- Rangebound trade ahead of Lunar New Year holidays

- Indian scrap prices correct after record-high rally

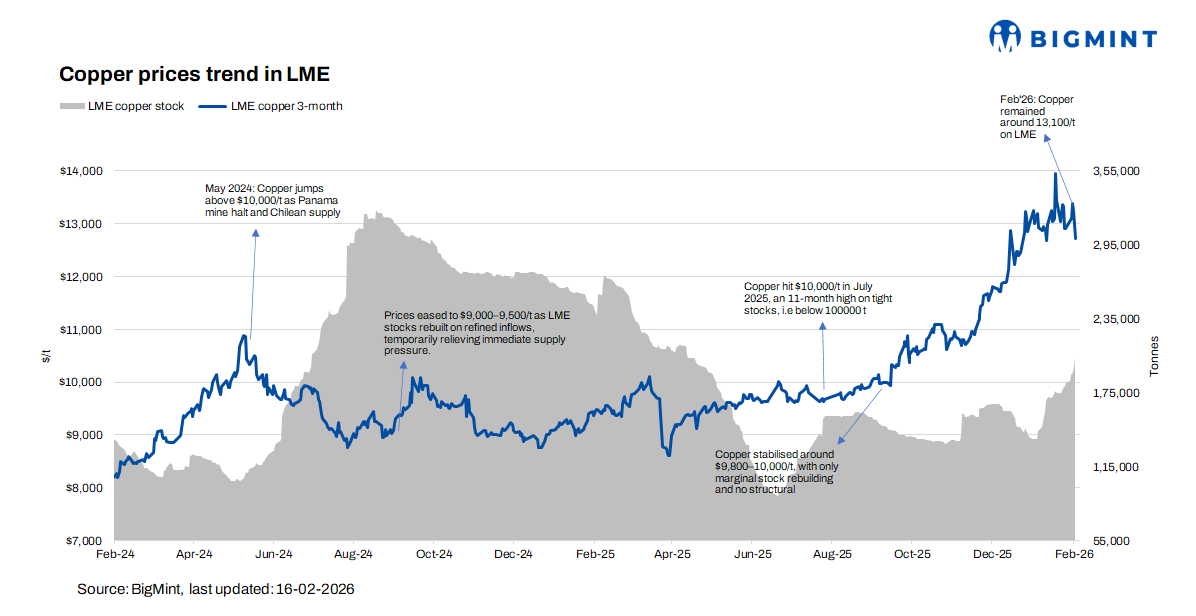

LME copper prices declined 1.1% w-o-w in the week ended 13 February 2026, as mild profit booking and a cautious tone ahead of China’s Lunar New Year capped upside momentum. After touching record highs in the previous sessions, the red metal traded largely rangebound, with selling pressure emerging at higher levels and limiting fresh gains.

Pricing, currency and supply dynamics

The weekly correction was partly influenced by a relatively firm US dollar, which made copper more expensive for non-dollar buyers and curbed fresh speculative inflows. Market participants indicated that funds trimmed long positions after recent price stability, adding short-term downside pressure.

On the supply side, there were no major disruptions reported from key mining regions in Latin America. Concentrate flows remained stable and treatment charge expectations were largely unchanged, signalling comfortable raw material availability. In the absence of supply shocks, the market lacked fresh bullish triggers to sustain the earlier rally.

Indian market updates

In India, domestic copper scrap prices corrected following the sharp LME-led rally seen earlier this month. Ample physical availability eased supply-side tightness, resulting in Armature scrap trading around INR 1,140,000/t ex-Punjab and INR 1,145,000/t ex-Delhi, down from INR 1,200,000/t levels earlier.

The imported scrap market, however, remained firm w-o-w, with overseas suppliers maintaining offer levels despite softer domestic spot trades. For Indian buyers, the modest LME correction may offer limited cost relief for scrap and semi-finished imports, unless the downtrend extends further.

Outlook

The recent dip appears to be a healthy consolidation phase after steep gains. Post-holiday restocking demand from China, movements in LME warehouse stocks, US dollar trends, and shifts in the forward curve will remain key indicators for near-term direction. Prices are likely to stay rangebound with a slight downside bias unless fresh supply disruptions or stronger physical demand re-emerge.

Leave a Reply