- Total Q3 capex at INR 2,076 cr

- EBITDA per tonne drops q-o-q

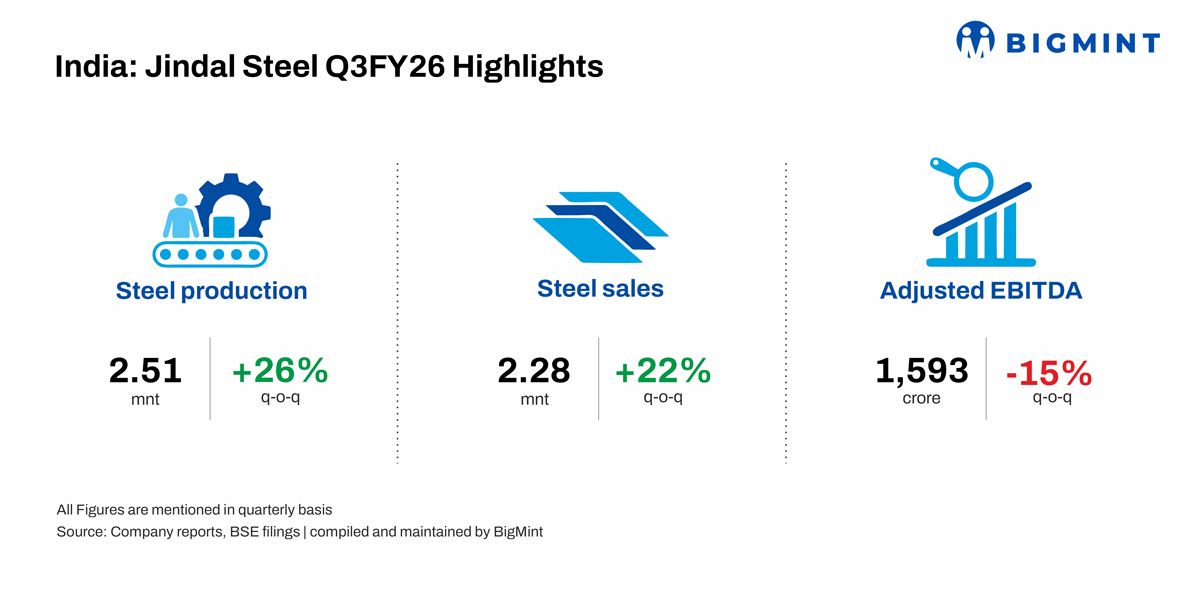

Jindal Steel Ltd’s steel production increased by 26% on the quarter to 2.51 mnt in Q3FY26. Steel sales witnessed an increase of 22% q-o-q to 2.28 mnt during the quarter.

The total capex for Q3FY26 was INR 2,076 crore, primarily directed towards ongoing expansion projects at the Angul steel facility. This investment reflects the company’s continued focus on scaling capacity and project execution during the quarter.

Update on key projects

Angul expansion

- Coal pipe conveyor: Belt laying work completed in Jan’26.

- CRM (Cold Rolling Mill) complex: CGL-1 (Continuous Galvanising Line-1) commissioned; progressive commissioning of multiple lines planned in Q4FY26.

- Utkal BI (Utkal B Iron Ore Mine): Mine opened; overburden removal currently underway.

- Slurry pipeline: 94% completed; commissioning targeted in Q4FY26.

- RMHS (Raw Material Handling System): All critical routes expected to be completed by Q4FY26.

- BOF3 (Basic Oxygen Furnace-3) & PP2 (Pellet Plant-2): Projects progressing as per planned timelines.

Other highlights

Steel production rises q-o-q: The company’s steel production increased by 26% q-o-q to 2.51 mnt in Q3FY26 as against 2 mnt in the previous quarter. Likewise on y-o-y basis, the same rose by 26% from 1.99 mnt in Q3FY25.

Steel sales increase q-o-q: Jindal Steel’s steel sales rose 22% on the quarter to 2.28 mnt during the quarter from 1.87 mnt in Q2FY26. The same witnessed increase of 20% y-o-y from 1.9 mnt in Q3FY25.

EBITDA down q-o-q: The company’s EBITDA dropped q-o-q by 15% to INR 1,593 crores in Q3FY26 from INR 1,875 crores in Q2FY26. Likewise, on y-o-y basis, EBITDA declined by 25% from INR 2,133 crores in the same period last year.

The company’s EBITDA per tonnes witnessed drop of 30% on the quarter to INR 6,981 in Q3FY26 as against INR 10,010 seen in the previous quarter. On yearly basis, the same declined by 38% from INR 11,209.

Raw material costs: Coal consumption costs rose by $2/t in Q3FY26 due to blast furnace (BF2) ramp-up using higher-cost bought-out coke at elevated coke rates. With a new coke oven battery commissioned in November, costs are expected to normalise. However, in Q4FY26, coal costs may rise by $18-20/t sequentially, while iron ore costs also remain elevated.

Steel price movements: Steel prices remained under pressure in Q3FY26, with a sharp decline in realisations and muted demand impacting performance, while auto-linked HRC exposure was limited. The company expects Q4FY26 to be stronger, supported by improved pricing, better underlying steel demand, and higher opening volumes, keeping rebar and HRC prices relatively supported.

Leave a Reply