- Weak Asian demand drives volume decline

- Supply tightness supports prices despite soft demand

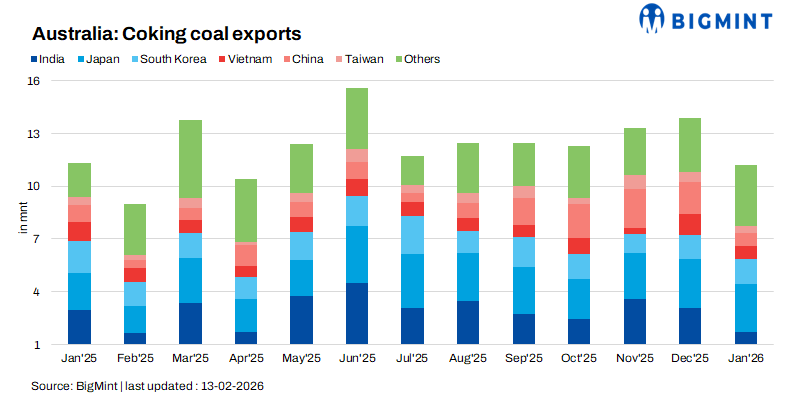

Australia’s coking coal exports stood at 11.21 million tonnes (mnt) in January 2026, marking a 19% month-on-month (m-o-m) decline from 13.86 mnt in December 2025. Y-o-y, exports were marginally lower by 1% compared to January 2025, indicating relative stability annually but significant short-term volatility.

The monthly decline can be attributed to a combination of weaker downstream steel demand across key Asian markets, seasonal production adjustments, and logistical or weather-related disruptions that typically impact shipments at the beginning of the year.

Diverging demand trends across Asia

India remained a key importer in January, though volumes declined sharply by 44% m-o-m to 1.72 mnt. The drop was primarily due to the sharp spike in prices post-December which instilled caution in buyers.

Japan’s coking coal imports also declined 3.2% m-o-m to 2.69 mnt, reflecting ongoing steel production cuts and subdued domestic demand. Structural headwinds and slower industrial activity continue to constrain raw material consumption.

China’s imports fell sharply by 58% m-o-m to 0.75 mnt in January, driven by policy-led supply adjustments, tighter import controls, and weak steel sector activity. Increased domestic coal availability and greater reliance on Mongolian supplies further reduced demand for Australian cargoes.

In contrast, South Korea’s imports rose by 7% m-o-m to 1.47 mnt, suggesting relatively stable blast furnace operations and restocking activity. The increase indicates moderate resilience in Korean steel output compared to other regional peers.

Taiwan’s imports declined by 27% m-o-m to 0.41 mnt, while Vietnam registered a 39% m-o-m drop to 0.72 mnt.

Overall, the regional picture reflected uneven steel sector performance, with most markets experiencing demand moderation at the start of the year.

Port-wise export performance

Dalrymple Bay Coal Terminal (DBCT) reported a 41% m-o-m decline in shipments at 3.06 mnt, potentially impacted by weather disruptions, maintenance schedules, or vessel congestion. Haypoint Port also recorded a 15% m-o-m decrease, with exports falling to 2.49 mnt. Similarly, Abbot Point experienced a sharper contraction of 35% m-o-m, with shipments totaling 0.9 mnt.

In contrast, Gladstone registered a 7% m-o-m increase in shipments at 2.49 mnt, reflecting comparatively stable loading operations. Among smaller ports, Port Kembla recorded nil shipments in January.

Supply disruptions support price recovery

Australian coking coal prices strengthened in January, rising by approximately $22/t m-o-m compared with December 2025. The price recovery was primarily supported by supply-side disruptions, which tightened spot availability despite weaker demand fundamentals. Seasonal weather-related constraints and logistical challenges further contributed to the recovery.

Outlook

Australia’s coking coal exports may remain volatile in February due to weather and logistical disruptions; however, ongoing steel output cuts may limit volume recovery. A rebound in Asian steel production in Q2 2026 may play a key role in boosting stronger trade flows.

Leave a Reply