- Active domestic demand for pellet in the east coast

- Realization gap continues to widen between domestic-exports

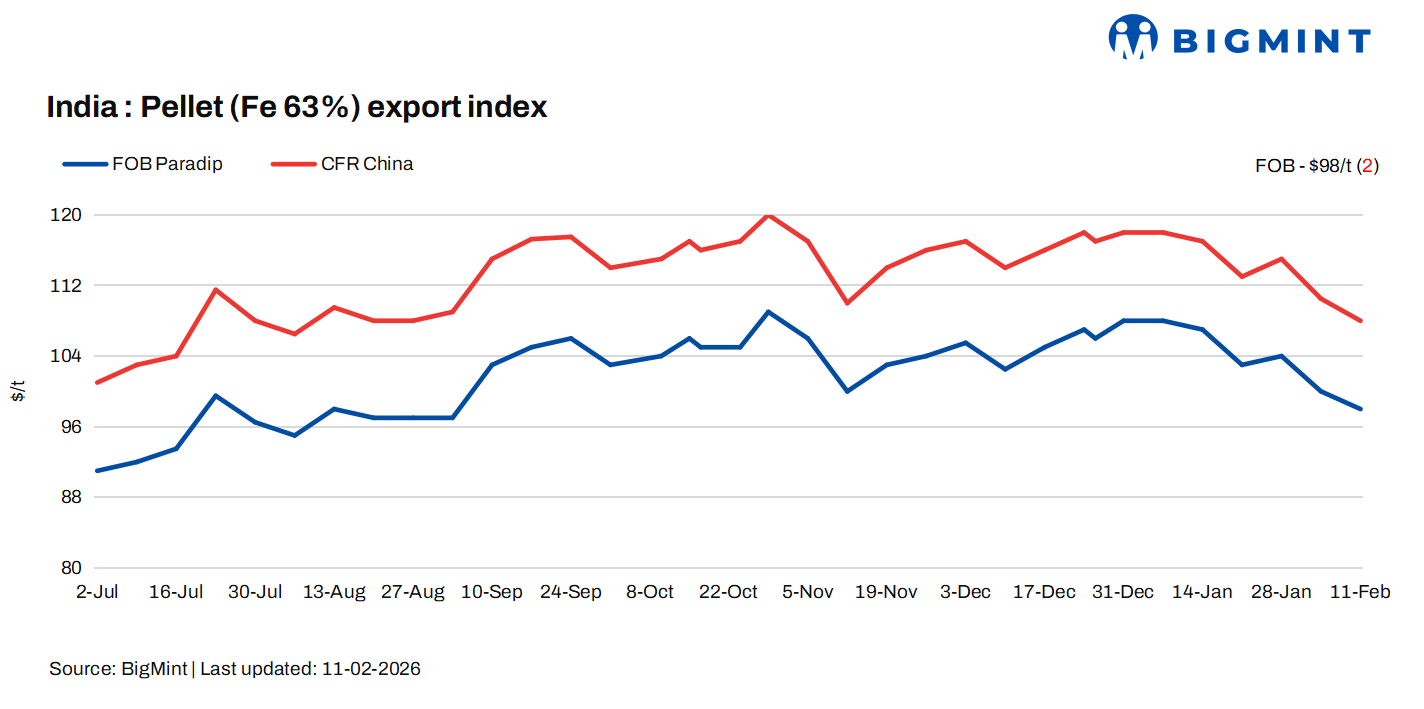

India’s pellet export prices declined by $2/t over the past week on weakening demand and slowing market activity ahead of the upcoming Chinese holidays. Market participants indicated that buying interest in the seaborne market has thinned considerably, with most overseas buyers adopting a wait-and-watch approach.

Price update

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index fell by $2/t w-o-w to $98/t FOB east coast on 11 February 2026. The index hit a five-month low as similar levels were seen in early September 2025. However, recently a deal also got concluded from the east-coast amid lower export price realization and bid-offer disparity.

Market updates

According to an international trader, the market has already entered a “holiday mode”, resulting in fewer inquiries and limited spot negotiations. A trader said, “Prices have been under pressure for the last few days, and seaborne buyers are showing less interest in fresh bookings. Mills in China are reportedly maintaining cautious procurement strategies as global iron ore fines indices continue to trend downward, further weighing on pellet sentiment.”

Despite the overall weakness, buying interest persists for low-alumina pellets. Industry sources noted that a few buyers may participate in the export tender, particularly for premium-grade material. A pellet exporter informed, “Low-alumina pellets are still drawing attention due to their operational advantages for Chinese mills, but bids are coming at lower-than-expected levels.”

East coast-based pellet producers are currently cautious, as lower bids from overseas buyers are squeezing margins. Exporters are reportedly waiting for firmer price signals before committing to large volumes. A producer said, “We are monitoring the situation closely. Unless there is some stability in global indices, aggressive export sales look unlikely.”

Another east coast-based pellet producer said, “We are currently using pellets for our captive steel plant and are not offering them in the export market. However, the counter bids in the market are very low, which is unacceptable from the perspective of other producers.”

In contrast, the domestic pellet market remains firm, supported by active deals and a stable downstream sponge iron and steel segment. Strong domestic realizations are offering some cushion to producers amid export uncertainty.

Market participants are awaiting clearer signals on post-holiday demand trends. Some sellers are still preferring the domestic market on active demand and better price realizations.

Domestic vs export market

Domestic prices exceeded export realizations by around INR 1,500/t ($16.5/t), with the gap widening w-o-w. Pellet (Fe 62.5%) prices in Odisha’s Barbil were recorded at INR 8,650/t ($95/t) exw remaining same as last weekend. Meanwhile, the ex-plant realization in exports from Barbil also dropped w-o-w to INR 6,900/t ($77/t) exw.

Rational

- One confirmed deal from India’s east coast was recorded in this publishing window for T1 trade and was allotted 50% weightage for today’s price calculations. Click here for the detailed methodology.

- Nine (9) indicative prices were received, and seven (7) were considered for the calculation of the index and given a balance 50% weightage.

Factors impacting pellet exports

- Chinese iron ore fines prices drop w-o-w: The benchmark iron ore fines Fe 61% index edged down by $2/dmt w-o-w to $100/dmt CFR China on 10 February. Pre-holiday trading stayed selective, though liquidity in non-mainstream low-grade fines remained adequate. High-low blending demand and steady portside destocking supported the market. With firm import margins and no rush to move April cargoes, sellers may raise offers.

- DCE iron ore futures lower w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2026 contract closed at RMB 763/t ($110/t) on 11 February, weakening by RMB 10/t ($1.5/t) w-o-w.

Outlook

Leave a Reply