- Indonesian policy uncertainty is restricting exports and supporting prices

- Global Indonesian benchmarks extend gains weekly

Indian portside prices of Indonesian-origin thermal coal increased on a week-on-week (w-o-w) basis during the week ended 13 February 2026, driven primarily by supply-side constraints linked to regulatory uncertainty in Indonesia and steady domestic demand in India.

Price movement at Indian ports

Portside prices across major Indian ports registered an upward trend. BigMint’s assessment, 5,000 GAR coal prices increased by INR 450/t w-o-w to INR 7,700/t at Kandla and INR 7,600/t at Vizag. Similarly, 4,200 GAR coal prices rose by INR 400/t to INR 6,000/t at Kandla and INR 5,900/t at Vizag. Meanwhile, 3,400 GAR coal prices edged up by INR 100/t to INR 4,600/t at Navlakhi.

The relatively sharper increase in higher grades reflects tighter availability in the mid- to high-calorific value segments, whereas lower-grade material witnessed comparatively moderate gains due to adequate port inventories.

Supply-side constraints: RKAB and DMO compliance

There are reports suggesting that exporters may be required to prioritize domestic dispatches before proceeding with exports. Furthermore, the transition from a three-year Rencana Kerja & Anggaran Biaya (RKAB), or Mining Work Plan and Budget, approval cycle to an annual review mechanism has introduced greater operational uncertainty. This regulatory overhang has led certain exporters to scale back export volumes, thereby tightening spot availability in key importing markets, including India.

“It is understood that companies issued with RKAB are yet to fulfill their DMO obligations. Market sources suggest that PLN (for state owned electricity company) shipments may need to be completed before export activities can commence; however, there is currently no official clarity on the matter.”, quoted an Indonesian miner.

Despite concerns over export moderation, the availability of lower-grade (3,400 GAR) coal remains relatively stable. Approximately 5-6 vessels carrying 3,400 GAR material are currently stationed at Navlakhi, with total coal stock at the port estimated at around 4 lakh tonnes (t). Daily lifting continues at approximately 20,000 t per day, supported by steady industrial demand.

However, the higher-grade segment is witnessing constrained supply, contributing to stronger price momentum in the 4,200 and 5,000 GAR categories. The divergence in grade-wise availability has resulted in selective price escalation rather than a broad-based supply shortage across all categories.

Cost stock position at power plants in India

Coal stocks at Indian power plants stood at 57.9 mnt as of 12 February, equivalent to approximately 19 days of consumption. Although overall inventory levels remain stable, 21 power plants continue to operate under critical stock levels, including domestic coal-based plants, imported coal-based plants, and washery reject-based units. This mixed inventory position is likely to sustain procurement activity in the near term.

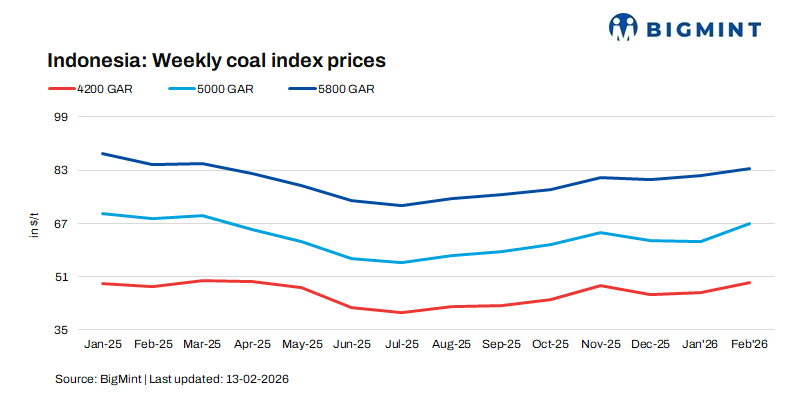

Indonesian benchmark price trends

Indonesian weekly benchmark prices also recorded w-o-w gains, mirroring tightening export availability and cautious buying sentiment. During the period, 5,800 GAR coal prices increased by $1.26/t, 4,200 GAR by $ 2.42/t, and 3,400 GAR by $ 0.73/t. The comparatively stronger gains in mid-grade benchmarks align with the tighter supply dynamics observed in the Indian market.

Market outlook

In the near term, Indian portside prices are expected to remain firm, particularly in the 4,200-5,000 GAR segments, unless greater clarity emerges regarding Indonesia’s RKAB approvals and DMO compliance framework.

Key factors influencing the outlook include:

- Regulatory clarity in Indonesia: Any formal resolution or streamlining of RKAB approvals could ease export constraints and moderate price momentum. Conversely, stricter enforcement of DMO commitments may further restrict export availability.

- Grade-specific supply tightness: Lower-grade 3,400 GAR coal is likely to remain relatively stable due to adequate inventories, while mid- and higher-grade coal may continue to trade at a premium.

- Power sector demand: With summer approaching and inventories unevenly distributed across power plants, spot demand may remain resilient.

Overall, the market sentiment remains cautiously firm in the short term, with price volatility closely linked to policy developments in Indonesia and procurement strategies of Indian end-users. Notably, India imported 163 mnt non-coking coal in CY’25, out of which share of Indonesia was 60%.

Leave a Reply