- Higher bunkers and a firmer BDI supported coal freight rates

- Owner-charterer standoff kept gains limited

Dry bulk coal freight rates to India recorded an uptick in the week ended 30 January, compared with the previous week, driven mainly by the approaching Chinese New Year and a sharp rise in bunker prices following heightened geopolitical tensions, as the US deployed naval forces near Iran. With owners pushing for higher levels ahead of Friday while charterers largely held their ground, market decision-making remains cautious, with participants now largely waiting for clarity in the coming week.

“Asia-Pacific Panamax freight rates edged higher, supported by a sharp d-o-d rise in bunker prices following marginal losses in the previous session.,” a source told BigMint.

Another ship-operator noted, “Asia-Pacific Supramax freight rates were largely firmer, although elevated tonnage in the Indian Ocean weighed on the market, keeping rates under pressure – particularly along India’s east coast.”

“Meanwhile, oil prices extended gains for a third consecutive day on Thursday amid growing concerns that a potential U.S. military strike on Iran could disrupt Middle Eastern supply”, a ship-broker highlighted.

Another supportive factor for freight rates was the sharp rebound in the Baltic Dry Index, which jumped 241 points w-o-w to 2,002 on 29 January 2026. The rise was driven by stronger Panamax and Supramax performance -Panamax climbed 43 points to 1,062 and Supramax rose 56 points to 1,716 – reflecting improved cargo enquiries and firmer sentiment across the mid-sized segments.

Rising bunker costs add support to freight rates amid growing cost concerns

Rising bunker prices are increasingly influencing the vessel freight market, as higher fuel costs push owners to seek firmer freight rates to protect voyage economics. The uptick in bunkers has widened the bid-offer gap, with owners holding out for higher levels while charterers remain cautious, slowing fixture activity in some segments. This cost pressure has lent underlying support to freight rates, particularly on longer-haul routes, even as overall market sentiment remains mixed.

Route-wise updates

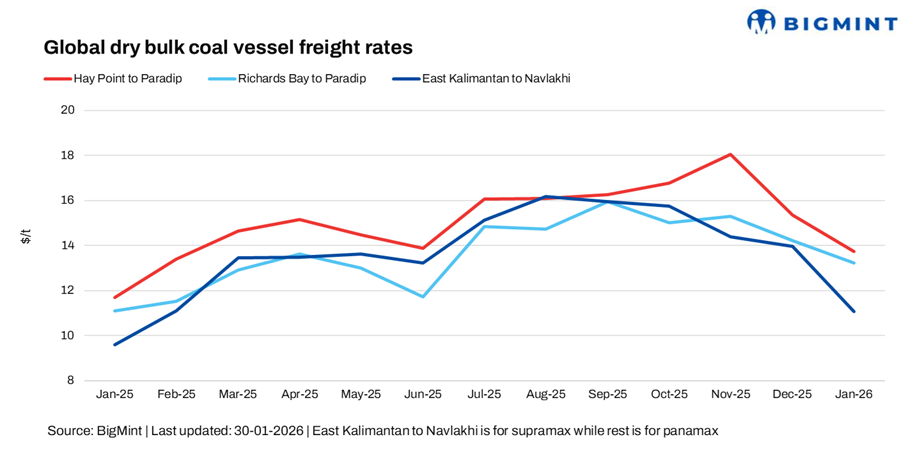

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India edged up by around 0.9/dry metric tonne (dmt) w-o-w to $15.0/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route increased by $0.3/dmt w-o-w to $14.2/dmt.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route rose by around $0.2/dmt w-o-w to $11/dmt.

Outlook

In the near term, dry bulk coal freight into India is likely to stay firm, supported by steady import demand and seasonal power requirements. However, ample vessel availability in the Indian Ocean is expected to limit any sharp upside.

Rising bunker prices and a firmer Baltic Dry Index are providing underlying support, prompting owners to hold rates, while charterers remain cautious. Overall, movements are expected to be modest, with limited volatility in the short term.

Leave a Reply