- Supply-demand imbalance keeps BF prices supported

- IF-rebar segment witnesses demand slowdown

Indian primary steelmakers increased rebar prices by up to INR 1,000/tonne (t) ($11/t) this week, sources informed BigMint. Post-revision, list prices stood at INR 58,000-59,500/t ($640-656/t) on landed basis.

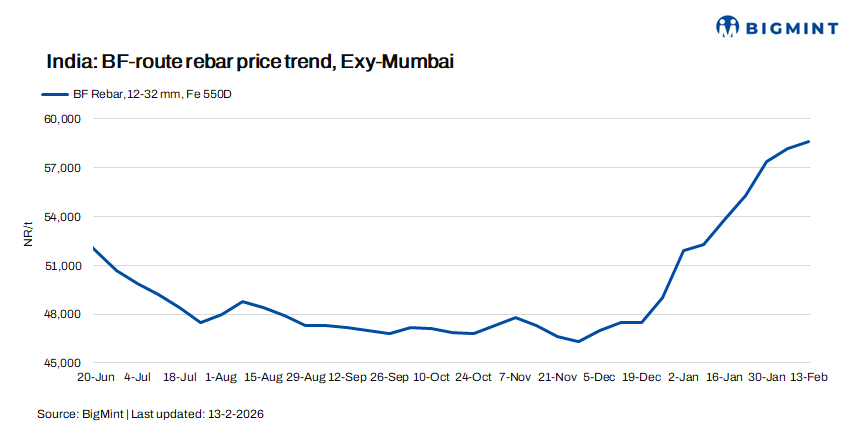

Trade-level BF-rebar prices (distributor to dealer) rose by INR 400/t ($4/t) w-o-w to INR 58,600/t ($646/t) exy-Mumbai, as per BigMint’s assessment on 13 February 2026. Market participants noted that buyers were reluctant to place fresh orders at elevated price levels following the recent sharp price increase, leading to cautious procurement behaviour.

In the projects segment, prices hovered at around INR 59,000-60,000/t ($651-662/t) FOR basis. Demand from the projects segment remained steady with dispatches of previously booked orders.

Update on projects

- L&T’s Transportation Infrastructure vertical won a contract to upgrade Latifa Bint Hamdan Street, Dubai, including road widening and interchange construction, to enhance traffic flow.

- G R Infraprojects Limited emerged as L-1 bidder for a INR 1,897.51 crore EPC railway project under West Central Railway, Madhya Pradesh, with a 900-day completion timeline.

- Dilip Buildcon Limited received PNGRB authorisation for developing, operating, and maintaining an ATF pipeline from Navgam to Ahmedabad airport, with EPC works worth INR 124 crore.

Factors shaping market dynamics

1. Supply-demand imbalance: Strong material lifting in the previous month led to significant liquidation of inventories at mill yards, resulting in tighter availability across select rebar sizes. Additionally, the shutdown of blast furnace-3 (BF3) at Vijayanagar of a leading private steelmaker for capacity upgradation since September 2025 has constrained production. With commissioning expected by the end of Q4 FY26, capacity utilisation at Indian operations remained impacted in January.

Consequently, the current supply-demand imbalance has led to limited material availability in the distribution channel. Trade participants indicated that “major mills are operating with restricted inventories and are largely booked for nearly a month due to ongoing project commitments, thereby limiting spot supplies and creating shortages in certain sizes”. Notably, inventory levels at primary mills fell by around 40% m-o-m in early-February.

2. IF rebar prices show mixed trends w-o-w: IF rebar trade prices exhibited mixed trends w-o-w across major Indian markets. Trading activities in the finished segment was subdued this week, marked by limited volumes and largely need-based buying after recent procurements. Elevated price levels prompted cautious purchasing, while sluggish demand led to prices softening in key markets. Sellers reduced their offers or increased discounts amid cautious market sentiments. Inventory days stood at 8-10 days. IF rebar prices were stable w-o-w at INR 49,600/t ($547/t) exw-Mumbai as on 13 February.

The BF-IF rebar price spread in Mumbai widened to around INR 8,500-9,000/t ($94-99/t) due to a sharper hike in BF-rebar prices recently. IF rebars continue to dominate the Indian market with a 65-70% share.

3. Property registrations drop y-o-y: Property registrations in Mumbai, the country’s largest real estate market, dropped by 8% on the year to 11,219 units in January, as per data released by Knight Frank India. Likewise, monthly registrations were down 32% as against 16,415 units reported in December last year.

Mumbai’s property registrations declined in January 2026 mainly due to a high base effect after December’s year-end surge and elevated property prices delaying fresh purchase decisions, despite steady buyer interest and stable stamp duty collections.

Outlook

Market participants anticipate that the pace of price increase will decrease in the coming weeks due to a slight drop in buying interest.

Leave a Reply