- Billet prices jump INR 1,500/t w-o-w

- Slow import arrivals tighten local availability

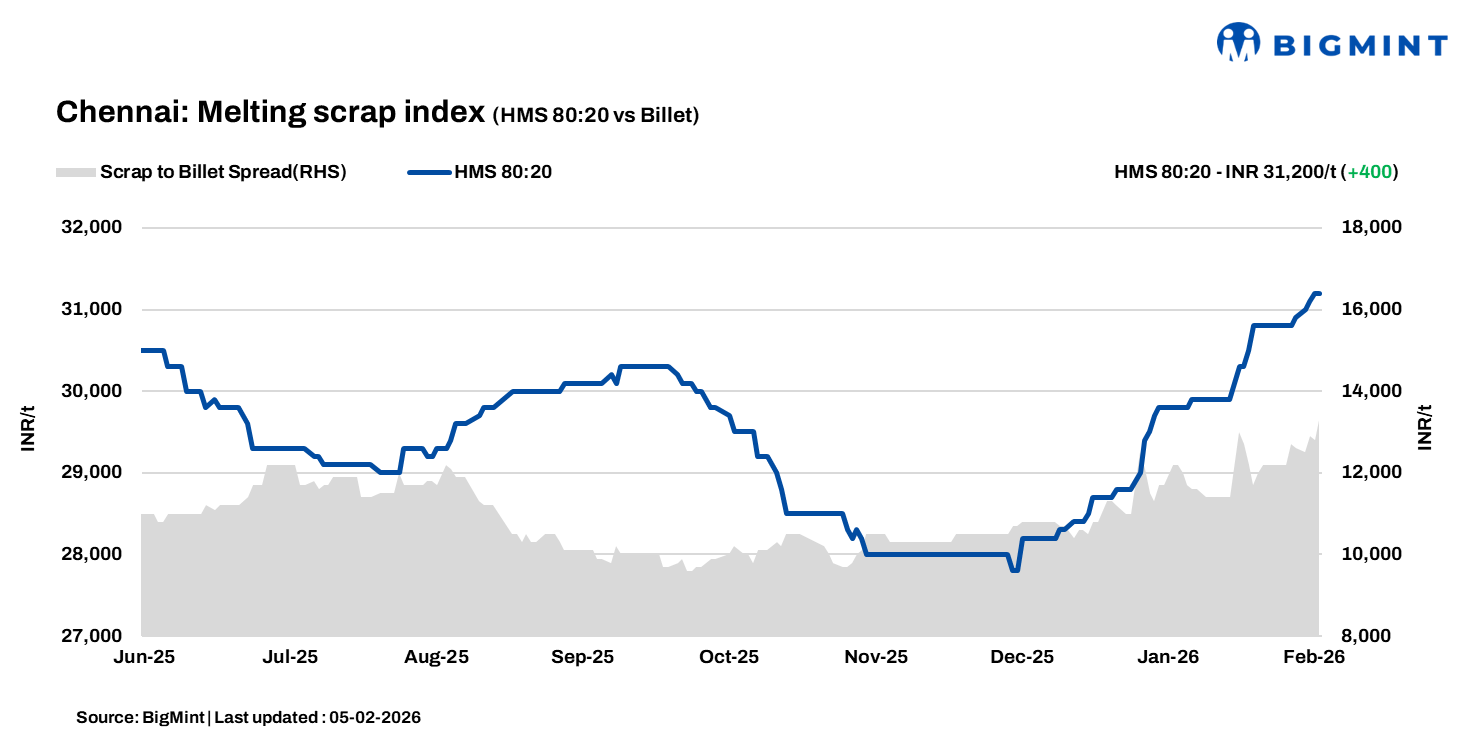

Ferrous scrap prices in Chennai strengthened w-o-w, supported by higher semi-finished steel prices and tightening supply dynamics. BigMint’s latest assessment showed HMS (80:20) scrap at INR 31,200/t on 5 February 2026, up INR 400/t w-o-w, while remaining unchanged day-on-day. The uptrend was reinforced by a sharp rise in billet prices, which increased by INR 1,500/t w-o-w to INR 44,500/t, improving the scrap-to-steel conversion economics.

Domestic scrap market gains traction

Improved rebar realisations encouraged mills to stay active in the scrap market, although procurement remained largely requirement-driven. Domestic HMS (80:20) scrap transactions were reported in the range of INR 31,000-31,500/t, depending on payment terms and volumes. Spot deals with immediate payment were concluded at INR 31,000-31,300/t, while extended-credit transactions fetched premiums, settling at INR 31,800-32,000/t.

Mill opening prices reflected firm sentiment across Chennai clusters. In Kanchipuram and Gummidipoondi, HMS (80:20) was quoted at INR 31,200-31,300/t DAP, while HMS (90:10) stood higher at INR 32,300-32,400/t DAP.

Imports remain slow, sponge availability tight

Imported scrap arrivals stayed sluggish, lending further support to domestic prices. Shredded scrap offers were heard at $350-355/t CFR Chennai, while HMS (80:20) was quoted at $335-340/t CFR, with buyers bidding $5-10/t lower. A stronger US dollar and comparatively cheaper domestic scrap continued to curb aggressive import bookings.

On the raw material front, rising iron ore and pellet prices prompted sponge iron producers to divert output toward captive consumption, reducing merchant availability. Mills increasingly channeled billets into rebar production as margins remained favourable. Rebar demand was described as moderate, with inventories comfortable at 10–12 days. A local scrap supplier noted that improved rebar offtake has eased liquidity stress, enabling timely payments and supporting higher scrap prices.

Outlook

Chennai scrap prices are expected to remain firm in the near term, supported by higher steel prices, slow imported scrap arrivals, and captive sponge iron consumption. However, moderate demand and cautious mill procurement could cap further upside, with prices likely to fluctuate within a narrow band of INR 200-500/t.

Leave a Reply