- China records production growth of 8.3% y-o-y

- Alcoa forecasts higher alumina, aluminum output in CY’26

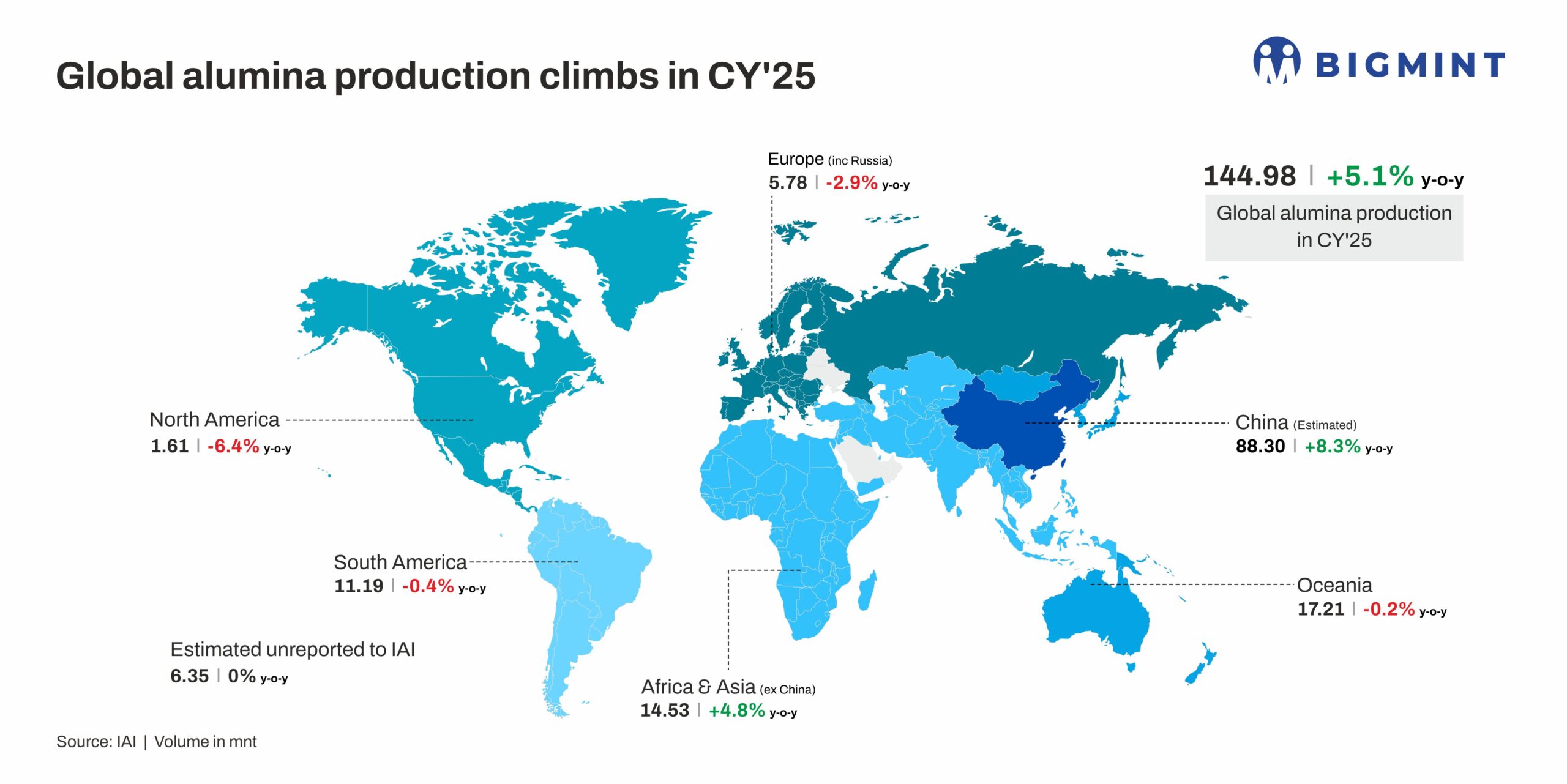

Global alumina production increased by 5.1% y-o-y to 144.98 million tonnes (mnt) in CY’25 from 137.88 mnt in CY’24, according to the International Aluminium Institute (IAI). The growth reflects steady global output, supported by improved refinery operations, capacity expansions, and sustained demand across major producing regions.

Regional performance highlights

China, the world’s largest alumina producer, recorded an estimated 8.3% y-o-y increase in CY’25 output to 88.30 mnt from 81.52 mnt in CY’24, reinforcing its dominant share in global production.

Africa and Asia (excluding China) also saw solid growth, with production rising 4.8% y-o-y to 14.53 mnt, supported by steady refinery operations across India and the Middle East.

In contrast, output in Oceania remained largely flat at 17.21 mnt, marginally lower by 0.2% y-o-y, while South America slipped 0.4% to 11.19 mnt amid uneven refinery utilisations.

Europe (including Russia) posted a 2.9% y-o-y decline to 5.78 mnt, reflecting ongoing energy and raw material constraints. North America saw a sharper contraction, with production falling 6.4% to 1.61 mnt, indicating continued operational challenges.

Global alumina production climbs

Last year began with mixed trends, as production in January dipped slightly compared with December 2024 due to marginal declines in South America and Europe and lower chemical-grade alumina output. However, by March, global production rebounded sharply, rising nearly 10% m-o-m, led by China and supported by Oceania and other regions as winter slowdowns eased.

Mid-year pressures emerged in June, when global output slipped roughly 3% m-o-m to about 12.15 mnt. Softer chemical-grade alumina production, structural pressures in certain regions, and slower refinery operations weighed on overall output. Despite this temporary decline, July saw a robust recovery with production rising about 4% m-o-m to roughly 12.95 mnt, marking the highest monthly total in six months. China drove this rebound as operating capacity and utilisation rates improved to around 81.6%, while overseas expansions, including Indonesia’s PT Bintan Alumina Phase III and Vedanta’s Lanjigarh refinery, added to global output. Limited maintenance disruptions in July allowed steadier operations, and strong alumina prices encouraged refiners to maximise output and optimise supply.

August continued the positive momentum, with production increasing modestly by about 1% m-o-m, driven by contributions from Africa, Asia (excluding China), South America, and Europe. September, however, saw a temporary dip of around 3% m-o-m, as refinery maintenance, energy constraints, and reduced roasting loads in China, Oceania, and other regions temporarily constrained output. Despite these disruptions, year-on-year production remained elevated.

October marked a significant rebound as the issues from September were resolved. Normalised operating rates across China, Oceania, and the Middle East contributed to higher output, with metallurgical-grade alumina rising to 37 mnt and chemical-grade alumina reaching 2.39 mnt. Cumulative consumption from January to September tracked closely with production at 109.7 mnt, with full-year demand projected at 142 mnt, nearly matching forecast production of 145 mnt. November recorded a slight softening after October’s peak, with global output exceeding 13 mnt but down about 1.5% month-on-month. China continued to lead production, while Africa and Asia (excluding China) expanded output modestly, reflecting seasonal refinery scheduling and ongoing market optimisation.

Throughout 2025, global alumina production was shaped by a combination of structural and market factors. China remained the dominant producer, accounting for around 60-62% of global output, while capacity additions in Asia and strong operational performance supported overall growth. Maintenance cycles, energy constraints, bauxite supply variability, and regional logistical challenges led to temporary monthly fluctuations but were largely offset by recovery periods in subsequent months. Elevated alumina prices, favourable arbitrage opportunities, and consistent long-term demand from the aluminium sector encouraged refiners to maintain high operating rates.

Despite temporary disruptions in certain months, global alumina production demonstrated resilience, resulting in a solid year-on-year growth of 5.1% in CY’25. The industry’s ability to recover quickly from operational challenges, coupled with capacity expansions and stable market demand, ensured that global supply remained closely aligned with consumption throughout the year.

Outlook

Global alumina production is expected to remain strong in 2026, supported by ongoing capacity expansions, operational restarts, and robust demand from the aluminum sector. Major producers like Alcoa anticipate higher output, forecasting alumina production between 9.7-9.9 mnt and aluminum output of 2.4-2.6 mnt, driven by smelter restarts and improved refinery operations. While maintenance and restart costs may affect early-year production, market conditions, including firm alumina prices and long-term industry demand, are expected to provide stability.

Leave a Reply