- Pakistan’s buying offsets muted domestic scrap demand

- Selective restocking limits near-term price upside

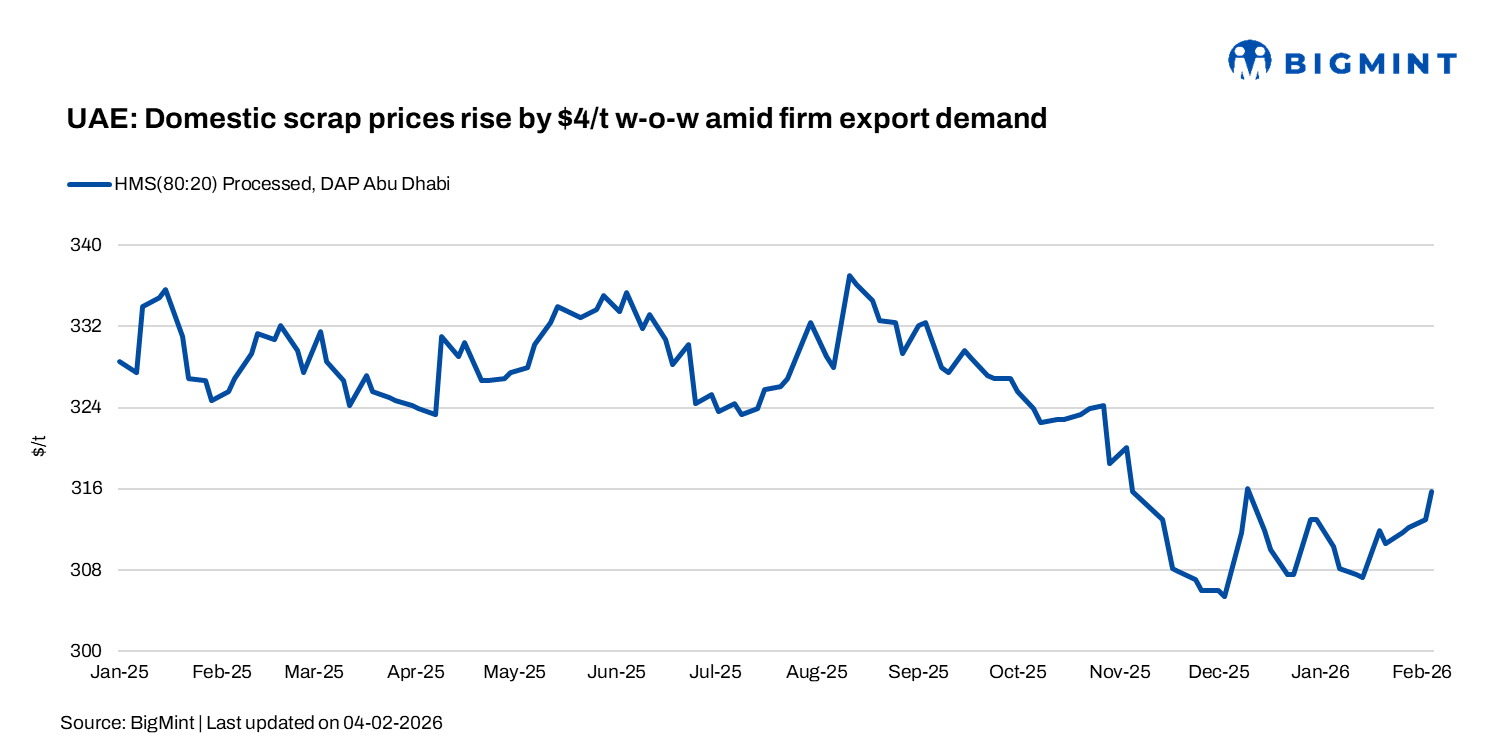

Scrap prices in the UAE edged up modestly in the week ended 6 February, rising by around AED 13/t ($4/t) w-o-w, supported by firm export demand, particularly from Pakistan. Despite the uptick, trading activity remained subdued.

Last heard, levels were at around AED 1,150-1,160/t ($313-316/t) for processed HMS and AED 1,210/t ($330/t) for shredded scrap. However, no firm offers have emerged in recent days, with market participants largely adopting a wait-and-watch stance amid thin spot activity, a UAE-based trader said.

The prices below were heard from the market (excluding 5% VAT)

- HMS 80:20: AED 1,100-1,120/t ($300-305/t)

- HMS 80:20 (processed): AED 1,160-1,170/t ($316-319/t)

- HMS shredded: AED 1,230-1,245/t ($335-339/t)

- PNS unprocessed: AED 1,140-1,170/t ($311-319/t)

- Fabrication scrap: AED 1,230-1,250/t ($335-341/t)

Export market

UAE-origin scrap offers to Pakistan stayed firm, with shredded scrap quoted at around $400/t CFR Qasim and sheared HMS at $375/t CFR. A deal was heard for HMS 80:20 at $370/t CFR Qasim for 300-400 t shipment, while a larger 1,000 t shredded shipment traded at $398/t CFR. GI bundle offers were reported in the $366-370/t CFR range, reflecting varied quality and buyer selectivity.

GCC steel market

The GCC rebar market recorded divergent price trends in February, reflecting uneven demand momentum and differing procurement strategies across the region. Prices increased in the UAE, Saudi Arabia, and Bahrain, while in Kuwait, they remained largely stable amid cautious buying behaviour.

In the UAE, benchmark rebar offers were assessed at around $721/t CPT Abu Dhabi, unchanged m-o-m. However, tradable levels strengthened by $15-20/t, supported by steady construction activity and firmer buying interest. Market participants noted limited discounting, allowing producers to maintain price discipline despite ongoing import competition.

Saudi Arabia also posted gains, with the benchmark producer’s offer at approximately $603/t delivered, while the wider market range rose by around $19/t m-o-m. Price support stemmed from selective restocking and improved mill sales compared with late 2025, although project-driven demand remains uneven.

In Bahrain, rebar prices edged up modestly, with benchmark offers at $583/t exw, up $2/t m-o-m, reflecting subdued demand and cautious procurement. In contrast, Kuwait held steady, with benchmark prices at $559-562/t exw, as adequate inventories capped any upside.

Despite the upward bias in parts of the region, market participants cautioned that price sustainability will depend on mills’ ability to convert firmer offers into confirmed bookings amid selective buying.

Separately, Jindal Steel Oman completed a modernisation upgrade at its Sohar Steel rebar rolling mill, installing an automated bar counting system supplied by Dalian Baosteel Metallurgy Group. The upgrade enhances operational efficiency, accuracy, and consistency.

Outlook: UAE scrap prices are expected to remain rangebound in the near term, supported by firm export demand but capped by subdued domestic trading interest. In the GCC steel market, rebar prices may hold steady, with sustainability dependent on actual booking volumes amid selective buying and uneven project execution.

Leave a Reply