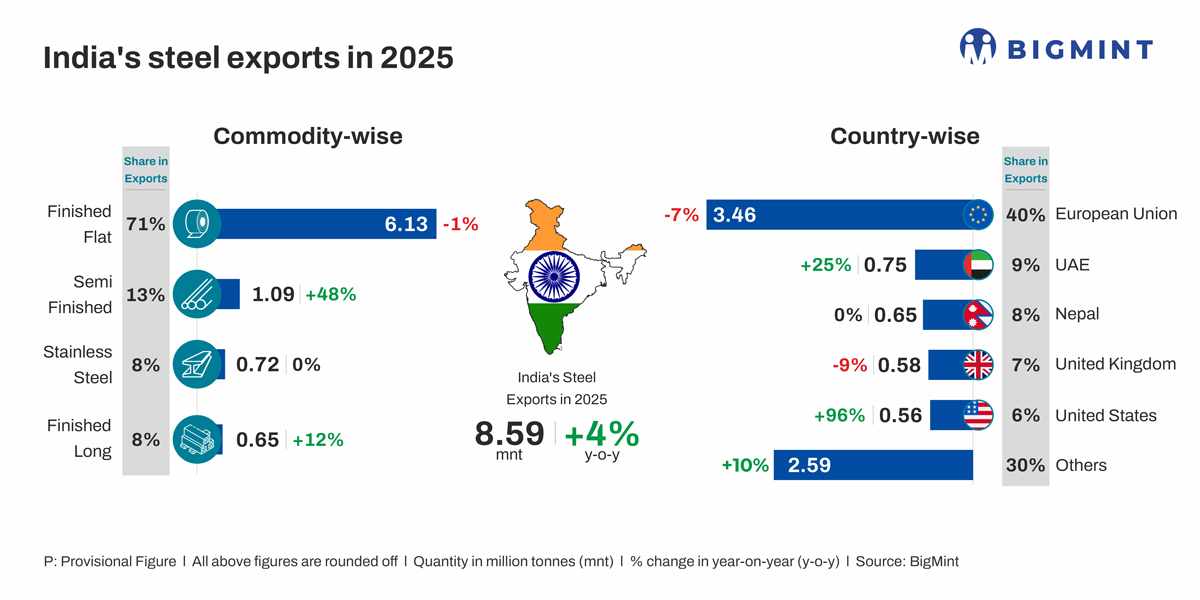

- EU sentiment cautiously positive on tighter imports

- ME offers remain absent amid better domestic realisations

BigMint’s India HRC (S275) export index for the European Union (EU) rose by $25/t w-o-w to $575/t FOB main port on 10 February, up from $550/t a week earlier, driven by higher domestic EU prices. Meanwhile, in the Middle East, Chinese offers remained competitive, while no firm offers from India were heard due to higher domestic realisations.

1. HRC offers to the EU: Indian HRC export offers to the EU rose by $25/t w-o-w to $625/t CFR Antwerp, up from $600/t CFR a week earlier. This increase mainly reflected higher domestic price levels in Europe, supported by tighter import availability under the CBAM framework. European mills have continued pushing prices upward as import volumes remain limited, while expectations of stricter safeguard measures are also likely to further restrict inflows. As a result, overseas suppliers adjusted offers upward. Overall sentiment in the EU stayed cautiously positive due to these regulatory factors, although demand fundamentals remained weak, with subdued downstream consumption and buyers still largely resisting higher prices.

2. HRC offers to the Middle East: Indian HRC export offers to the Middle East remained absent w-o-w, as Indian mills were not making any firm offers to the region due to better realisations in the domestic market. Indian trade-level HRC prices rose by INR 100/t ($1/t) w-o-w to INR 53,900/t ($595/t) exw-Mumbai on 6 February, while the monthly average price for January stood at INR 52,000/t ($574/t), up by INR 4,900/t ($54/t) m-o-m.

Meanwhile, Chinese HRC export offers to the Middle East remained stable w-o-w at around $500/t CFR UAE. May 2026 HRC contracts on the Shanghai Futures Exchange (SHFE) declined by RMB 42/t ($6/t) w-ow to RMB 3,226/t ($467/t) on 10 February from RMB 3,268/t ($473/t) on 3 February 2026.

Outlook

In the coming week, Indian HRC export offers to the EU are expected to remain supported by higher domestic European prices, tighter import availability under CBAM, and expectations of stricter safeguard measures. In the Middle East, Indian offers are likely to remain absent as long as domestic realisations stay more attractive, while competitive Chinese export offers are expected to continue exerting pressure on the market.

Leave a Reply