- Margin pressure, tight supply support Turkish scrap prices

- Tight margins keep mills cautious, lead to price resistance

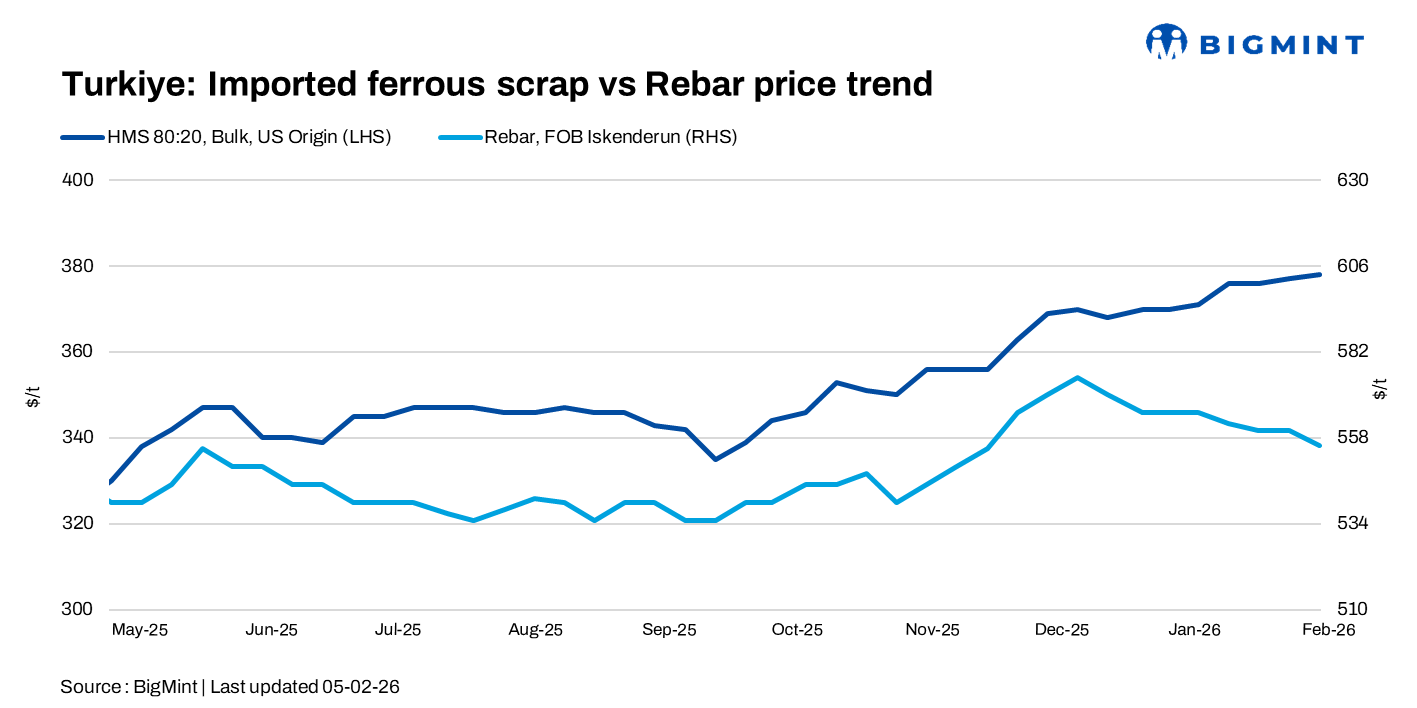

Turkish deep-sea imported ferrous scrap prices remained stable w-o-w as of 5 February, with sentiment largely steady. Tight scrap availability in the US and Europe, firm collection costs, and weather disruptions provided underlying support, while weak rebar demand and compressed mill margins kept buying measured and capped any upside.

Price assessments

- US-origin bulk HMS 80:20: $377/t CFR Turkiye, stable w-o-w.

- US East Coast HMS 80:20: $351/t FOB, up by $1/t w-o-w.

The scrap-to-rebar spread remained at $175-178/t, with rebar export offers at $555/t FOB.

Around three deals were reported in the $375-378/t CFR range, largely from US-origin.

Market commentary

Market participants noted persistent resistance from Turkish mills to higher prices, despite some easing in the euro. European exporters continued to face buyer pushback amid thin inflows and elevated collection costs, reported near EUR 270/t ($318/t). Scrap collection rates in parts of the Baltic region were said to be just 30-40% of normal levels.

US sellers targeted $380-385/t CFR amid tight domestic supply, with February shredded settlements expected to rise by $20-30/t. Severe winter conditions across the US East Coast and parts of Europe further constrained availability, supporting sell-side sentiment.

A major trader said market sentiment remains fragile, with only limited deals reported from the US and Baltic. European offers were heard at $372-373/t CFR, while a US-origin HMS 90:10 cargo was indicated near $382/t CFR. However, weak rebar demand and tight margins, with the scrap-rebar spread around $175-178/t, continue to curb mills’ willingness to accept higher prices, casting doubt on the durability of current levels.

On the buy side, some Turkish mills re-entered the market for March shipments, seeking faster loadings.

Turkiye’s scrap market continues to face structural pressure. In 2025, scrap imports fell as mills reduced scrap intake amid margin compression and increased reliance on ore-based metallics. US-origin shipments declined nearly 20%, while European volumes only partially offset the drop. HMS grades still accounted for about 55-60% of imports.

Producers increasingly shifted towards pig iron and HBI, with pig iron imports rising sharply and HBI intake nearly doubling. Higher semi-finished steel imports further displaced domestic scrap consumption. Capacity utilisation remained low at around 60-65%, with a cautious operating environment.

Outlook

Turkish imported scrap prices are expected to remain largely stable in early February. Tight supply, high collection costs, and weather disruptions should continue to support prices, but weak rebar demand, narrow margins, and selective mill buying are likely to cap any meaningful upside.

Leave a Reply