- Buyers remain cautious due to elevated prices

- Scrap, cathode supply remains comfortable

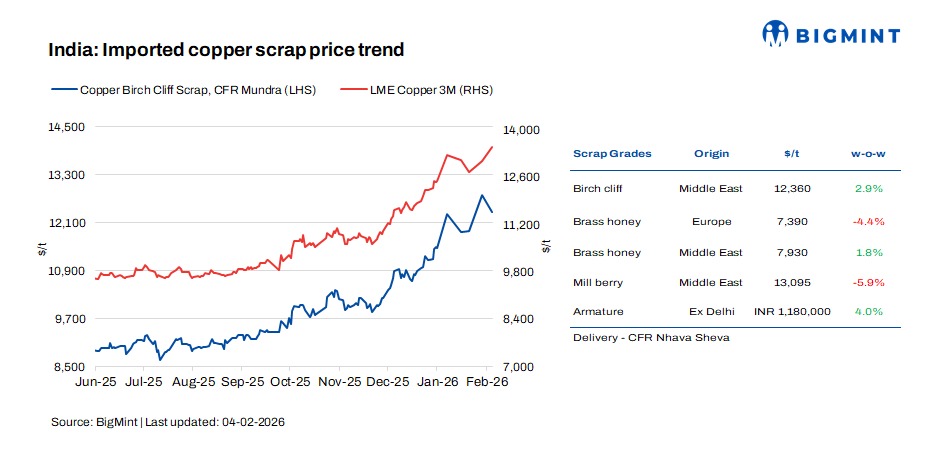

Imported copper scrap prices in India surged w-o-w on 4 February, tracking a rebound in benchmark copper futures on the London Metal Exchange (LME). Domestic copper scrap prices also moved higher.

According to BigMint’s assessment, Middle East-origin Birch Cliff scrap was assessed at $12,390/t CFR Mundra, up sharply by 1.5% w-o-w, while Armature scrap prices jumped 4% w-o-w to INR 118,0000/t ex-Delhi. US Motors mix prices also strengthened notably, rising 1% w-o-w to around $1,450/t CFR Mundra.

LME copper rebounds

LME three-month copper prices rebounded during the week, rising 3.1% to $13,480/t today.

Indian market updates

In India, buyers were very careful due to high LME prices and uncertain margins. A trader stated, “Even though demand exists, profitability is tight, so no one wants to overpay.” Importers and rod mills were mostly buying only what they immediately needed, not stocking up.

Motors scrap demand remained firm, with trades heard at around $1450-1,500/t. However, buying activity was cautious, with consumers largely focusing on smaller, hand-to-mouth purchases. Scrap suppliers noted that inventories were manageable, though higher LME prices pushed overall scrap valuations higher.

Market participants shared, Copper cathode spot premiums were unchanged during the week, but sentiment remained soft. With availability improving, buyers held back from offering material, expecting premium levels to ease in the coming weeks.

Another player stated, “On the cathode side, availability has slightly improved, especially from Asia and Africa. This has reduced panic buying. From a global scrap angle, higher prices are bringing more scrap into the market, but demand is not strong enough to create shortages. Sellers are willing to sell at high prices, but buyers are resisting, leading to slower trade flow. Overall, the copper market is being pushed more by price movements on exchanges than by real demand on the ground. Until factories start buying more confidently, most players expect the market to remain volatile and cautious.”

Australia-origin Motors mix was offered around $1,350/t. Birch was heard at 90.5% of 3M LME, while Meatballs 20% were offered near $2,300/t. Brass Honey with 2% impurity was indicated at 59% of LME. Millberry was available at 99% of LME, while Candy Berry was priced at 97.25%. Druid was offered across grades, with the high grade at 93% (Few loads on a CIF Nhava Sheva basis), mid grade at 91%, and low grade at 89%.

Europe-origin #2 (Birch/Cliff) was indicated at 89.5-90.5% of LME, while Europe-origin #1 copper wire and tubes were at 96.5-97.5% of LME. Bare Bright (Millberry) of European origin is being heard at 97-98% of LME.

In recent times, sharp and frequent swings in LME copper prices have been complicating trade negotiations. As a result, sellers are increasingly moving away from percentage-based pricing and opting for fixed dollar-per-tonne discounts, which provide better price certainty amid ongoing volatility.

Overall, high and volatile copper prices continue to keep buyers on the sidelines. Scrap availability across Europe remains comfortable, leaving the physical market well supplied and limiting any near-term upside in prices.

Global market update

The broader European copper scrap market continued to trade in a quiet and cautious tone. Lower-grade material remained under pressure due to weak demand and elevated inventories at processors, although prices were largely stable w-o-w.

Chilean miner Antofagasta reported copper production of 177,000 t in Q4CY’25, up 9% q-o-q, supported by higher output across all operations. However, full-year CY’25 production fell 1.6% y-o-y to 653,700 t. Net cash costs dropped sharply by 27% y-o-y to a five-year low of $1.19/lb, aided by strict cost control and robust by-product credits. The miner’s CY’26 copper output guidance stood at 650,000-700,000 t.

Outlook

Copper demand remains strong, supporting higher prices. However, with ample availability and cautious buying at elevated prices, the market is expected to stay at around these levels, with volatility driven more by sentiment than by any immediate supply tightness.

Leave a Reply