- Mid-week firmness fades amid stock overhang

- MCX prices range-bound; open interest increases

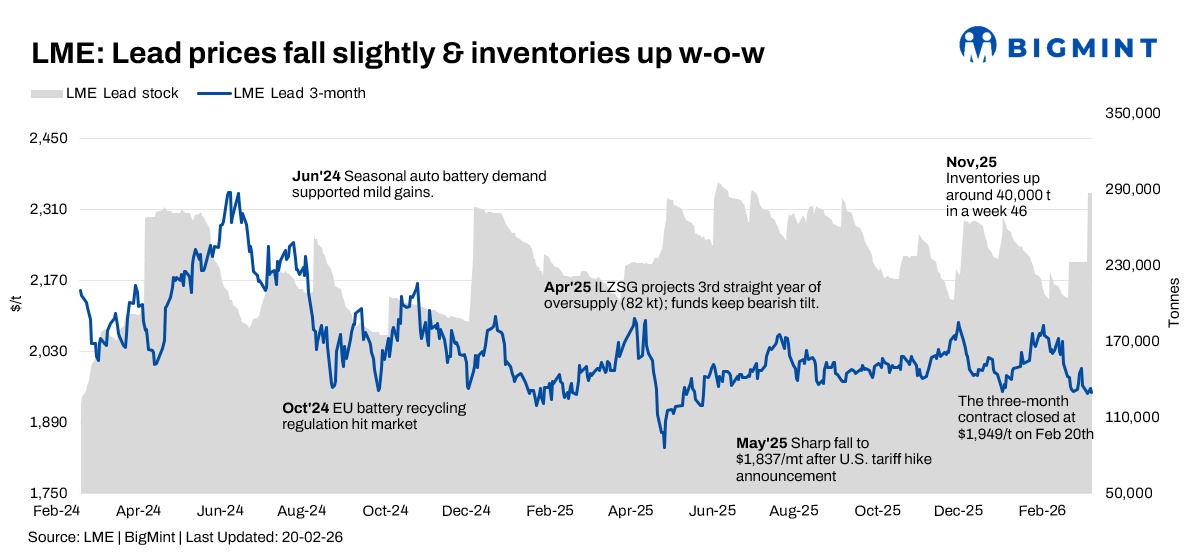

Lead prices on the London Metal Exchange (LME) traded in a narrow band in the week ended 20 February, as early stability gave way to consolidation amid a sharp rise in exchange inventories. While prices attempted to stabilise above the $1,900/t mark, a sizeable stock build mid-week weighed on sentiment and limited upside follow-through.

Price trends

LME cash lead opened at $1,903/t on 16 February and briefly climbed to a weekly high of $1,909/t on 19 February before easing to close at $1,902/t on 20 February, marginally lower w-o-w.

The three-month contract followed a similar pattern, rising to a weekly high of $1,957/t on 19 February before settling at $1,949/t on 20 February, broadly steady compared with the start of the week.

The contract once again failed to sustain momentum toward the psychologically significant $2,000/t resistance level. The price action reflects a market lacking strong directional conviction, with rallies attracting selling interest near the upper band of the recent range.

Inventory analysis

LME lead stocks surged sharply to 287,125 t on 17 February from 232,650 t at the start of the week, marking a significant 54,475 t increase. Inventories remained unchanged at this elevated level through 20 February.

The sharp inflow contrasts with the previous week’s stability and signals renewed availability of metal into exchange warehouses. While prices did not react aggressively lower, the sizeable stock build reinforces the presence of comfortable visible supply and may cap near-term rallies.

If further inflows materialise, bearish pressure could intensify. Conversely, the market may stabilise if stocks plateau at current levels without additional builds.

SHFE lead trends

Price publication for China’s domestic lead market remained suspended from 16-24 February due to Lunar New Year holidays, limiting fresh directional cues from the Shanghai market.

The absence of Chinese trading activity likely contributed to the subdued global volatility, as arbitrage flows and cross-exchange momentum were temporarily muted.

MCX price movements

On the MCX, the March 2026 lead contract traded within a narrow INR 188,000-190,250/t range during the week.

Prices closed at INR 188,750/t on 20 February, marginally lower compared with INR 188,900/t on 16 February. Open interest rose from 268 lots to 319 lots over the same period, indicating selective fresh positioning despite muted price action.

Volumes remained modest, reflecting cautious domestic participation amid range-bound global cues and limited immediate triggers from China.

Outlook

Lead is likely to trade within the $1,880-1,970/t range in the near term. The sharp increase in LME inventories introduces a bearish overhang, though the absence of continued daily inflows suggests the market may stabilise.

The resumption of Chinese trading post-holiday will be a key catalyst for directional clarity. Until then, price action may remain range-bound, with cross-metal sentiment and macro cues guiding short-term moves.

Leave a Reply