- Surge in finished steel prices supports pig iron uptrend

- Met coke imports fall by 9% m-o-m, add to cost pressures

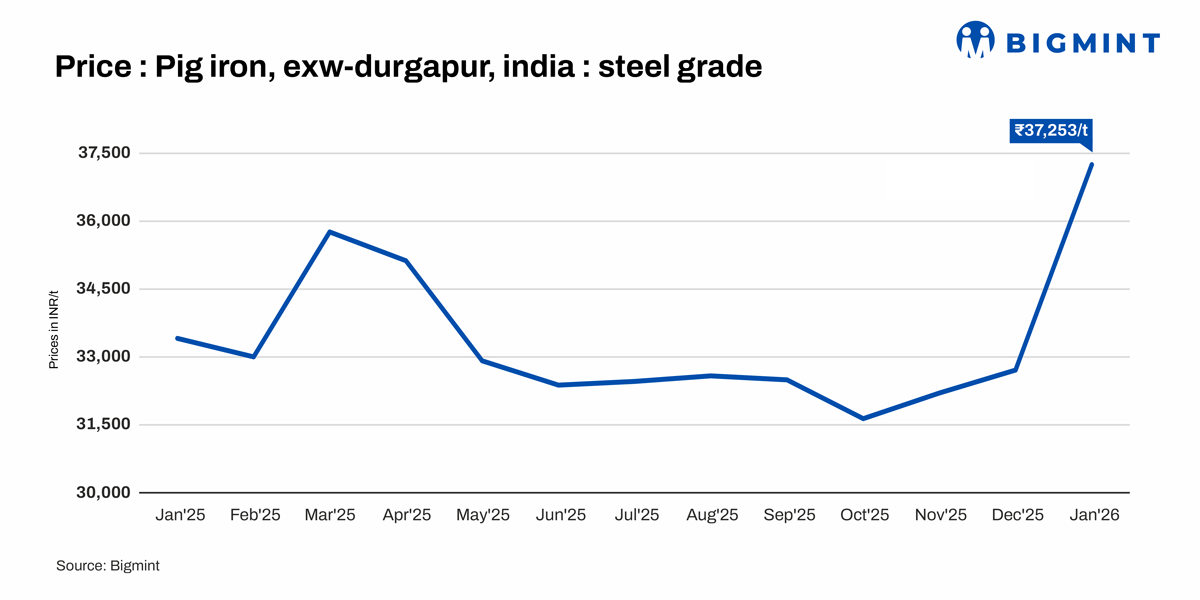

Indian pig iron prices increased moderately by around INR 2,250/tonne (t) m-o-m in January 2026, driven largely by rising raw material costs rather than a demand-side recovery. Prices strengthened steadily through the month, from around INR 35,750/t at the start of January to nearly INR 38,000/t by month-end, supported by a sharp increase in met coke prices, while buying activity remained cautious amid uneven downstream demand. Buyers largely limited purchases to immediate requirements, keeping overall volumes moderate.

Raw material cost pressure drives pricing

Met coke prices increased sharply during the month, from around INR 32,000/t in early January to nearly INR 34,000/t by month-end. The surge was triggered by an uptick in coking coal prices due to weather-related disruptions in Australia, which tightened global supply. Additionally, higher coking coal prices boosted demand for met coke, further squeezing availability. As met coke is the primary input for pig iron production, elevated costs directly translated into higher pig iron prices.

Supply-side data further explains the cost pressure seen during the month. Met coke availability declined by around 8.5% m-o-m, with volumes easing to 0.43 million tonnes (mnt) in January 2026 from 0.47 mnt in December 2025, tightening prompt supply. In contrast, coking coal availability remained largely stable, inching up marginally by 0.2% m-o-m to 5.50 mnt. The contraction in met coke availability, despite steady coking coal volumes, added to cost-side pressure and reinforced the upward movement in pig iron prices.

Rising finished steel prices support upward momentum

Additionally, the upward movement in pig iron prices was reinforced by strengthening finished steel prices during January. Domestic rebar prices climbed up by around INR 3,000-3,500/t m-o-m across major regions due to improved demand, supporting higher raw material pass-through. The firmer finished steel pricing environment encouraged pig iron producers to raise offers and absorb higher input costs, making it a key contributory factor behind the rise in pig iron prices alongside met coke inflation.

Auction activity offers mixed signals

Multiple auctions were conducted by NMDC and SAIL (BSP and RSP) in January 2026, though results were mixed. While some auctions achieved improved realisations on cost pressure, others saw limited participation as buyers resisted higher prices. NMDC’s auctions reflected mixed outcomes, with sold quantities declining in late January. SAIL RSP achieved strong realisations earlier in the month, though prices softened in subsequent auctions. Tata Metaliks auctions showed higher bids for both foundry- and steel-grade pig iron, indicating selective restocking.

Outlook

Market sentiment remains cautiously positive, supported by firm raw material prices and controlled supply. Further price direction will be dependent on downstream demand recovery and movements in met coke and coking coal costs.

Leave a Reply