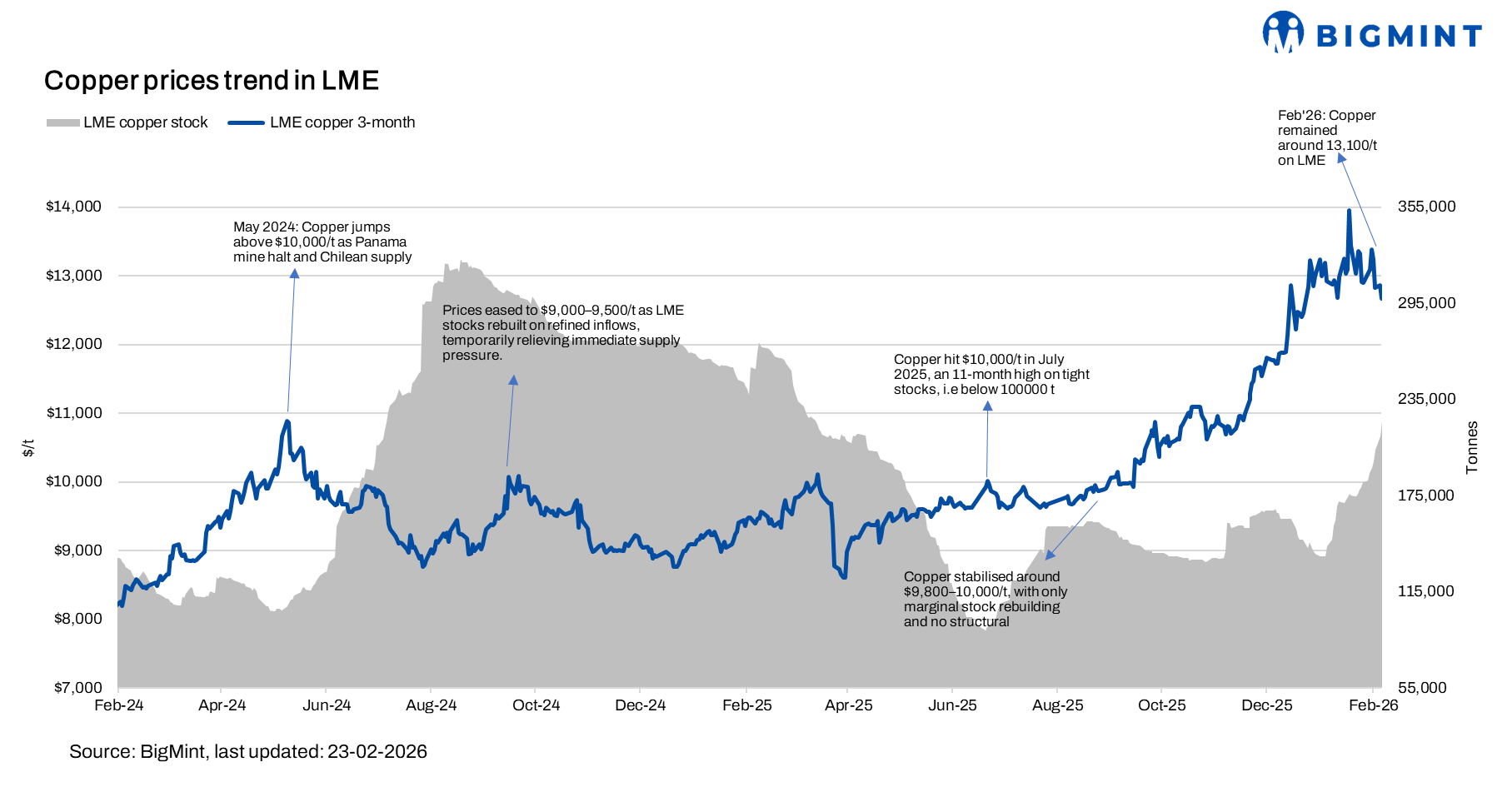

Copper futures on the London Metal Exchange (LME) climbed up to $13,000/tonne (t) on 20 February from $12,800/t on 13 February, marking an increase of roughly $200/t.

On the supply side, global refined copper output growth has moderated. Industry forecasts show world refined copper production is set to rise by a modest 0.9% in 2026, compared with 3% growth in 2025, while consumption continues to expand — particularly in China, which accounts for over half of global usage.

This supply crunch has also prompted major producers to raise their output: Teck Resources reported a nearly 10% increase in copper output to 134,000 t in Q4 and has maintained a 2026 production outlook of 455,000-530,000 t — a meaningful chunk of global mine supply. Meanwhile, Codelco expects to lift output to 1.344 million tonnes (mnt) in 2026, a slight increase from 1.33 mnt in 2025.

In concentrated markets, processing charges remain under pressure. Long-term TC/RC benchmarks for Chinese smelters have moved toward a record-low $0/t, reflecting tight concentrate availability and uneAven regional pricing structures.

Indian market sources noted that exporters lifted import scrap offers in line with LME gains, though Indian buyers are selectively procuring amid currency volatility and existing inventory cover.

BHP outlines copper production expansion plans

BHP has outlined a global copper project pipeline that could lift its production capacity by 1.8-2 mnt over the next decade, with final investment decisions planned between 2026 and 2032 and start-ups from 2028 onward. Its major Copper South Australia Phase 1 and 2 projects are expected to add 790,000-910,000 t between 2029 and 2038. The company maintained FY’26 copper production guidance at 1.9-2 mnt and recently invested $555 million to expand South Australian operations. BHP estimates that an additional 10 mnt/yr of new capacity will be required globally by 2035 to address supply gaps, projecting demand growth from 34 mnt in 2026 to over 50 mnt by 2050. Similar deficit concerns have been flagged by South32, Cochilco, and Nornickel.

Outlook

Copper is likely to stay largely stable to mildly firm near current levels. A post-holiday pickup in Chinese physical demand and clearer TC/RC contract settlements could reinforce the rally, while profit taking and subdued spot activity may temper sharp upward extensions in the near term.

Leave a Reply