- LME aluminium prices rose 2.5% w-o-w

- China’s policy support boosted investor confidence

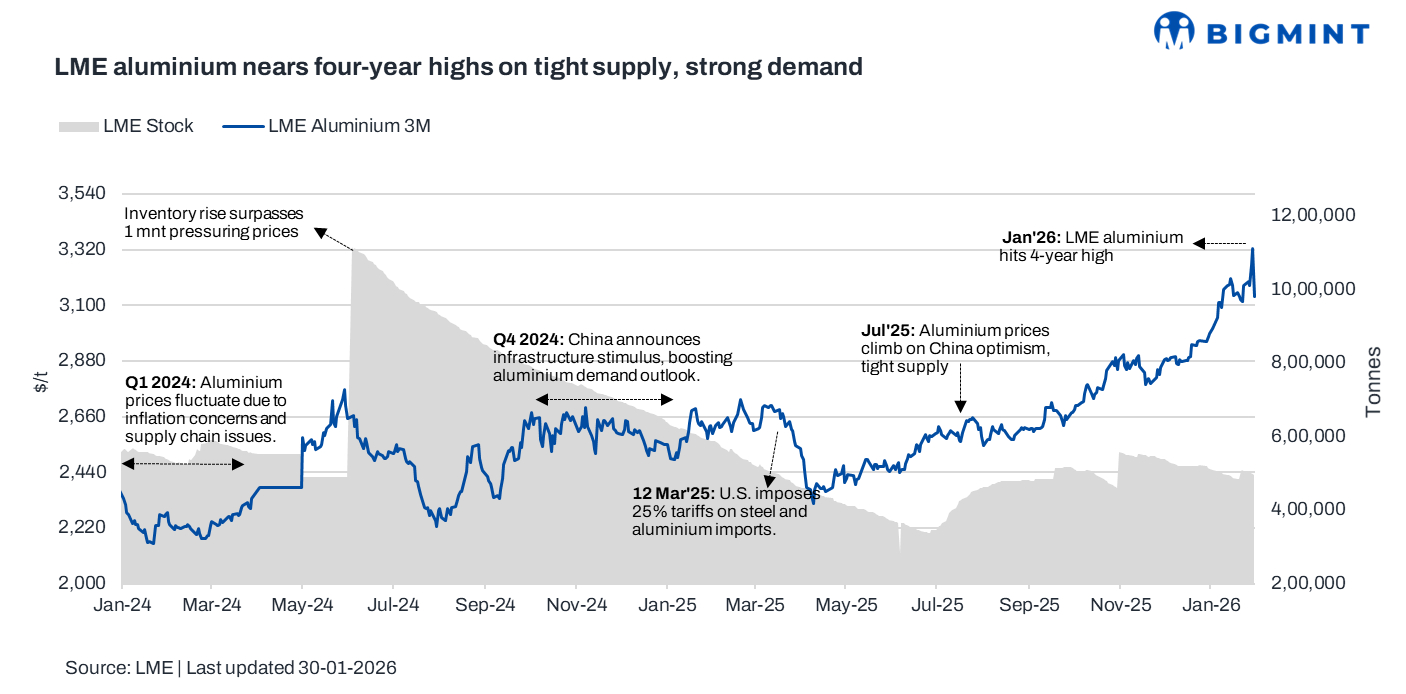

Benchmark aluminium prices on the LME rose 2.5% in the week ended 30 January 2026, climbing to near four-year highs as a weaker US dollar lifted risk appetite. Tight global inventories, power uncertainties at Indonesian smelters, and steady EV and grid demand supported prices, despite expectations of faster supply growth ahead.

Pricing, inventory trends

LME aluminium prices averaged $3,219/t in the week ended 30 January, up $79/t or 2.5% w-o-w. Prices opened the week at around $3,195/t and strengthened mid-week, reaching $3,262/t, and closed the week at $3,134/t.

Meanwhile, LME aluminium inventories gained marginally, reaching at 500,190 t w-o-w from 498,345 t in the week.

Factors impacting prices

Aluminium prices strengthened further w-o-w, as tightening global supply conditions coincided with improving demand sentiment. Supply-side pressures intensified following production disruptions at key smelters in Iceland, Mozambique, and Australia, constraining near-term availability. Adding to the bullish tone, Goldman Sachs raised its H1 average aluminium price forecast to $3,150/t from $2,575/t, citing low global inventories, power availability uncertainty at new Indonesian smelters, and robust demand growth from electric vehicles and power grid expansion. Investor confidence was further supported by early signs of economic stabilisation in China after Beijing reiterated its commitment to policy support.

The People’s Bank of China signalled potential cuts to reserve requirement ratios and interest rates in 2026, reinforcing an accommodative monetary stance. On the supply front, global primary aluminium output edged up 0.5% y-o-y in December to 6.296 mnt, while inventories showed mixed trends, with stocks at major Japanese ports rising 1.5% m-o-m and Shanghai Futures Exchange inventories increasing 6% w-o-w.

Outlook

Aluminium prices are expected to remain well supported in the near term, underpinned by tight global inventories, ongoing supply-side constraints, and firm demand from EV and power infrastructure sectors. Supportive macro signals from China and a softer US dollar may further bolster investor sentiment, keeping price momentum intact despite gradual improvements in global supply.

Leave a Reply