- Higher bunker costs and firmer fixtures support rates

- Steady exports and higher voyage costs keep freights supported

Dry bulk iron ore freight rates increased on a w-o-w basis, primarily driven by higher bunker costs following the sharp rise in Brent crude prices and fixtures being concluded at firmer levels across key routes. The rise in oil prices lifted voyage expenses, prompting shipowners to seek higher freight rates, while improved fixing activity provided the market with near-term support despite mixed underlying commodity fundamentals.

The broader dry bulk market reflected this strength, with the Baltic Dry Index posting a solid weekly gain, supported by improved cargo demand in the Panamax and Supramax segments and firmer Atlantic basin activity. This positive momentum in freight markets contrasted with softer iron ore prices on the Dalian Commodity Exchange, where futures declined amid cautious steel demand, weak downstream margins, and expectations of sufficient near-term supply.

Overall, the increase in iron ore freight rates appears cost-driven rather than demand-led, as higher oil prices and firmer fixtures outweighed the impact of weaker iron ore prices. While steady export volumes and improved fixture flow have helped underpin freight levels, continued pressure on Chinese steel margins and selective chartering are likely to cap further upside in the near term.

China’s iron ore demand remains cautious to soft. Steel mills are operating with compressed margins, and construction activity is still subdued, limiting aggressive restocking. While mills are maintaining steady procurement for near-term needs, there is little evidence of strong inventory build-up.

As a result, iron ore imports are stable rather than expanding, keeping demand supportive enough to sustain shipments but insufficient to drive a strong, demand-led rally in freight rates.

Route-wise updates

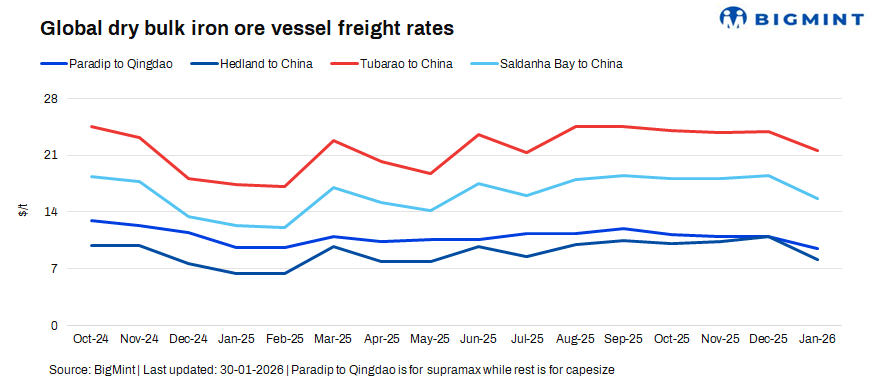

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China rose by $1/dry metric tonne (dmt) w-o-w to $10/dmt on 30 January.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China increased by $0.4/dmt w-o-w to $9/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil-China iron ore shipments gained by $2.5/dmt w-o-w to $24.3/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao surged by $1.9/dmt w-o-w to $17.4/dmt.

Market highlights

- Baltic index gain w-o-w: The Baltic Dry Index rose by 241 points w-o-w to 2,002 on 29 January, supported by improved cargo demand across Panamax and Supramax segments and firmer freight activity in the Atlantic basin.

- Brent crude futures surge w-o-w: Brent crude oil futures jumped about $5.2/bbl w-o-w to $70.4/bbl for the March 2026 contract on 30 January, driven by supply-side concerns, firmer demand outlook, and continued geopolitical risk premiums.

- DCE iron ore futures drop w-o-w: Iron ore futures on the Dalian Commodity Exchange fell by RMB 3.5/t w-o-w to RMB 791.5/t on 30 January, pressured by cautious steel demand, weak downstream margins, and expectations of adequate near-term supply.

Outlook

The near-term outlook for the iron ore freight market is cautiously stable. Freight rates are likely to hold at current levels, supported by higher bunker costs, steady export volumes from major producers, and moderate fixture activity. However, upside potential remains limited as China’s iron ore demand stays measured amid weak steel margins and uncertain construction activity. Ample vessel availability-particularly outside the Capesize segment-and selective chartering are expected to cap gains, keeping the market range-bound with pockets of volatility across routes.

Leave a Reply