- Longs demand remains tepid despite firm inputs

- QCO extension eases near-term supply bottlenecks

India’s stainless steel finished market remained largely unchanged week-on-week, as volatile nickel prices and limited spot buying kept transactions thin. A firmer rupee weighed on export competitiveness, while domestic buyers adopted a wait-and-watch stance despite firm alloy input costs. Mills indicated that expectations of demand recovery post recent trade developments failed to materialise, particularly in the longs segment.

Flats segment steady on policy support

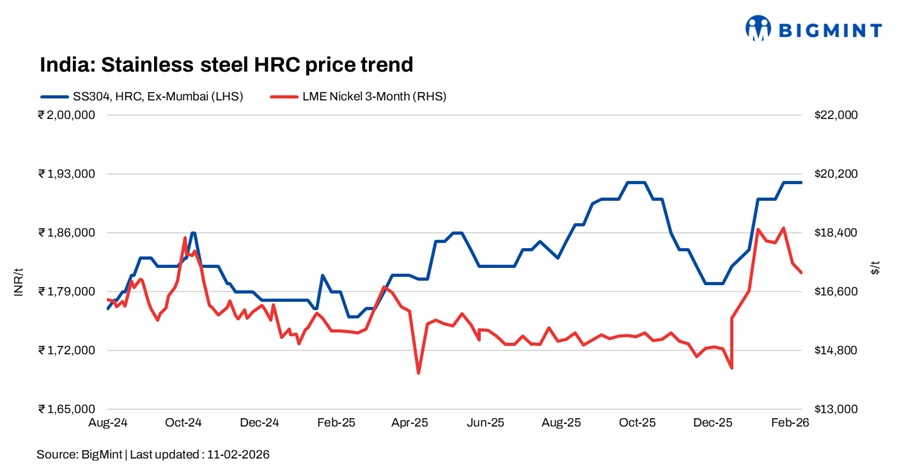

BigMint’s benchmark 304 HRC remained unchanged at INR 192,000/t ex-Mumbai, while 316 HRC held steady at INR 343,000/t w-o-w. In China, 304 CRC stood at RMB 14,750/t ($2,134/t) exw, with export offers at $2,050/t FOB.

In the import segment, POSCO’s 1250 width HR coils were heard at $1,962-1,973/t (INR 178,000-179,000/t) and CR coils were heard at $2,017-2,028/t (INR 183,000-184,000/t), while 1500 width HR coils were heard at $2,039-2,050/t (INR 185,000-186,000/t) and CR coils were heard at $2,094-2,149/t (INR 190,000-195,000/t).

Additionally, The government’s extension of key Quality Control Order (QCO) compliance deadlines until March 2026 has provided temporary relief across the supply chain. Stainless steel flats, especially 200- and 300-series grades facing domestic supply gaps, may see smoother import flows for shipments dispatched before the deadline, even if not fully BIS-compliant.

Longs demand fails to reflect alloy strength

Finished longs remained under pressure, with 304L black round bars (25–100 mm) stable at INR 165,000/t ex-Mumbai and 316L at INR 280,000/t.

A mill source noted that while “LME nickel and molybdenum are firm due to disruptions in the US, this strength is not translating into longs demand.”

Chinese stainless steel, NPI prices

In China, domestic stainless steel 304-grade CRC prices stood at RMB 14,750/t ($2,134/t) exw, while FOB tags for 304-grade CRC stood at $2,050/t. Indonesian FOB prices of nickel pig iron (NPI) (12-14%) were assessed at $137/t, while NPI (10-12%) stood at $136/t.

LME nickel prices

Benchmark three-month nickel prices on the London Metal Exchange (LME) stood at $17,185/t on 10 February, down around 2% w-o-w from $17,540/t. LME-registered nickel stocks were reported at 285,750 t, largely stable compared with 285,528 t in the previous week.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices increased by INR 167,000/t ($1,844/t) compared to the previous assessment on 4 February. The rise was driven by higher seller offers, supported by the upward trend in global markets and firm LME prices, along with steady demand from the end-user sector. In addition, molybdenum oxide shortage was reported in the global market leading to the rise in prices.

As per BigMint’s assessment on 11 February, ferro molybdenum prices stood at INR 3,243,000/t ($35,808/t) exw India.

Ferro chrome: Indian high-carbon ferro chrome (HC 60%) prices increased by INR 4,600/t w-o-w to INR 124,600/t exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices stayed unchanged in comparison to the last assessment on 2 February. Prices were stable as the market largely operated at Bhutans February offer price of INR 95,000/t ($1,049/t) exw.

Ferro silicon prices in India and Bhutan were INR 95,000/t ($1,049/t) exw, as per BigMints assessment on 9 February.

Ferrous scrap: India’s imported scrap market stayed subdued as ample domestic scrap and cautious mill buying kept activity limited. HMS 80:20 held at $335-340/t CFR and shredded at $365-368/t CFR, with selective buying supported only by a mild rupee improvement.

UAE shredded at $395/t and small deals included car bales at $218/t CFR Chennai and Australian offers remained stable, with workable HMS levels at $350-360/t across Chennai and Mundra.

Outlook

Stainless steel prices are expected to remain firm in the near term, supported by alloy cost strength and policy relief on imports. However, subdued demand in the longs segment and currency-led export pressure may cap any sharp upside.

Leave a Reply