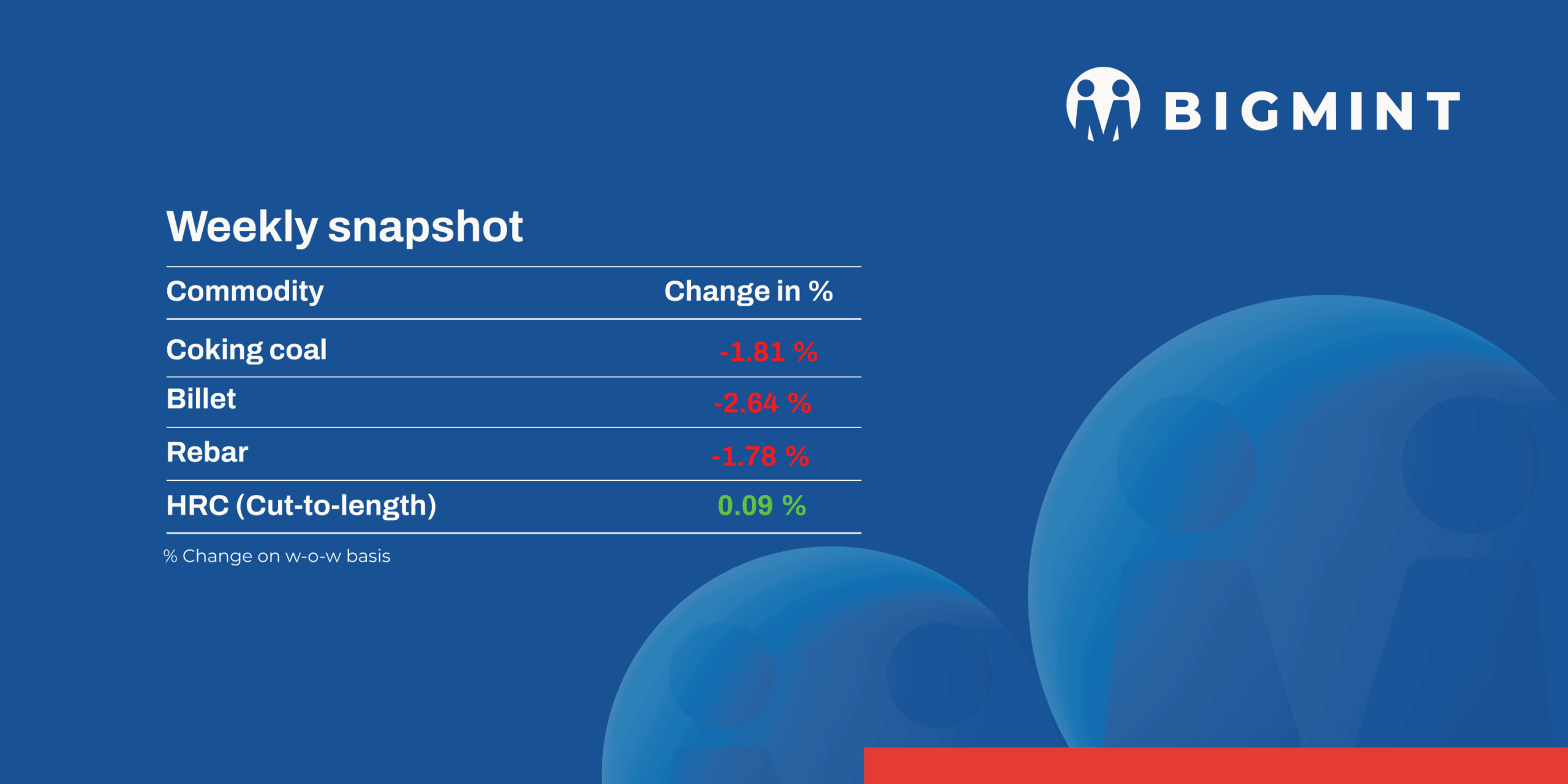

- Semi-finished and long steel prices fell sharply as weak demand persisted across domestic markets

- Raw material prices stayed mixed, while cautious buying and low liquidity limited overall market recovery

Indian steel market weakens as semi-finished and long steel prices fall amid sluggish demand

Iron ore and pellet

- In OMC’s 19 Feb’26 auction, 99% of 1.58 mnt iron ore lumps were booked at INR 5,850–7,350/t with premiums of INR 150–900/t, though weighted bids fell INR 150/t m-o-m despite a base price hike. Strong demand was driven by likely supply tightening in March. For fines, 88% of 2.25 mnt were booked at INR 4,450–6,300/t with average premiums of INR 350/t. Weighted bids declined INR 100/t m-o-m even as base prices increased, keeping overall sentiment rangebound.

- BigMint’s bi-weekly assessment indicates that iron ore concentrate (Fe 62%) prices in Jabalpur held steady at INR 5,300/t ($58/t) ex-works on 18 February, remained steady w-o-w also. The firmness is supported by stability in pellet and iron ore rates in Odisha, while most producers remain booked for the next month with ongoing dispatches against prior orders.

- In SAIL’s auction from Odisha, 12,000 t of fresh fines (Fe 64%) from Bolani were booked at INR 6,400/t on 13 Feb, followed by 20,000 t of dump fines (Fe 60.77%) at a base price of INR 4,950/t on 14 Feb, and another 12,000 t of dump fines (Fe 61.74%) at INR 5,700/t against a base price of INR 5,150/t on 17 Feb. From Barsua, 19,950 t of iron ore tailings (Fe 59.02%) were booked at INR 5,100/t on 13 Feb.

Coal

-

South African thermal coal prices at Indian ports moved higher w-o-w on firm RBCT export offers and tight coal availability due to mine maintenance and operational disruptions in South Africa. As per BigMint’s assessment, exw-Paradip 5,500 NAR rose INR 350/t to INR 10,350/t and 4,800 NAR increased INR 400/t to INR 9,000/t. At Vizag, 5,500 NAR gained INR 200/t to INR 10,100/t while 4,800 NAR rose INR 350/t to INR 8,850/t. Export offers climbed $4–6 to around $91/t FOB RBCT. No South African stock was available at Haldia.

-

Domestic non-coking coal prices strengthened w-o-w, supported by firmer imported coal trends and stronger SECL auction participation. As per BigMint’s assessment, 4,500 GCV increased to INR 4,900/t and 5,000 GCV to INR 5,950/t exw Bilaspur. At the 19 Feb’26 SECL auction, high-grade bids rose INR 150–200/t compared with the previous event. SECL also announced sale of 1,768,000 t on 26 Feb’26, indicating steady domestic supply despite improving demand sentiment.

-

BigMint’s PHCC index was assessed at $260/t CNF Paradip on 21 Feb’26, down $3/t w-o-w amid subdued activity during Chinese Lunar holidays. Limited fresh deals were reported as buyers awaited clearer price direction, with FOB expectations from large Indian mills below $220/t. Australian PHCC declined $6/t to $243/t FOB, reflecting muted global participation.

-

Indian BF-grade metallurgical coke prices remained stable w-o-w despite softer coking coal costs, as firm import parity provided support. BF coke stood at INR 34,800/t ex-Jajpur in the east and INR 30,400/t ex-Gandhidham in the west. Foundry-grade coke was unchanged at INR 36,100/t ex-Rajkot. Indonesian BF coke offers were heard at $270–275/t CFR India, translating to INR 34,000–34,500/t landed, helping domestic producers maintain price stability.

Ferrous scrap

- Imported scrap prices into India remained largely steady w-o-w, with some variation by origin and port. HMS 80:20 was indicated at $350–355/t CFR at Chennai, Mundra, and Nhava Sheva, while shredded was heard at $368–375/t. UK and European-origin offers dominated the market, with selective quotations from the US, Australia, Brazil, West Africa, and Latin America. Buyer bids were typically $5–10/t below offers, reflecting cautious sentiment.

- Trading was limited, with a few deals concluded for HMS, bundles, and turning borings. Chennai saw relatively better demand than the west coast, though mills largely continued hand-to-mouth buying.

- Around 5,000-6,000 t was booked during the week, including nearly 1,500-2,000 t of HMS at $330–355/t, along with turning borings, HMS bundles, and HMS 60:40.

- Ferro Alloys

Silico Manganese:Indian silico manganese (60-14) prices went down slightly INR 525/t ($6/t) w-o-w to INR 73,000 -73,700/t ($805-812/t ) across Durgapur, Raipur, Vizag, and Raigarh. Steel mills continued need-based procurement, maintaining cautious buying. Improved supplies, limited liquidity in the market pressured some sellers to reduce offers, contributing to the overall price softening. - Ferro Manganese:Indian ferro manganese (70%) prices inched down by INR 800/t ($9/t) w-o-w to INR 73,700/t ($812/t) in Raipur and INR 300/t ($3/t) to INR 73,500/t ($810/t) in Durgapur. Weak acceptance of higher quotes and cautious buying limited transactions, exerting mild downward pressure on market sentiment.

- Ferro Silicon:Indian ferro silicon (Si 70%) prices increased by INR 2,500/t ($28/t) w-o-w to INR 98,300/t ($1,083/t) exw Guwahati. Prices in Bhutan also rose by INR 3,300/t ($37/t) to the same level. Prices strengthened due to tight supply, as major sellers were largely sold out, pushing offers higher while sustained buying supported the market

- Ferro Chrome:Indian high carbon ferro chrome (HC 60%, Si 4%) prices declined by INR 800/t ($8t) to INR 123,000/t ($1,356/t) exw- Jajpur, as cautious end-user buying reduced support for higher offers. Bid-offer gaps emerged, limiting trade.

- Additionally, at the 19 Feb’26 auction by Odisha Mining Corporation (OMC), 59,400 t of chrome ore were sold out of 114,600 t offered. Bids for grades above 40% increased 13-17%(INR 2,498 – 3,545/t) m-o-m, while bids for grades below 40% rose by about 10% (INR 997/t).

Semi Finished

- India’s semi-finished steel market witnessed a sharp correction this week, as continuous weakness in finished steel demand weighed on sentiment across the country. As per BigMint’s assessment, domestic billet prices across key regions declined by INR 400-1,500/t ($4-16/t) w-o-w, amid subdued buying interest and thin trade volumes. Major producing hubs including Mandi Gobindgarh, Raipur, Chennai, and Hyderabad recorded sharp declines of INR 1,000-1,500/t ($11-16/t) w-o-w, amid continued pressure from weak downstream offtake. Market participants indicated that despite aggressive price corrections, demand revival remains absent in both semi-finished and finished steel segments.

- Sponge iron (DRI) segment also tracked the downward trend. Prices across key producing regions declined by INR 250-800/t ($2-8/t) w-o-w, pressured by weak offtake and competitive offers from neighbouring markets. Limited bookings and cautious buying behaviour further dampened sentiment. Falling realisations in billet, coupled with narrowing conversion spreads, intensified margin pressure for induction furnace mills. Producers remained reluctant to build raw material inventory amid uncertain finished steel demand and volatile pricing conditions.

- SAIL-BSP conducted an auction for 1,950 t of steel-grade pig iron on 19 Feb’26, with the entire volume booked at an average price of INR 37,400/t ex-works. Prices remained stable compared to the 9 Feb’26 auction, where 2,990 t were fully sold at INR 37,400/t, following an INR 550/t increase in the preceding auction.

- NMDC’s Nagarnar Steel Plant auctioned 12,000 t of steel-grade pig iron on 20 Feb’26, with 4,600 t booked at a base price of INR 36,500/t exw. The remaining 7,400 t were left unsold. Bid levels were unchanged from the 13 Feb’26 auction, when the entire 12,000 t were sold at the same price, indicating steady but selective buying interest.

- India’s DRI export market remained under pressure this week, tracking the persistent downtrend in the domestic market. Offers to Nepal declined by $5/t to $335/t CPT Raxaul, while offers to Bangladesh eased by $1/t to $344/t CPT Benapole with limited deals reported.

Finished Long Steel

- IF-rebar: India’s Induction Furnace (IF) route rebar prices witnessed a downward trend on a week-on-week basis. Buying activity remained limited and largely need-based, as market participants continued to adopt a cautious, wait-and-watch approach. Fresh order bookings were subdued, prompting manufacturers to either reduce their offers or extend higher trade discounts depending on their previous booking positions. Mill inventories are currently estimated above 10 days which was earlier maintained around 8-10 across the regions. Given the prevailing market conditions, prices are expected to remain range-bound in the near term.

- On a weekly basis, rebar prices declined by INR 400–1,200/t across regions, with Mandi witnessing the sharpest fall of INR 1,200/t, as per BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebars (10–25 mm), manufactured through the IF route, were assessed at INR 44,000–44,400/t ex-works Raipur and INR 48,200–49,200/t ex-works Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 45,600-46,200/t exw-Raipur.

- Trade reference prices of wire rod stood at INR 44,000-44,500/t ex-Raipur.

BF-rebar-Indian primary steelmakers increased rebar prices by up to INR 1,000/tonne (t) ($11/t) this week, sources informed BigMint. Post-revision, list prices stood at INR 58,500-59,500/t ($643-654/t) on landed basis. - Trade-level BF-rebar prices (distributor to dealer) rose by INR 400/t ($4/t) w-o-w to INR 59,000/t ($648/t) exy-Mumbai, as per BigMints assessment on 20 February 2026. Market participants noted that buyers were reluctant to place fresh orders at elevated price levels following the recent sharp price increase, leading to cautious procurement behaviour during the week.

- In the projects segment, prices hovered at around INR 59,000-60,000/t ($648-659/t) FOR basis. Demand from the projects segment remained steady with dispatches of previously booked orders.

Flat Steel

- The trade-level prices of hot-rolled coils (HRC) in India held steady in most regions during the week ending 17 February with HRC prices assessed in the range of INR 52,000-55,100/t ($573-608/t) and cold-rolled coil (CRC) prices assessed at INR 56,500-62,000/t ($623-683/t).

- Demand in the South remains steady, with consumption maintaining normal levels across key sectors. Market sentiment in the North has weakened over the past week. There was initially strong anticipation of a mid-month price hike from the mills, but since this has not occurred, confidence has declined. The Western market is currently fairly balanced, though trading activity has slowed in recent days. Market feedback suggests that mills are working to maintain pricing discipline despite lower trading volumes.

- India’s bulk imports of HRCs touched 149,529 t as of 13 February, based on vessel line-up data. Around 2,55,163 t of additional cargoes are expected by mid-March.

- India’s bulk exports of HRCs touched 31,250 t as of 13 February. Around 1,08,500 t of additional cargoes are in transit.

- BigMint’s Indian HRC (S275) export index for the European Union (EU) dropped by $5/t w-o-w to around $570/t FOB main port from $575/t in the previous week. Moreover, Indian HRC (SAE 1006) export index for the Middle East and South East Asia declined by $5/t w-o-w to $485/t FOB main port compared with $490/t a week earlier following a recently concluded deal.

Leave a Reply