- India steady, Pakistan subdued as Ramadan nears

- Bangladesh stable; Turkiye softens on weak rebar demand

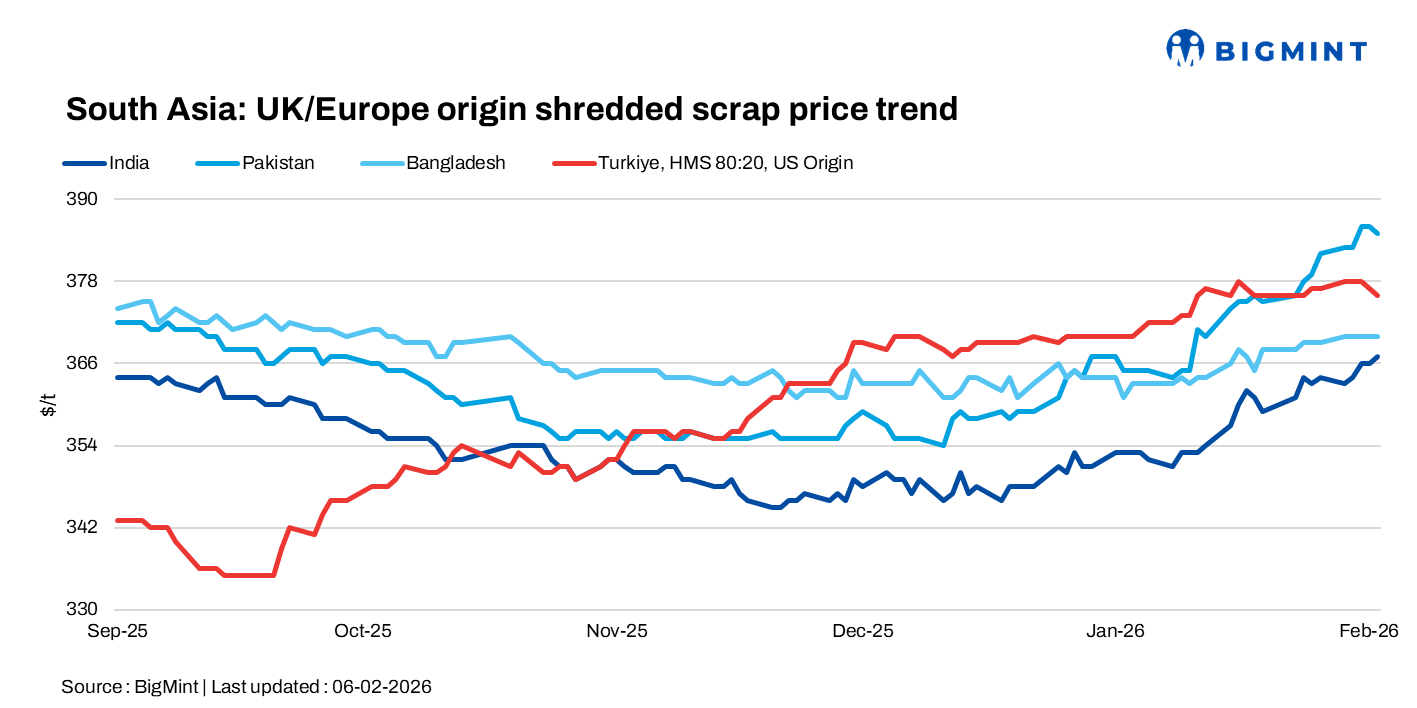

South Asia’s imported scrap market stayed mixed on 6 February, with India seeing steady but highly price-sensitive buying, Pakistan subdued ahead of Ramadan, and Bangladesh stable amid tight local supply, while Turkiye softened as mills resisted higher offers under weak rebar demand and squeezed margins.

Region-wise highlights

India: Imported scrap sentiment in India stayed steady, although no major EU/UK deals were heard as collection costs there continued to rise, pushing offer levels higher. Workable prices emerged through small containerised bookings into Chennai, including LMS bundles near $314/t CFR, turnings around $319/t CFR, tin-can bundles near $265/t CFR, HMS 80:20 around $325/t CFR from Central America, and Australian HMS 80:20 near $342/t CFR. These deals broadly indicate the current buying comfort in the market.

Fresh offers to Mundra showed US-origin workable levels at $320/t for blue turnings, $360/t for HMS 1, $380/t for blue steel scrap and $370/t for PNS. Other regional indicators include Bahrain HMS 1 near $355/t and South Africa HMS around $340-345/t CFR.

Pakistan: Imported shredded scrap sentiment in Pakistan remained steady, though buying activity stayed muted. Qasim buyers showed limited interest after offers neared $390/t, while freight for Karachi remained comparatively higher earlier in the week. Market participants noted that Pakistan has been largely quiet for the past 3-4 days, with only selective deals taking place ahead of the expected Ramadan-driven slowdown.

Bangladesh: Imported ferrous scrap prices in Bangladesh remained largely unchanged, with PNS from Malaysia/Singapore offered around $380/t CFR Chattogram and HMS 90:10 near $370/t. Offers from Australia also stayed steady with HMS 1 at $355-360/t. Tight domestic scrap availability and pre-election positioning supported a mild uptick in buying sentiment despite limited overall activity.

Turkiye: Imported scrap market softened on 6 February as mills resisted higher offers amid weak domestic and export rebar demand. Buyers pushed back against levels above $375/t CFR, with margins squeezed and the scrap-rebar spread narrowing to an unworkable $175/t. European offers hovered around $372-373/t CFR and a US HMS 90:10 cargo was indicated near $382/t CFR, but limited finished steel orders and poor mill profitability suggest elevated deep-sea prices are unlikely to hold.

Leave a Reply