- SECL auctions record selective, need-based participation

- Lower South African exports tighten prompt availability

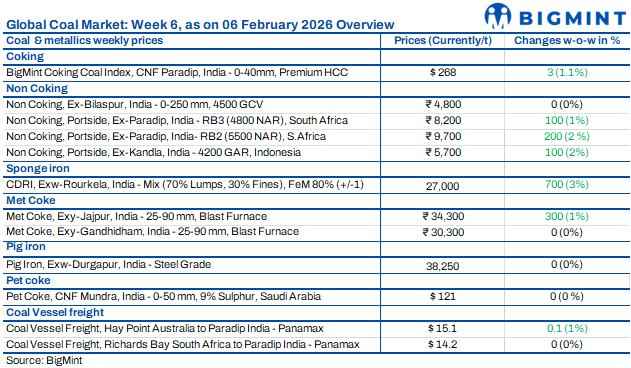

Indian coal markets reflected a firm yet cautious tone in the week ended 7 February 2026. Uncertainties regarding South African and Indonesian thermal coal supply supported seaborne prices, while domestic coal remained stable with disciplined auction participation. Freights stayed supported despite weak underlying demand. Sponge and industrial buyers largely covered near-term needs, limiting aggressive procurement. Overall sentiment remained balanced, with supply-side constraints offsetting subdued end-user enthusiasm.

Indonesian thermal coal prices edge higher on production cut rumours

Imported Indonesian thermal coal prices at Indian ports increased w-o-w amid supply uncertainty. 5,000 GAR rose INR 50/t to INR 7,300/t at Kandla and INR 7,200/t at Vizag, while 4,200 GAR gained INR 100/t to INR 5,700/t and INR 5,600/t respectively. 3,400 GAR remained at INR 4,500/t at Navlakhi. Regulatory uncertainty and expectations of possible Indonesian output cuts supported prices, though adequate inventories may limit sharp upside in the near term. ESDM raised thermal coal benchmarks for the first half of February across all grades except HBA-II on firm utility demand.

Portside South African thermal coal prices rise as exports plunge

South African thermal coal prices at Indian ports extended gains w-o-w amid tight stocks. Exw-Paradip 5,500 NAR increased INR 200/t to INR 9,700/t and 4,800 NAR rose INR 50/t to INR 8,150/t, while Vizag 5,500 NAR gained INR 100/t to INR 9,500/t. FOB levels were near $85/t, with CNF around $100/t. South African non-coking coal exports declined 33% m-o-m to over a one-year low of 4.03 mnt in January, tightening supply. Sponge iron CDRI rose INR 700/t to INR 27,000/t exw-Rourkela, while improving South African logistics may limit further upside.

Domestic non-coking coal prices remain stable

Domestic non-coking coal prices remained unchanged w-o-w, with 5,000 GCV at INR 5,750/t and 4,500 GCV at INR 4,800/t. Market offers stayed steady, supported by consistent supply through SECL auctions. On 31 January, SECL offered 554,000 t and allocated 128,100 t, significantly lower than 915,200 t sold on 27 January. Subsequently, on 3 February, 380,050 t of G11 from RLS Laxman mine were offered, and the entire quantity was allocated, indicating balanced and need-based procurement.

Indian met coke prices rise further

Indian blast furnace and foundry grade metallurgical coke prices increased w-o-w on 4 February, supported by higher raw material costs and firmer imported offers. BF-grade 25-90 mm in east India rose INR 300/t to INR 34,300/t ex-Jajpur, while west India remained stable at INR 30,300/t ex-Gandhidham. Foundry-grade stood steady at INR 36,100/t ex-Rajkot. Indonesian met coke offers increased $5-10/t w-o-w, with a 30,000 t cargo concluded at $249/t FOB for April laycan. CFR indications were above $270/t. The market is expected to remain firm with mild upside bias.

Global pet coke prices stay firm

Global pet coke markets remained firm in early February, supported by steady buying from India and the Mediterranean. India continued as the highest-priced major destination, with CNF levels at $121-122/t and bids at $116-118/t. Turkish trades converged at $108-110/t CIF, while FOB US Gulf Coast (USGC) prices strengthened, and 2% sulphur material held near $145/t FOB US West Coast (USWC). Limited supply and firm cement demand kept prices elevated, with downside risks seen only if freight or demand weakened sharply.

Nayara marginally raises pet coke price

Nayara Energy raised its pet coke price by INR 90/t (0.6%) m-o-m to INR 15,370/t with effect from 1 February, from INR 15,280/t. The revised level was 11% higher y-o-y compared with INR 13,850/t and 5.6% above the 12-month average of INR 14,463/t. The increase remained modest but reflected steady domestic demand. RIL continued full captive consumption and did not declare market prices, which kept open market availability tight and supported Nayara’s firmer realisation.

Coal freights stay supported

Dry bulk coal freights to India remained firm w-o-w despite weak demand and limited fixtures. The Baltic Dry Index fell 66 points to 1,936, with Panamax was down 57 points to 1,659, while Supramax rose 40 points to 1,102. DCE coke futures for May declined RMB 47.5/t to RMB 1,698.50/t or $244.8/t, reflecting a weaker steel outlook. Firm bunker prices kept owners resistant to lower bids, widening the bid-offer gap. Route-wise, Australia-Paradip rose $0.1/dmt to $15.1/dmt, Richards Bay-Paradip stayed at $14.2/dmt, and Indonesia-Navlakhi remained at $11/dmt amid limited Indonesian spot exports. Rates are expected to stay largely stable next week.

Leave a Reply