- LME zinc stocks decline 1.2% w-o-w

- SHFE MCX futures dip

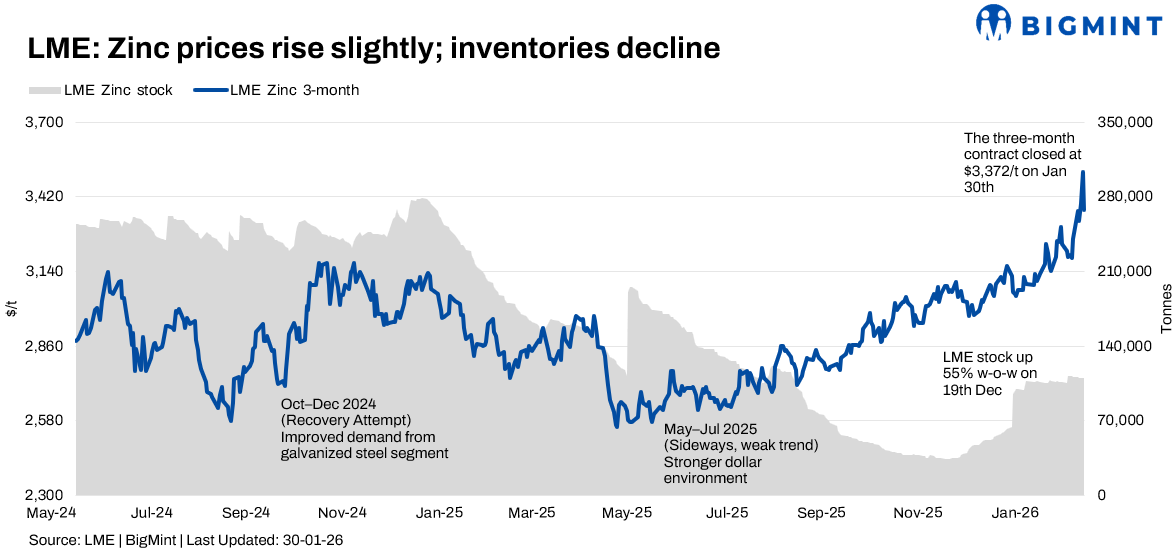

London Metal Exchange (LME) zinc prices inched up during 26-30 January 2026 compared to the previous week, supported by ongoing concentrate supply constraints and resilient demand from galvanising sectors, even as prices faced mild resistance from stable inventories.

Price trends

LME zinc cash prices started at $3,329/t on 26 January, climbed to $3,359/t mid-week, peaked at $3,487/t on 29 January, and settled at $3,343/t on 30 January — a weekly gain of 0.4%. The three-month contract followed suit, rising from $3,367/t to a high of $3,515/t on 29 January before closing at $3,372/t on 30 January (up 0.14% w-o-w), hovering near key resistance at $3,300/t amid technical support.

Inventory analysis

LME zinc stocks continued to decline for the third consecutive week, falling by 1.2% w-o-w from 111,325 t on 26 January to around 110,000 t by the week-end. Although fresh material arrived from Asia, withdrawals outweighed inflows, signalling tightening spot availability.

A European trader remarked that “visible stocks are thinning, but buyers remain cautious at current price levels.”

MCX zinc trends (26-30 Jan)

On the MCX, zinc futures witnessed sharp volatility during 27-30 January, rallying strongly before correcting by 0.6% from the start of the week, with movements broadly in line with global cues. The active contract traded in a wide range of INR 322,400-340,750/t, closing at INR 324,400/t on 27 January, surging to a weekly high of INR 340,750/t on 29 January, before retreating to INR 322,400/t on 30 January amid profit-booking. Trading volumes peaked near the price high, while easing open interest indicated long liquidation rather than fresh short-building, with domestic supply remaining comfortable despite supportive galvanising demand.

SHFE zinc trend

The SHFE March 2026 contract (ZN2603) traded around RMB 23,250/t, up 0.9% w-o-w, with SHFE/LME arbitrage spreads widening slightly to 7.75. Low TC rates at RMB 1,450/t and limited export windows due to domestic tightness sustained premiums, reflecting persistent smelter feedstock pressures in China.

Outlook

Zinc prices are expected to remain supported by concentrate tightness and declining inventories, though further gains may face resistance unless macro sentiment or supply disruptions intensify.

Leave a Reply